HSBC 2007 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

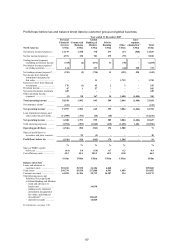

103

correspondent business, concentrated in second lien

and portions of first lien mortgages originated and

purchased in 2005 and 2006. As noted previously,

HSBC witnessed a deterioration in the performance

of these 2005 originations during the first half of

2006. This deterioration continued into the third

quarter and started to affect equivalent loans

originated in 2006. In the final quarter of 2006,

deterioration of these loans, largely the first lien

adjustable-rate and second lien loans, worsened

considerably. The heightened risk of loss was

attributable to lower equity in homes as price growth

moderated or reversed, together with a higher

prospective interest burden from ARM resets. As

many of these mortgages were being re-priced in an

environment of higher interest rates, slower asset

price appreciation and tightening credit, HSBC

considers it highly likely that these factors will lead

to increased instances of default in the future on both

first and any associated second lien loans.

Accordingly, a significant increase in loan

impairment charges was recorded in the final

quarter of the year.

Higher lending, the seasoning of the loan

portfolio, and a return to more normal historical

levels of delinquency from the exceptionally

favourable credit conditions experienced in recent

periods, all contributed to the overall increase in

impairment charges in the US. This was partly offset

by lower numbers and levels of bankruptcy filings

and the positive effect of low unemployment. The

credit card business, in addition, benefited from

improved recovery rates from loans previously

written off. Notwithstanding the accelerated credit

weakness witnessed in the mortgage services

correspondent business, credit performance as

measured by delinquency and loss in the majority of

the other lending portfolios, including mortgage

balances originated through the branch-based

consumer lending business gradually deteriorated

from the seasoning of a growing portfolio and the

rising proportion of credit card balances. Loan

impairment charges in these portfolios were

consequently higher in the second half of 2006 as

these portfolios seasoned, coinciding with the

weakening housing market.

In Canada, loan impairment charges were 38 per

cent higher. This primarily reflected the non-

recurrence of loan impairment releases from core

banking operations, which occurred in 2005, as well

as growth in both secured and unsecured lending

balances and higher delinquency rates in the motor

vehicle finance business.

Operating expenses grew by 12 per cent

to US$7.4 billion. In the US, costs of US$6.7 billion

were 11 per cent higher than in 2005. In the

consumer finance business, the rise was driven by

increased headcount to support incremental

collections activity, and greater volumes. Higher

costs were incurred in marketing cards to support the

launch of new co-branded credit cards, greater levels

of mailing and other promotional campaigns in the

cards and retail services businesses. IT and

administrative expenses grew in support of higher

asset balances. A lower level of deferred origination

costs in the mortgage services business, due to a

decline in volumes, contributed further to the cost

growth.

In HSBC Bank USA, expense growth was

primarily driven by branch staff costs from

additional headcount recruited to support investment

in business expansion and new branch openings.

Greater emphasis placed on increasing the quality

and number of branch staff dedicated to sales and

customer relationship activities, which changed the

staff mix, also contributed to cost growth. The

continued promotion of the online savings product,

new branch openings and branding initiatives at the

John F. Kennedy International and LaGuardia

airports in New York led to a rise in marketing costs.

IT costs also grew following significant investment

expenditure incurred on several key network

efficiency projects.

In Canada, costs rose by 19 per cent, mainly due

to higher staff and marketing costs. Staff costs grew

by 13 per cent, with increased headcount supporting

expansion of the consumer finance business and

bank distribution network. Continuing investment in

growing the wealth management business and higher

incentive costs reflecting improved revenues also

contributed to the increase. Marketing costs grew

following external campaigns to improve brand

awareness.

Commercial Banking’s pre-tax profits rose by

4 per cent to US$957 million, largely driven by

lending and deposit growth and higher fee income,

partly offset by increased loan impairment charges.

Costs rose mainly from geographical expansion in

the US and branch and business expansion in

Canada. The cost efficiency ratio worsened by

2.1 percentage points, as costs grew faster than

revenues.

Net interest income grew by 15 per cent to

US$1.4 billion. In the US, net interest income was

13 per cent higher, as HSBC continued to expand its

geographical presence, notably in Boston,

Connecticut, New Jersey, Philadelphia, Washington

D.C., Chicago and Los Angeles. Average deposit

balances rose by 30 per cent, aided by geographical