HSBC 2011 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

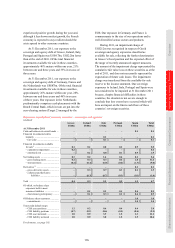

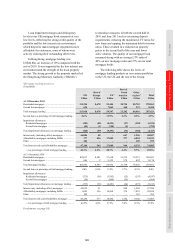

Risk > Credit risk > Areas of special interest > US personal lending

124

US personal lending

(Unaudited)

Credit quality

During 2011, economic conditions in the US

remained challenging. However, they began to show

signs of improvement during the fourth quarter as

employment growth accelerated, in part due to

seasonal hiring, and increased consumer spending.

House prices remained under pressure during 2011

due to foreclosure levels, which remained high,

despite the industry-wide delays in foreclosure

processing.

Unemployment rates, which are a major factor

in the deterioration of credit quality, remained high

at 8.5% in December 2011, down from 9.4% in

December 2010. Unemployment rates were at or

above the US national average in 17 states.

A future improvement in the US economy

remains dependant upon a recovery in the housing

market, a fall in unemployment rates, the

stabilisation of energy prices and improved

consumer confidence. Any further weakening in

these factors may continue to adversely affect

consumer payment patterns and credit quality.

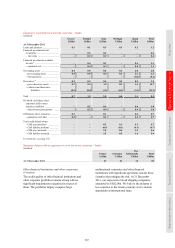

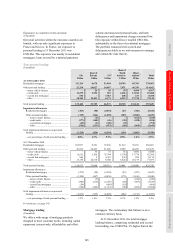

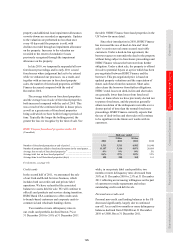

Mortgage lending

In 2011, we further reduced our mortgage exposure

in the US as balances continued to run-off in the CML

portfolio, as discussed on page 122. At 31 December

2011, residential mortgage lending balances were

US$52.5bn, a decline of 9% compared with the end of

2010. The ratio of impairment allowances to total

mortgage lending in HSBC Finance increased from

8.5% at 31 December 2010 to 11.5% at 31 December

2011. This increase largely reflected the effects of the

delays in foreclosure activity and the increased

forbearance activity within the portfolio.

Real estate markets in the US have been affected

by stagnation or declines in property values. As a

result, LTV ratios for our real estate secured loans

have generally deteriorated since origination. Lending

balances with LTV ratios of greater than 100% have

historically had a greater likelihood of becoming

delinquent, resulting in higher loss severity which

could adversely affect our loan impairment

allowances. For more information on residential

mortgages by levels of collateral, see page 144.

In the CML portfolio, two months or more

delinquent balances increased compared with the end

of 2010. This was due to the temporary suspension of

foreclosure activities, which resulted in a slowing in

the rate at which lending balances were transferred to

foreclosed. As a result, in our Consumer Lending

portfolio, two months or more delinquent balances

increased in dollar terms from US$4.9bn at

31 December 2010 to US$5.1bn at 31 December

2011, while in our Mortgage Services portfolio they

remained unchanged at US$2.8bn.

At HSBC Bank USA, two months or more

delinquency rates increased from 7.9% to 8.2%

at 31 December 2011, reflecting the suspension of

foreclosure activities.

Second lien mortgage loans have a risk profile

characterised by higher LTV ratios because in the

majority of cases the loans were taken out

to complete the refinancing of properties. Loss

experience on default of second lien loans has

typically approached 100% of the amount

outstanding, as any equity in the property is initially

applied to the first lien loan. The majority of second

lien loans are to customers that hold a first lien

mortgage issued by a third party. Impairment

allowances for these loans are determined by

applying a roll-rate migration analysis which

captures the propensity of these loans to default

based on past experience. Approximately 97% of

our US second lien mortgages, where the first lien

mortgages are held or serviced by us and have a

delinquency status of 90 days or more past due,

are themselves 90 days or more past due. Once

we assume a second lien mortgage loan is likely to

progress to write-off, the loss severity assumed in

establishing our impairment allowance is close to

100%. In the US, second lien mortgage balances

declined by 24% to US$7.1bn at 31 December 2011,

representing 12% of the overall US mortgage

lending portfolio. Two months or more delinquent

balances were US$0.7bn at 31 December 2011

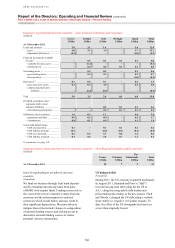

compared with US$0.8bn at 31 December 2010.

Prior to foreclosure, carrying amounts of the

loans in excess of fair value less costs to sell are

written down to the discounted cash flows expected

to be recovered, including from the sale of the

property. Broker price opinions are obtained and

updated every 180 days and real estate price trends

are reviewed quarterly to reflect any improvement

or additional deterioration. Our methodology is

regularly validated by comparing the discounted

cash flows expected to be recovered based on current

market conditions (including estimated cash flows

from the sale of the property) to the updated broker

price opinion, adjusted for the estimated historical

difference between interior and exterior appraisals.

The fair values of foreclosed properties are initially

determined based on broker price opinions. Within

90 days of foreclosure, a more detailed property

valuation is performed reflecting information

obtained from a physical interior inspection of the