HSBC 2011 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

147

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

any impairment allowances recognised in respect of

impaired loans, as the loans may be performing in

accordance with their contractual terms. Where loans

are not performing in accordance with their

contractual terms, the recovery of cash flows may be

affected by other cash resources of the customer, or

other credit risk enhancements not quantified for the

purposes of the tables above. The Group’s policy for

determining impairment allowances, including the

effect of collateral on these impairment allowances,

is provided on page 190.

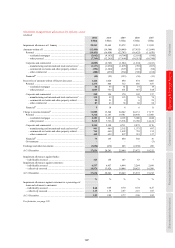

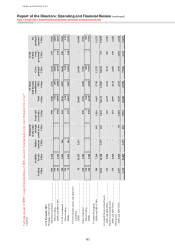

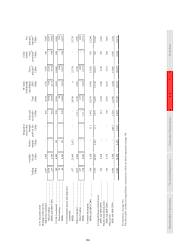

Loans and advances to banks

The following table shows loans and advances to

banks including off-balance sheet loan commitments

by level of collateral.

Loans and advances to banks including loan commitments by level of collateral

(Audited)

Europe

Hong

Kong

Rest of

Asia-Pacific MENA

North

America

Latin

America

Total

US$m US$m US$m US$m US$m US$m US$m

At 31 December 2011

Not collateralised ........................ 25,896 34,892 42,586 9,337 14,132 19,516 146,359

Fully collateralised ..................... 31,515 1,365 6,927 32 978 1,238 42,055

Partially collateralised (A)........... 146 50 445 – 784 114 1,539

– collateral value on A ............ 104 50 207 –702 88 1,151

Total ............................................ 57,557 36,307 49,958 9,369 15,894 20,868 189,953

At 31 December 2010

Not collateralised ........................ 31,225 34,336 32,631 10,416 16,829 22,436 147,873

Fully collateralised ..................... 50,316 154 9,558 188 3,101 4,937 68,254

Partially collateralised (B)........... 91 – 28 – 959 3 1,081

– collateral value on B ............ 64 – 24 – 956 – 1,044

Total ............................................ 81,632 34,490 42,217 10,604 20,889 27,376 217,208

The collateral used in the assessment of the

above relates primarily to cash and marketable

securities. Loans and advances to banks are typically

unsecured. Certain products such as reverse repos

and stock borrowing are effectively collateralised

and have been included in the above as fully

collateralised. The fully collateralised loans and

advances to banks for Europe in the table above

consist primarily of reverse repurchase agreements

and stock borrowing.

Derivatives

The ISDA Master Agreement is our preferred

agreement for documenting derivatives activity. It

provides the contractual framework within which

dealing activity across a full range of OTC products

is conducted, and contractually binds both parties

to apply close-out netting across all outstanding

transactions covered by an agreement if either party

defaults or another pre-agreed termination event

occurs. It is common, and our preferred practice, for

the parties to execute a Credit Support Annex

(‘CSA’) in conjunction with the ISDA Master

Agreement. Under a CSA, collateral is passed

between the parties to mitigate the counterparty risk

inherent in outstanding positions. The majority of

our CSAs are with financial institutional clients.

A description of the derivative offset amount

in the ‘Maximum exposure to credit risk’ table is

provided on page 107.

Other credit risk exposures

In addition to collateralised lending described above,

other credit enhancements are employed and

methods used to mitigate credit risk arising from

financial assets. These are described in more detail

below.

Government, bank and other financial institution

issued securities may benefit from additional credit

enhancement, notably through government

guarantees that reference these assets. Details of

government guarantees are included in Notes 15, 19

and 21 on the Financial Statements. Corporate issued

debt securities are primarily unsecured. Debt

securities issued by banks and financial institutions

include ABSs and similar instruments, which are

supported by underlying pools of financial assets.

Credit risk associated with ABSs is reduced through

the purchase of CDS protection. Disclosure of the

Group’s holdings of ABSs and associated CDS

protection is provided on page 152.

Trading assets include loans and advances held

with trading intent, the majority of which consist of