HSBC 2007 Annual Report Download - page 226

Download and view the complete annual report

Please find page 226 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

HSBC HOLDINGS PLC

Report of the Directors: The Management of Risk (continued)

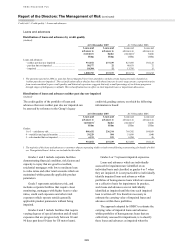

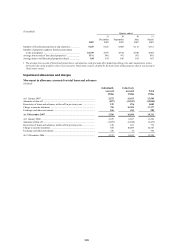

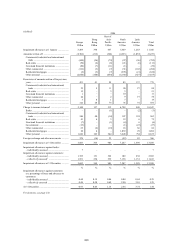

Credit risk > Credit quality > Loans and advances

224

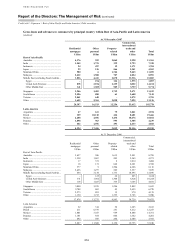

Loans and advances

Distribution of loans and advances by credit quality

(Audited)

At 31 December 2007 At 31 December 2006

Loans and

advances to

customers

Loans and

advances to

banks

Loans and

advances to

customers1

Loans and

advances to

banks

US$m US$m US$m US$m

Loans and advances:

– neither past due nor impaired ................................ 931,872 237,339 827,495 185,125

– past due but not impaired ...................................... 50,577 22 40,431 72

– impaired ................................................................. 18,304 12 13,785 15

1,000,753 237,373 881,711 185,212

1 The amounts reported in 2006 as ‘past due but not impaired’ have been amended to include certain loans previously classified as

‘neither past due nor impaired’. The reclassification reflects the fact that, while these loans are in early-stage arrears, a proportion arise

from events unrelated to poor credit quality, and historical experience suggests that only a small percentage of such loans progresses

through stages of delinquency to default. This reclassification has no effect on total impaired loans or impairment allowances.

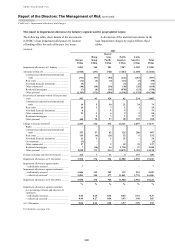

Distribution of loans and advances neither past due nor impaired

(Audited)

The credit quality of the portfolio of loans and

advances that were neither past due nor impaired can

be assessed by reference to the Group’s legacy

credit risk grading system, on which the following

information is based:

At 31 December 2007 At 31 December 2006

Loans and

advances to

customers1

Loans and

advances to

banks

Loans and

advances to

customers1

Loans and

advances to

banks

US$m US$m US$m US$m

Grades:

1 to 3 – satisfactory risk ........................................... 886,432 236,314 769,392 184,059

4 – watch list and special mention ........................... 39,229 504 51,899 1,040

5 – sub-standard but not impaired ............................ 6,211 521 6,204 26

931,872 237,339 827,495 185,125

1 The majority of the loans and advances to customers that are operating within revised terms following restructuring, for details of which

see ‘Renegotiated loans’ below, are included in this table.

Grades 1 and 2 include corporate facilities

demonstrating financial condition, risk factors and

capacity to repay that are good to excellent,

residential mortgages with low to moderate loan

to value ratios and other retail accounts which are

maintained within generally applicable product

parameters.

Grade 3 represents satisfactory risk, and

includes corporate facilities that require closer

monitoring, mortgages with higher loan to value

ratios, credit card exposures and other retail

exposures which operate outside generally

applicable product parameters without being

impaired.

Grades 4 and 5 include facilities that require

varying degrees of special attention and all retail

exposures that are progressively between 30 and

90 days past due (60 days for US motor loans).

Grades 6 or 7 represent impaired exposures.

Loans and advances which are individually

assessed for impairment are identified on an

individual basis and classified as grades 6 or 7 when

they are impaired. It is not practicable to individually

identify impaired loans and advances within

portfolios of homogeneous loans which are assessed

on a collective basis for impairment. In practice,

such loans and advances are not individually

identified as impaired until the time each impaired

loan is written off. It is therefore necessary to

estimate the carrying value of impaired loans and

advances within these portfolios.

The approach adopted by HSBC to estimate the

carrying value of impaired loans and advances

within portfolios of homogeneous loans that are

collectively assessed for impairment, is to classify

these loans and advances as impaired when the