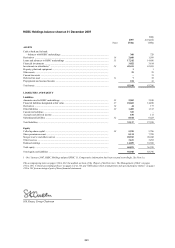

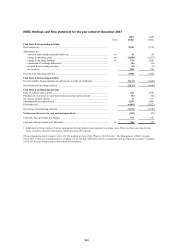

HSBC 2007 Annual Report Download - page 349

Download and view the complete annual report

Please find page 349 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

347

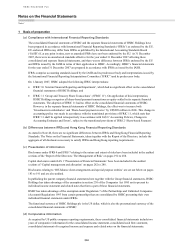

• changes in a parent’s ownership interest in a subsidiary that do not result in a change of control are treated

as transactions between equity holders and reported in equity; and

• An option is available, on a transaction-by-transaction basis, to measure any non-controlling interests

(previously referred to as minority interests) in the entity acquired either at fair value, or at the non-

controlling interest’s proportionate share of the net identifiable assets of the entity acquired.

The effect that the changes will have on the results and financial position of HSBC will depend on the incidence

and timing of business combinations occurring on or after 1 January 2010.

The IASB issued amendments to IAS 32 ‘Financial Instruments: Presentation’ and IAS 1 ‘Presentation

of Financial Statements’, – ‘Puttable Financial Instruments and Obligations Arising on Liquidation’, on

14 February 2008. The amendments are applicable for annual periods beginning on or after 1 January 2009.

HSBC is currently assessing the effect of the amendments, if any, on the consolidated financial statements.

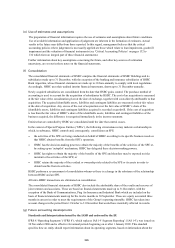

2 Summary of significant accounting policies

(a) Interest income and expense

Interest income and expense for all financial instruments except for those classified as held for trading or

designated at fair value (other than debt securities issued by HSBC and derivatives managed in conjunction with

such debt securities issued) are recognised in ‘Interest income’ and ‘Interest expense’ in the income statement

using the effective interest method. The effective interest method is a way of calculating the amortised cost of a

financial asset or a financial liability (or groups of financial assets or financial liabilities) and of allocating the

interest income or interest expense over the relevant period.

The effective interest rate is the rate that exactly discounts estimated future cash receipts or payments through

the expected life of the financial instrument or, where appropriate, a shorter period, to the net carrying amount of

the financial asset or financial liability. When calculating the effective interest rate, HSBC estimates cash flows

considering all contractual terms of the financial instrument but not future credit losses. The calculation includes

all amounts paid or received by HSBC that are an integral part of the effective interest rate of a financial

instrument, including transaction costs and all other premiums or discounts.

Interest on impaired financial assets is calculated by applying the original effective interest rate of the financial

asset to the carrying amount as reduced by any allowance for impairment.

(b) Non-interest income

HSBC earns fee income from a diverse range of services provided to its customers. Fee income is accounted for

as follows:

− income earned on the execution of a significant act is recognised as revenue when the act is completed (for

example, fees arising from negotiating, or participating in the negotiation of, a transaction for a third party,

such as the arrangement for the acquisition of shares or other securities);

− income earned from the provision of services is recognised as revenue as the services are provided (for

example, asset management, portfolio and other management advisory and service fees); and

− income which forms an integral part of the effective interest rate of a financial instrument is recognised as

an adjustment to the effective interest rate (for example, certain loan commitment fees) and recorded in

‘Interest income’ (Note 2a).

Net trading income comprises all gains and losses from changes in the fair value of financial assets and

financial liabilities held for trading, together with related interest income, expense and dividends.

Net income from financial instruments designated at fair value includes all gains and losses from changes in

the fair value of financial assets and financial liabilities designated at fair value through profit or loss. Interest

income and expense and dividend income arising on these financial instruments are also included, except for

debt securities issued and derivatives managed in conjunction with debt securities issued. Interest on these

instruments is presented in ‘Interest expense’.

Dividend income is recognised when the right to receive payment is established. This is the ex-dividend date for

equity securities.