HSBC 2007 Annual Report Download - page 230

Download and view the complete annual report

Please find page 230 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

HSBC HOLDINGS PLC

Report of the Directors: The Management of Risk (continued)

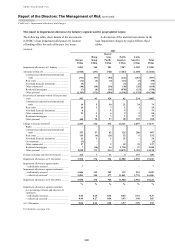

Credit risk > Credit quality > Renegotiated loans / Impairment allowances and charges

228

product, and the availability of empirically based

data. Criteria vary between products, but typically

include: receipt of one or more qualifying payments

within a certain period, a minimum lapse of time

from origination before restructuring may occur, and

restrictions on the number and/or frequency of

successive restructurings. When empirical evidence

indicates an increased propensity to default on

restructured accounts, the use of roll rate

methodology ensures this factor is taken into account

when calculating impairment allowances.

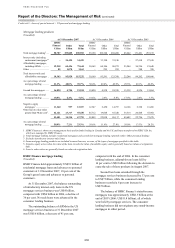

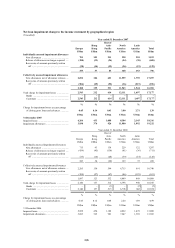

Renegotiated loans that would otherwise be

past due or impaired totalled US$28 billion at

31 December 2007 (2006: US$21 billion).

Restructuring is most commonly applied to

consumer finance portfolios. The largest

concentration was in the US and amounted to

US$24 billion (2006: US$17 billion) or 86 per cent

(2006: 81 per cent) of the Group’s total renegotiated

loans. The increase was due to a significant

deterioration in credit quality in the US. Most

restructurings in the US related to loans secured

on real estate.

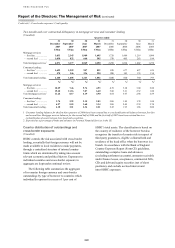

US loan modifications

(Unaudited)

In October 2006, as part of its efforts to mitigate risk

in the affected components of the mortgage services

portfolio in the US, HSBC Finance established a

new programme specifically designed to meet the

needs of selected customers with ARMs. HSBC

Finance is proactively calling and writing to

customers who have ARM loans nearing their first

reset that HSBC Finance expects will be the most

affected by a rate adjustment. By a variety of means,

HSBC Finance assesses the customer’s ability to

make the adjusted payment and, as appropriate and

in accordance with defined policies, HSBC Finance

modifies the loans, allowing time for the customer to

seek alternative financing or improve their individual

situation. These loan modifications primarily provide

for temporary interest rate relief for 12 months by

either maintaining the current interest rate for the

entire 12-month period or resetting the interest rate

for the 12-month period to a rate lower than that

originally required at the reset date. At the end of the

12-month period, the interest rate on the loan will

reset in accordance with the original loan terms,

unless the borrower qualifies for, and is granted, a

further modification. In 2007, HSBC Finance made

more than 33,000 outbound contacts and modified

more than 8,500 loans with an aggregate balance of

US$1.4 billion. Since the inception of this

programme, HSBC Finance has made more than

41,000 outbound contacts and modified more than

10,300 loans with an aggregate balance of

US$1.6 billion. These loans are not included in the

figures quoted above, because HSBC Finance has

not reset delinquency on them as they were not

contractually delinquent at the time of the

modification. However, loans which have been

restructured in the past for other reasons are included

in the figures above. HSBC Finance also continues

to manage a Foreclosure Avoidance Programme for

delinquent consumer lending customers designed to

provide relief to qualifying home owners by either

loan restructuring or modification. HSBC Finance

also supports a variety of national and local efforts

in home ownership preservation and foreclosure

avoidance.

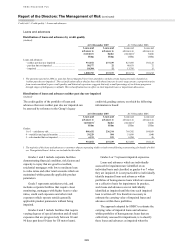

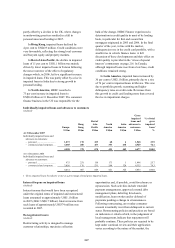

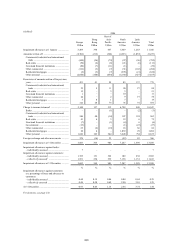

Collateral and other credit enhancements

obtained

(Audited)

HSBC obtained assets by taking possession of

collateral held as security, or calling upon other

credit enhancements, as follows:

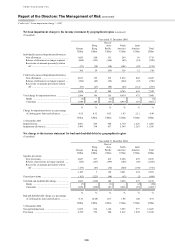

(Audited)

Carrying amount

obtained in:

2007 2006

US$m US$m

Nature of assets

Residential property ................. 2,509 1,716

Commercial and industrial

property ................................ 18 6

Other ........................................ 373 215

2,900 1,937

Repossessed properties are made available for

sale in an orderly fashion, with the proceeds used to

reduce or repay the outstanding indebtedness. Where

excess funds are available after the debt has been

repaid, they are available either for other secured

lenders with lower priority or are returned to the

customer. HSBC does not generally occupy

repossessed properties for its business use. The

majority of repossessed properties arose in the US in

HSBC Finance, which experienced higher levels of

foreclosure and higher losses on sale due to

declining house prices. The average time taken to

sell a foreclosed property in the US during 2007 was

184 days and the average loss on sale was 11 per

cent. A quarterly breakdown is provided below: