HSBC 2007 Annual Report Download - page 185

Download and view the complete annual report

Please find page 185 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

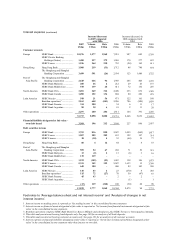

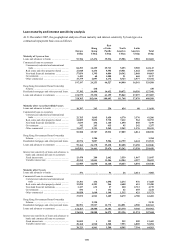

183

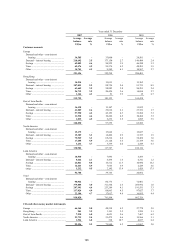

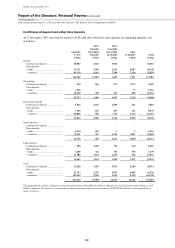

Off-balance sheet arrangements and

special purpose entities

(Audited)

This section contains disclosures about off-balance

sheet arrangements and special purpose entities

(‘SPEs’) that have been included in HSBC’s

consolidated balance sheet.

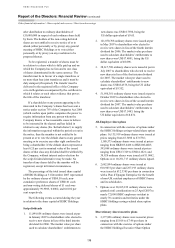

Special purpose entities (including on and

off-balance sheet arrangements)

HSBC enters into certain transactions with

customers in the ordinary course of business which

involve the establishment of SPEs to facilitate

customer transactions.

HSBC structures that utilise SPEs are authorised

centrally upon establishment to ensure appropriate

purpose and governance. The activities of SPEs

administered by HSBC are closely monitored by

senior management. The use of SPEs is not a

significant part of HSBC’s activities and HSBC is

not reliant on the use of SPEs for any material part

of its business operations or profitability. HSBC’s

involvements with SPE transactions are described

below.

HSBC-sponsored vehicles

HSBC sponsors the formation of entities to

accomplish certain narrow and well-defined

objectives, such as securitisations of financial assets

or to effect a lease. HSBC consolidates these SPEs

when the substance of the relationship indicates that

HSBC controls the SPE. In assessing control, all

relevant factors need to be considered. Such factors

may have qualitative and quantitative aspects. For

example:

Qualitative factors. In substance:

• the activities of the SPE are being conducted on

behalf of HSBC according to HSBC’s specific

business needs so that it obtains benefit from the

SPE’s operation. This might be evidenced, for

example, by HSBC providing a significant level

of support to the SPE; and

• HSBC has the decision-making powers to obtain

the majority of the benefits of the activities of

the SPE.

Quantitative factors – hereinafter referred to as

‘the majority of risks and rewards of ownership’. In

substance:

• HSBC has rights to obtain the majority of the

benefits of the SPE and therefore may be

exposed to risks incidental to the activities

of the SPE; and

• HSBC retains the majority of the residual or

ownership risks related to the SPE or its assets

in order to obtain benefits from its activities.

In a number of cases, these SPEs are accounted

for off-balance sheet under IFRSs where HSBC does

not have the majority of the risks and rewards of

ownership of the SPE. However in certain

circumstances, after careful consideration of the

facts, HSBC consolidates an SPE where, although it

does not obtain the majority of risks and rewards of

ownership, the qualitative features of HSBC’s

involvement indicate that, in substance, the activities

of the SPE are being conducted on behalf of HSBC.

HSBC reassesses the required consolidation

accounting tests whenever there is a change in the

substance of a relationship between HSBC and an

SPE, for example, when there is a change in HSBC’s

involvement or there is a change in the governing

rules, contractual arrangements or capital structure

of the SPE. The most significant categories of SPEs

are discussed in more detail below.

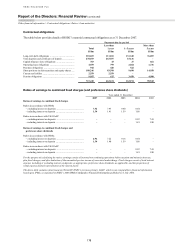

Structured investment vehicles

Structured investment vehicles (‘SIVs’) are SPEs

which are established to invest in diversified

portfolios of interest-earning assets, generally

comprising asset-backed debt securities and other

debt securities issued by financial institutions or

corporates. SIVs are typically funded through the

issue of CP, medium-term notes or other senior debt

(collectively referred to as ‘senior debt’), repo

financing, and subordinated income or mezzanine

notes (commonly referred to as ‘capital notes’).

The sponsor of the SIV would typically provide only

limited liquidity support to the senior debt investors

through committed liquidity facilities.

SIVs are structured to provide investors with the

opportunity to invest in a range of assets depending

on their risk preference. Senior debt issued by SIVs

is structured to be highly rated and the SIVs are

managed within strict operating criteria. Liquidity in

SIVs is primarily managed by rolling over debt at

maturity or, if that is not possible, by the sale of

assets to provide protection to senior debt holders.

SIVs are typically subject to market value and net

asset value triggers which underpin the external

credit ratings of the senior debt. The liquidity risk in

SIVs is managed by controlling the maximum

cumulative cash outflow occurring in defined time

periods.

HSBC sponsored the establishment of two SIVs,

Cullinan and Asscher in August 2005 and May 2007,

respectively, which were successful in obtaining

funding from investors, who subscribed for senior