HSBC 2007 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

HSBC HOLDINGS PLC

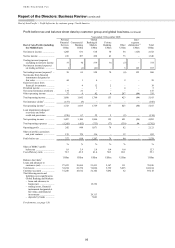

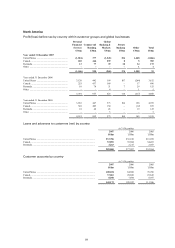

Report of the Directors: Business Review (continued)

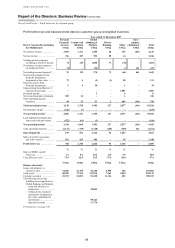

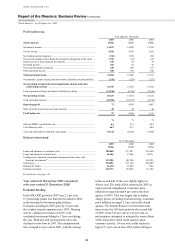

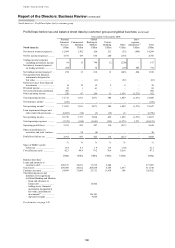

North America > 2007 / 2006

98

fee income rose with the increase in activity

volumes. Higher service charges and credit fees

were the main fee generators.

Loan impairment charges rose by 151 per cent

to US$191 million, reflecting the growth in the loan

book. In the US, loan impairment charges rose by

91 per cent, mainly due to the higher probability of

default among commercial real estate loans and a

change in methodology for loan impairment

allowances on a small business revolving loan

portfolio. Several condominium development

projects took longer to complete than intended,

resulting in cash flow issues for some customers.

This hindered their ability to obtain a mortgage at

the end of the construction phase which, in some

cases, precipitated downgrades by ratings agencies,

all of which combined to generate increased

impairment charges. In Canada, loan impairment

charges increased due to exposures to certain sectors

affected by the strength of the Canadian dollar. An

impairment charge for non-bank ABCP was also

taken. The risk reflected the historically low

impairment charges incurred in 2006.

Operating expenses rose by 8 per cent to

US$893million. US costs rose by 9 per cent as the

expansion of the branch network led to higher staff

and administration costs. Costs for collection

activities also rose. In Canada, costs rose by 2 per

cent due to an increase in headcount, higher staff

incentives, increases in business licenses, taxes, and

higher cheque clearing costs in line with rises in

business activity levels. The tight labour market

added upward pressure on staff costs and created

challenges in filling vacancies, particularly in

Western Canada.

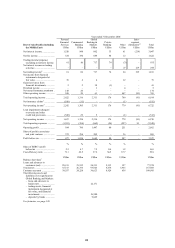

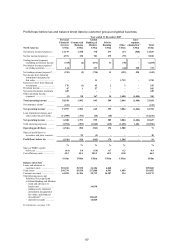

Global Banking and Markets in North

America reported a pre-tax loss of US$965 million,

compared with a profit of US$423 million in 2006.

Improvements across most businesses were

overwhelmed by significant losses in mortgages,

mortgage-backed securities and structured credit

products held for trading, which were driven by

widening credit spreads following the deterioration

in credit markets in the second half of 2007. In

addition, leveraged and acquisition finance recorded

write-downs on underwriting positions held.

Total operating income of US$645 million was

69 per cent lower than 2006, reflecting the impact of

the above-mentioned losses and write-downs, partly

offset by higher net interest income from corporate

lending and increased deposit balances in payments

and cash management.

The 38 per cent rise in net interest income partly

reflected increased lending driven by client demand

and higher outstanding unsyndicated loan balances

in financing and capital markets.

Payments and cash management delivered a

43 per cent increase in net interest income as a result

of growth in demand deposits, and a 15 per cent

increase in transaction fees as higher volumes were

generated from a wider range of product offerings.

Net fee income was 6 per cent ahead of 2006.

Apart from the growth in payments and cash

management referred to above, a strong performance

in HSBC Global Asset Management reflected

favourable market conditions in the first half of

the year.

Trading losses of US$734 million compared

with income of US$818 million in 2006. The decline

was driven by write-downs in credit and structured

derivatives, as detailed above, including

US$282 million relating to monoline exposures, of

which those below investment grade have been fully

written down. These losses were only partly offset

by strong foreign exchange revenues where trading

volumes benefited from market volatility and

positioning against a weakening US dollar. Trading

income from the rates business also increased, driven

by investor demand for lower risk products.

The credit market dislocation also led to an

adverse fair value adjustment for loan commitments

outstanding when global credit spreads widened in

the second half of the year. Including this and the

credit and structured derivatives write-downs

referred to above, the total write-down was

US$1.4 billion.

The benign corporate credit environment

experienced in recent years continued and

impairment charges were low, albeit higher

than in 2006.

Operating expenses declined by 5 per cent,

mainly as a result of reduced performance-related

remuneration resulting from lower revenues.

Expenses were also reduced by savings initiatives

started in late 2006 and early 2007 though these

were offset by the restructuring costs associated

with the Group’s exit from the mortgage-backed

securities business.

Private Banking reported a pre-tax profit

of US$174 million. Excluding a US$39 million

geographical reclassification, the underlying

increase was 27 per cent, reflecting improvements

in Bermuda and the US, the addition of Private

Banking in Canada and a one-off gain from the sale

of Wealth and Tax Advisory Services (‘WTAS’) to

its management. The revenue growth was partially

offset by increased costs from the launch of Private