HSBC 2007 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

HSBC HOLDINGS PLC

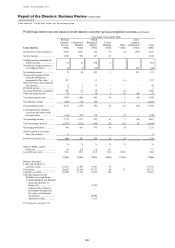

Report of the Directors: Business Review (continued)

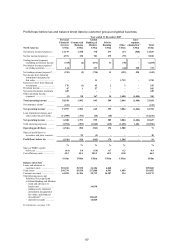

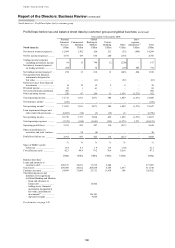

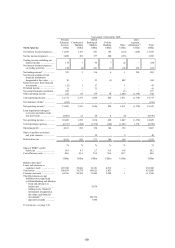

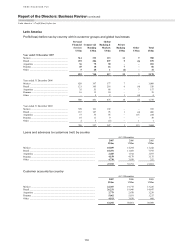

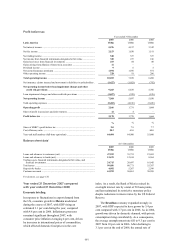

Latin America > 2007

114

In Brazil, fee income rose by 3 per cent on

the back of growth in lending balances and a

commensurate rise in credit facility fees. Fee

income further benefited from re-pricing initiatives,

particularly in current account fees.

Fee income in Argentina, higher by 12 per cent,

primarily reflected an extra four months of Banca

Nazionale revenues. Business growth in

bancassurance and credit cards also contributed

to improved fees.

The continued growth of insurance operations in

the region, through increased product offerings and

expanded distribution channels, led to higher

insurance premiums and claims.

In Mexico, increased cross-selling activities in

the branch network resulted in higher net insurance

income, mainly driven by sales of a five-year life

assurance product. Refinement of the recognition

methodology used in respect of the PVIF long-term

insurance contracts resulted in a one-off revenue

increment in the first half of 2007.

In Brazil, income grew from higher sales

volumes of pension and life assurance products. The

growth in the life portfolio was driven by growth of

106 per cent in credit insurance products. Pension

portfolio income grew by 48 per cent following

targeted sales initiatives. Net insurance claims also

grew substantially during the year. Increased

premium income in Argentina was generated from

higher sales volumes of general insurance and life

protection policies, supported by innovative

marketing campaigns.

Net gains from financial investments increased

significantly, driven by a gain of US$97 million,

following a sale of shares held in a credit bureau, a

stock exchange and a derivatives exchange in Brazil.

Loan impairment charges rose by 70 per cent

to US$1.5 billion, mainly due to higher delinquency

from seasoned loan growth in Mexico.

Mexico reported a more than threefold increase

in loan impairment charges to US$737 million,

driven by higher impairments on credit cards

following the targeted expansion in market share, and

higher delinquencies from self-employed loan

balances. The increase in loan impairment charge is

part of the cost of building strong organic growth as

portfolios season. Regular reviews are undertaken to

improve the quality of new business, based on

underwriting experience, improved collection

strategies and better managed customer acquisition

channels. Credit models were updated during 2007 to

adjust to credit behaviour in underlying portfolios.

Loan impairment charges rose only modestly

in Brazil, notwithstanding strong asset growth,

reflecting the benign credit environment and the

application of proactive risk management techniques.

Increased loan impairment charges from the vehicle

finance, cards, payroll loans and store loans

portfolios were partially offset by lower loan

impairment charges in overdrafts and personal loans.

In Argentina, loan impairment charges grew by

US$14 million, again mainly due to the inclusion of

the Banca Nazionale portfolio, as well as organic

loan growth.

Operating expenses of US$3.8 billion were

12 per cent higher, mainly because of activities

undertaken in support of product and distribution

expansion initiatives, and integrating recent

acquisitions.

In Mexico, operating expenses increased by

14 per cent, as non-staff costs rose to support organic

business growth. Staff costs were flat as increases to

support business growth, mainly in debt collection

and call centres, were offset by one-off curtailment

and settlement gains from staff transferring out of the

bank’s defined benefit healthcare scheme to a new

defined contribution scheme. Growth in non-staff

costs was mainly attributable to supporting credit

card business growth and servicing, strengthening of

IT infrastructure and higher marketing spend on

product campaigns, promotions and sponsorships.

Campaigns included the HSBC Premier relaunch,

Tu Cuenta and insurance. The increased popularity of

the cash-back facility on the Tu Cuenta account,

where a customer receives a rebate on amounts spent

by credit or debit cards, also drove up expenses.

In Brazil, operating expenses were 8 per cent

higher. Staff costs included one-off expenditure

incurred to enable the business to improve

operational efficiencies and position itself for future

growth. Union-agreed pay rises took effect during

2007. Non-staff expenses, including marketing

campaigns, payroll acquisition costs and transactional

taxes also increased in support of revenue growth.

Costs in Argentina rose by 39 per cent, mainly

from the inclusion of four extra months of Banca

Nazionale costs. The rise in expenses reflected both

continued investment in infrastructure to support

business growth, and general price rises evident in

the economy as inflation rose. Increased marketing

campaign spending was focused on cards, personal

loans and the Premier relaunch.

Commercial Banking pre-tax profits rose by

46 per cent to US$740 million during 2007, mainly

driven by significant growth in Brazil and Mexico.