HSBC 2011 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

105

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

On a constant currency basis, our personal

lending book was US$394bn, 6% lower than at

31 December 2010 following the reclassification

referred to above. Excluding the reclassification,

total personal lending grew, primarily in the UK due

to growth in mortgage balances, driven by successful

marketing campaigns, and also in Hong Kong, as we

continued to provide competitive mortgage products

for our customers, partly offset by the continued run-

off of the CML portfolio in the US.

At US$279bn, residential mortgage lending

continued to comprise the Group’s largest

concentration in a single exposure type at

31 December 2011. The Group’s most significant

exposure to mortgage lending was in the UK, the US

and Hong Kong. Our UK mortgage portfolio

remained of high quality with an average loan to

value (‘LTV’) ratio for new business of 53%, while

in Hong Kong the average LTV ratio on new

mortgage originations was 49%. The average LTV

ratio of our mortgage books in the UK and Hong

Kong remained low at 52% and 37%, respectively.

The Group’s exposure to personal lending in

the US remained significant. At 31 December 2011,

total personal lending balances were US$67bn, a

decline of 39% compared with 31 December 2010,

largely due to the reclassification of certain lending

balances to held for sale. In 2011, we continued to

make progress in running off the CML portfolio as

balances declined by 15% to US$49.5bn. The rate at

which balances declined during 2011 was slowed by

the industry-wide examination of foreclosure

practices.

In dollar terms, lending balances that were two

months or more delinquent in the CML portfolio

decreased modestly in 2011 reflecting the continued

run-off, partly offset by the temporary suspension of

foreclosure activities. In our held-for-sale Card

and Retail Services portfolio, two months or more

delinquency rates improved as the credit quality of

the overall portfolio improved.

In 2011, we conducted a review of loan

portfolios with significant levels of forbearance.

The review resulted in no significant change in our

loan impairment allowances, though we amended

our presentation of impaired loans to provide more

relevant information on the effects of forbearance

on the credit risk of loans and advances (see

page 133). Our balance of impaired loans increased

significantly under the revised presentation, reducing

the ratio of total impairment allowances to impaired

loans. On a restated basis, this ratio was 42.3%

(2010: 43% instead of 71.6% under the previous

presentation).

Reclassification to assets held for sale

During 2011, the decline in gross loans and advances

was partly due to a reclassification of certain lending

balances to assets held for sale. Disclosures relating

to assets held for sale are provided in certain credit

risk management tables, primarily where the

disclosure is relevant to the measurement of these

financial assets, as follows:

• Maximum exposure to credit risk (page 107);

• Distribution of financial instruments by credit

quality (page 127); and

• Ageing analysis of days past due but not

impaired gross financial instruments (page 129).

Although gross loans and advances and related

impairment allowances are reclassified from ‘Loans

and advances to customers’ and ‘Loans and

advances to banks’ in the balance sheet, there is no

equivalent income statement reclassification. As a

result, charges for loan impairment losses shown in

the credit risk disclosures include loan impairment

charges relating to financial assets classified as

assets held for sale.

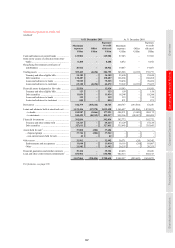

The table below presents ‘Loans and advances

to customers’ and ‘Loans and advances to banks’ as

reported, and those classified as held for sale:

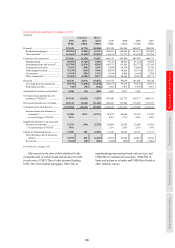

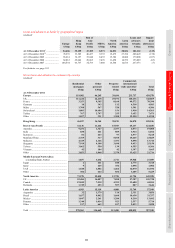

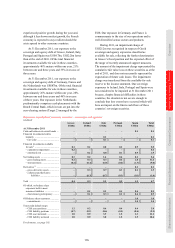

Reported and held-for-sale loans

At 31 December 2011

Total gross

loans and

advances

Impairment

allowances

on loans and

advances

US$m US$m

As reported ............................... 1,139,052 17,636

Assets held for sale .................. 37,273 1,614

Total reported and held

for sale ................................. 1,176,325 19,250

2010 comparative data have not been separately

presented for the credit risk management disclosures

as the amounts are insignificant.

Credit exposure

Maximum exposure to credit risk

(Audited)

Our credit exposure is spread across a broad range

of asset classes, including derivatives, trading assets,

loans and advances to customers, loans and advances

to banks and financial investments.

In 2011, our exposure to credit risk remained

well diversified across asset classes. During the year,

we reduced our exposure to the peripheral eurozone

countries and to countries across the broader