HSBC 2007 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

HSBC HOLDINGS PLC

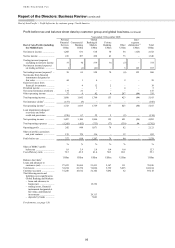

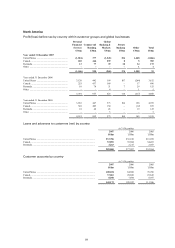

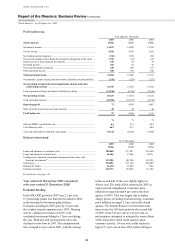

Report of the Directors: Business Review (continued)

North America > 2007

96

in servicing fees on mortgages, credit card fees and

deposit service charges.

Trading losses in 2007 were US$215 million

compared with trading income of US$274 million in

2006. Conditions in the housing market meant that

sub-prime mortgages could not be securitised, which

led to significantly wider credit spreads and a

considerable loss of market liquidity across all asset-

backed securities classes. These two factors, the loss

of liquidity and wider credit spreads, resulted in

substantial reductions in the value of mortgages held

for sale. In light of this, HSBC closed Decision One,

its wholesale mortgage business, in the second half

of 2007.

Gains less losses from financial instruments rose

to US$176 million from US$14 million in 2006, due

to the sale of MasterCard Inc. shares following its

IPO.

Other operating income fell by 109 per cent.

Losses on foreclosed properties rose due to the

combined effect of an increase in the stock of such

properties and a reduction in their value due to

falling prices. Total foreclosed assets rose to

US$1.0 billion from US$670 million in 2006. The

fall in other operating income also reflected a

US$123 million gain in 2006 (from the sale of

HSBC’s investment in Kanbay, a global IT services

firm) which did not recur in 2007.

Loan impairment charges and other

credit risk provisions rose by 78 per cent to

US$11.9 billion. US loan impairment charges rose

by 79 per cent as the deterioration in housing credit

markets extended to affect loans of all product types

and vintages, particularly loans originated in 2005,

2006 and the first half of 2007. The combination of

reduced financing options for consumers and weak

or falling property values had a significant impact on

delinquency levels. Developments in the credit

markets have raised fundamental concerns about the

viability of the ‘originate and distribute’ business

model for securitising residential mortgages. The

resulting industry-wide tightening of underwriting

criteria, and the elimination of many loan products

previously offered to consumers, reduced the general

availability of credit and borrowers’ ability to

refinance. This, in turn, exacerbated house price

falls, most notably in those areas which had seen the

most rapid appreciation in recent years.

Lower house prices reduced the equity which

customers had in their homes, removing a key source

of accessible funds and reducing customers’ capacity

to deal with unexpected problems such as

unemployment or illness. Bankruptcy levels also

increased from the exceptionally low levels seen

in 2006 which followed changes in bankruptcy

legislation in 2005.

In mortgage services, loan impairment charges

rose by 41 per cent to US$3.1 billion. Due to the

factors noted above, delinquencies increased at a

higher rate than was expected from normal portfolio

seasoning1, particularly for second lien customers.

In consumer lending, loan impairment charges

rose by 139 per cent to US$4.1 billion as evidence of

credit quality deterioration was seen across the loan

portfolio in the second half of 2007, in particular on

first lien loans originated in 2006. There was also

increased delinquency on second lien loans

purchased between 2004 and the third quarter of

2006. Lower run-offs of loans, growth in average

lending balances, normal seasoning and a rise in

bankruptcy filings to historically more usual levels

after the exceptional decline in 2006, also

contributed to the rise. There was a marked increase

in loan delinquency in those states most affected by

the fall in home values.

Credit card impairment charges rose by 83 per

cent to US$2.8 billion as a result of weaker

economic trends, growth in balances, normal

portfolio seasoning, a rise in bankruptcy rates closer

to historical levels, and a shift in mix to a higher

proportion of non-prime loans.

Loan impairment charges in Canada rose by

38 per cent, in line with the rise in loan balances and

seasoning of the vehicle finance and credit card

portfolios. In addition, an impairment charge on non-

bank asset-backed commercial paper (‘ABCP’) was

recognised in 2007.

Operating expenses rose by 2 per cent to

US$7.6 billion. In the US, while origination costs

fell as loan growth was curtailed, additional

resources were deployed to collection activities and

the retail bank added selectively to its branch

distribution network. Within the consumer finance

operations, restructuring costs in 2007 totalled

US$103 million, following the decision to reposition

the US consumer finance business, the closure of the

wholesale mortgage services business and the

reduction in the number of branches in the US

consumer lending network to around 1,000 to align

with the level of demand expected in light of the

Group’s revised risk appetite. The retail bank

incurred higher staff costs due to expansion of the

branch network, higher average salaries due to

normal annual pay increases, and a change in mix of

1 ‘Seasoning’ describes the emergence of credit loss patterns in portfolios over time.