HSBC 2007 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

HSBC HOLDINGS PLC

Report of the Directors: Business Review (continued)

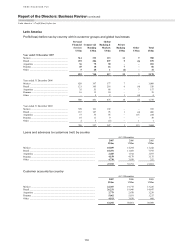

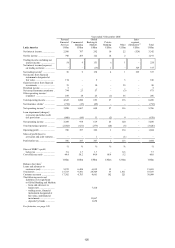

Latin America > 2006

120

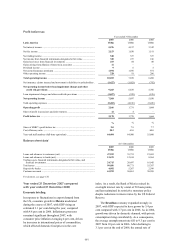

in transactions from non-HSBC customers. Growth in

mutual fund fees was mainly driven by higher sales

volumes and expanded product offerings in the

stronger economic environment.

Fee income in Brazil rose by 25 per cent, largely

from increased current account fees, reflecting

growth in customer numbers, greater transaction

volumes and re-pricing initiatives. Higher payroll and

vehicle balances also led to increased fees from

lending activities. In Argentina, higher credit card

fees from balance growth, re-pricing initiatives on

savings accounts, and the discontinuance of a free

current account promotion led to an improvement in

fee income.

Across the region, HSBC’s insurance businesses

continued to perform well. Sales of insurance

products in Mexico remained strong, with increased

cross-selling through the branch network of simple

insurance products together with other Personal

Financial Services products containing insurance

components. This led to a 19 per cent rise in net

premiums, mainly in respect of individual life

insurance products. In Brazil, excluding the effect of

the property and casualty insurance business sold in

2005, insurance revenues rose, largely from life and

pension products. In Argentina, increased advertising,

partnerships with established local consumer brands

and internal cross-selling initiatives led to a rise in

motor, home and extended-warranty insurance

premium income. Life and annuity premiums also

increased in line with higher customer salaries. The

‘Maxima’ pension funds business delivered higher

revenues helped by improvements in the economic

climate and greater levels of employment.

Lower other operating income reflected the non-

recurrence of profit on the sale of HSBC’s Brazilian

property and casualty insurance business.

Loan impairment charges and other credit risk

provisions rose by 15 per cent to US$764 million as

lending grew and the loan book seasoned. In Mexico,

the higher charge was primarily driven by the growth

in credit card lending. In Brazil, loan impairment

charges increased modestly, driven by growth in

vehicle finance, instalment loans (credito parcelado)

and credit card lending. As the credit environment

weakened during the first half of the year, various

measures were taken to mitigate the effects. These

included tightening lending criteria, enhancing credit

analytics, revising the collection policy, prioritising

secured lending ahead of unsecured advances and

strengthening credit operations. Following

implementation of these measures, several key credit

indicators showed improvement.

Operating expenses rose by 10 per cent. In

Mexico, expense growth of 10 per cent was mainly

driven by increased staff costs. This largely reflected

the recruitment of 2,200 employees to improve

customer service levels in branches and grow sales.

Incentive costs increased as profits rose, and

marketing costs grew as a result of various

promotional campaigns. The continued expansion

of the branch network and ATM infrastructure,

together with the new HSBC headquarters building

in Mexico City, led to increases in IT, premises and

equipment costs.

In Brazil, expenses were 10 per cent higher. As

in Mexico, this reflected the cost of new employees

recruited to support business expansion, including the

strengthening of credit operations, and new branch

openings. This, together with annual pay rises and

increased incentive payments, triggered a 13 per cent

growth in staff costs. Advertising costs rose to

promote brand awareness, while an HSBC Premier

promotion led to higher marketing costs.

Costs grew by 26 per cent in Argentina, with

higher staff costs driven by union-agreed pay rises in

2005, and increased incentives and commissions paid

in light of revenue growth. Marketing costs also

increased to support the launch of various promotions

and campaigns.

Commercial Banking reported pre-tax profits of

US$451 million, 17 per cent higher than in 2005.

Growth in net operating income before loan

impairment charges was strong at 26 per cent as

domestic economies in the region grew and HSBC

built market share. Cost growth in support of this

expansion was held within revenue growth and the

cost efficiency ratio improved by 2.5 per cent.

Net interest income rose by 24 per cent, largely

driven by business expansion in Mexico and Brazil.

In Mexico, net interest income rose by 49 per

cent, reflecting asset and deposit growth, in part due

to the transfer of the 56,000 customers from Personal

Financial Services noted above. As HSBC extended

its presence in the small and middle market business

segments, average deposit balances increased by

65 per cent (31 per cent excluding the transferred

customer accounts), although the benefit of this

volume growth was partly mitigated by lower deposit

spreads in a falling rate environment.

Lending balances in Mexico were 41 per cent

higher, primarily driven by strong demand in the

rapidly growing real estate and residential

construction sectors. During the final quarter of the

year, HSBC opened an International Banking Centre

to develop cross-border business for global