HSBC 2007 Annual Report Download - page 241

Download and view the complete annual report

Please find page 241 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

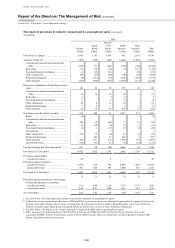

239

Releases and recoveries in Europe of

US$860 million were 17 per cent higher than in

2005. Increases in the UK were partially offset by a

decline in France. In the UK, increased resources

deployed on collection activities, combined with a

rise in sales of delinquent debt, were reflected in

significantly higher recoveries. The non-recurrence

of several significant recoveries in 2005 led to a

large fall in France.

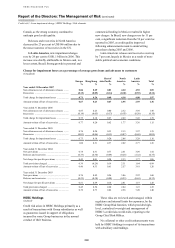

In Hong Kong, new loan impairment charges

declined by 22 per cent to US$243 million,

reflecting the non-recurrence of an individual charge

in 2005 for a large commercial customer. This was

partly offset by a rise in credit card impairments as a

result of a rise in balances. Overall, credit quality

remained stable as strong economic growth and low

levels of unemployment continued.

Releases and recoveries fell by 49 per cent to

US$86 million, again mainly as a result of fewer

individual impairment releases in the corporate and

commercial sector and the non-recurrence of

mortgage lending recoveries in 2005, following

improvement in the property market since 2004.

In Rest of Asia-Pacific, there was an 88 per

cent rise in new impairment allowances to

US$737 million. This was an improvement on the

situation in the first half of 2006, when new

impairment charges were 111 per cent higher than in

the first half of 2005. The year-on-year increase was

largely due to Taiwan and, to a lesser extent,

Indonesia. During the first half of 2006, new

government regulations placing restrictions on

collection activity, combined with the popularity of

renegotiation schemes offering the opportunity to

waive interest and postpone principal payments, led

to a sharp rise in credit card defaults, for which a

full-year charge of US$200 million was recorded. In

the second half of 2006, this problem had begun to

moderate and new impairment charges were 31 per

cent lower than in the first half. In Indonesia,

increased loan impairment charges in the personal

sector reflected legislation which introduced higher

minimum payment rules and a reduction in fuel

subsidies. There were further rises in the Middle

East, largely due to loan growth. Elsewhere in the

region, credit quality was stable.

Releases and recoveries in the region fell by

11 per cent to US$225 million. The fall was mainly

in Malaysia and was partly offset by a rise in

commercial releases and recoveries in the Middle

East.

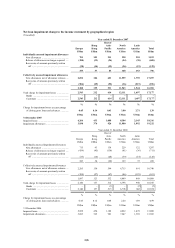

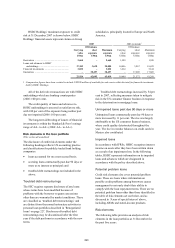

In North America, new loan impairment

charges rose by 36 per cent. Excluding Metris,

new charges increased by 30 per cent. Credit

deterioration, mainly in second lien, some portions

of first lien and adjustable-rate mortgages acquired

from third party correspondents through HSBC’s

mortgage services business, were the primary cause

of the rise in new charges. As the housing market in

the US slowed through 2006 and interest rates rose,

delinquency trends on both second lien and portions

of first lien mortgages originated in 2005 and 2006

were higher than for loans made in previous years. In

addition, the extra payment obligations arising from

the repricing of adjustable-rate mortgages to higher

rates added to the assessed impairment of the

correspondent portfolio, in particular in respect of

second lien mortgages ranking behind adjustable-

rate first lien mortgages.

As interest rate adjustments will be occurring in

an environment of lower home value appreciation

and tightening credit, it is estimated that the

probability of default on adjustable-rate first

mortgages subject to repricing, and on any second

lien mortgage loans that are subordinate to an

adjustable-rate first lien, will be greater than has

been experienced in the past. As a result, loan

impairment charges relating to the mortgage services

portfolio have increased significantly.

In the second half of 2006, HSBC took action to

tighten credit criteria in the mortgage services

operation as detailed on page 217. As a consequence,

balances in mortgage services declined compared

with 30 June 2006.

Notwithstanding the credit weakness witnessed

in the mortgage services business, credit delinquency

in the majority of the other portfolios, including

mortgage balances originated through the branch-

based consumer lending business, rose modestly,

driven by portfolio ageing and an increased

proportion of credit card loans following the Metris

acquisition. Partially offsetting factors included the

effects of a decline in bankruptcy filings, especially

in the first half of 2006 following the spike in the

fourth quarter of 2005, low unemployment and the

non-recurrence of charges relating to hurricane

Katrina.

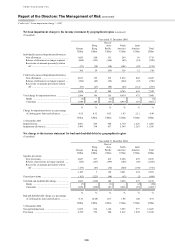

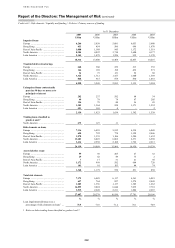

HSBC in the US closely monitors the two-

month-and-over contractual delinquency ratio (being

the ratio of two or more months delinquent accounts

to gross loans and advances), as management views

this as an important indicator of future write-offs.

Details are disclosed below. The rise in the total ratio

was chiefly as a result of the mortgage services

business.

The increase in the US was partly offset by a

small decline in new loan impairment charges in