HSBC 2007 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

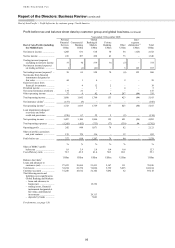

HSBC HOLDINGS PLC

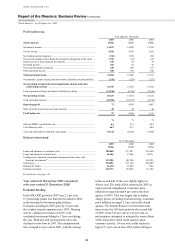

Report of the Directors: Business Review (continued)

North America > 2007

94

credit lines and reducing the volume of balance

transfers in credit cards, and restructuring the

consumer lending branch network by closing some

400 branches of HSBC Finance to reflect expected

lower demand. These measures gave rise to

restructuring charges of US$103 million in the

US in 2007.

US pre-tax losses of US$1.8 billion were

predominantly due to higher loan impairment

charges, trading losses in the wholesale mortgage

origination business and lower income from fewer

receivables in the correspondent mortgage services

business. In line with industry trends, the credit

quality of loans weakened steadily throughout the

year, particularly those underwritten in 2005, 2006

and the first half of 2007.

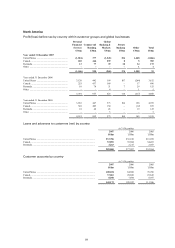

In Canada, profit before tax rose by 2 per cent to

US$265 million, benefiting from the strong local

economy. Of this, the retail bank generated

US$116 million, including an US$8 million gain on

the sale of shares in the Montreal Exchange.

Consumer finance operations added US$149 million

through balance sheet expansion in the first part of

the year, prior to a fourth quarter restructuring to

align with changes in the US consumer finance

operation.

Net interest income grew by 1 per cent to

US$13.2 billion as growth in card and average

deposit balances marginally offset a fall in US

deposit margins. In the US, net interest income rose

by 1 per cent as the mix of business changed to

higher yielding activity and HSBC raised rates on

new consumer finance mortgages to reflect increased

risk. The beneficial effect on yields was, however,

more than offset by the impact of non-performing

assets and a higher cost of funds. Higher volumes of

non-performing loans constrained revenue. Fewer

mortgages repaid early as refinancing activity

declined substantially, and this also resulted in lower

prepayment penalties. These factors combined to

limit HSBC’s ability to pass on in full the increased

cost of funds in a higher average rate environment.

This led to an overall decline in spreads.

In the US, average deposit balances were 19 per

cent higher, reflecting growth in the online savings

account and certificate of deposit products. A

competitively priced special promotional rate offer

in the first quarter of 2007 led to 147,000 new

account openings and US$5 billion of new balances

during the year, offset in part by decreases in money

market term deposits. At 31 December 2007, online

savings balances with HSBC Direct stood at

US$11.5 billion, held by more than 620,000

customers. HSBC Premier customer numbers rose

by 16 per cent. Deposit spreads tightened, reflecting

a change in the product mix from lower-paying

savings accounts to the higher-paying offerings

available online and in branches. HSBC Bank USA

opened 26 new branches during the year.

The slowdown in the US housing market first

noted in 2006 accelerated in 2007, with further

deterioration in sales of new and existing homes and

lower new-build activity. Market surveys showed a

broad-based decline in house prices, especially for

larger loans and in states that had experienced the

fastest rates of house price appreciation in recent

years. Average US mortgage balances declined by

2 per cent to US$123 billion.

Average mortgage balances originated through

the consumer lending branch network rose by

18 per cent, primarily driven by lower levels of

repayments and the severe contraction in market

capacity, which drove qualifying borrowers to the

few remaining market participants. Actions taken by

HSBC to restrict the product range, increase

collateral requirements, raise prices and close or

consolidate about 400 branches of HSBC Finance

during 2007 combined to curb lending growth

towards the end of the year.

Yields on consumer lending mortgages declined

overall due to increases in delinquency, loan

modifications (which deferred scheduled moves to

higher rates) and levels of non-performing loans, and

decreases in repayments, which resulted in reduced

prepayment penalties. Interest spreads narrowed as

funding costs rose.

In the mortgage services business, average

balances declined by 14 per cent to US$43 billion,

reflecting HSBC’s decision to wind down this book

in response to the deterioration in market conditions.

Spreads fell, driven by higher non-performing loans

and increased funding costs.

HSBC Bank USA’s average mortgage balances

fell by 9 per cent to US$31 billion. HSBC continued

to sell down new loan originations to government-

sponsored enterprises and private investors and, with

the exception of certain products, did not replace the

existing portfolio being run-off. Interest rate spreads

on the prime mortgage portfolio declined, primarily

due to loan portfolio run off.

Average credit card balances increased by

14 per cent to US$29 billion. Volumes in the

sub-prime and near-prime portfolios rose due to

additional marketing to this segment in late 2006 and

the first half of 2007. Expansion slowed during the

second half of 2007 as HSBC restricted growth in

customer loans and advances in light of the