HSBC 2007 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2007 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

|

|

HSBC HOLDINGS PLC

Report of the Directors: Business Review (continued)

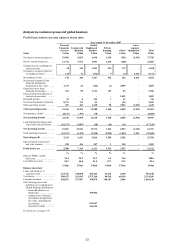

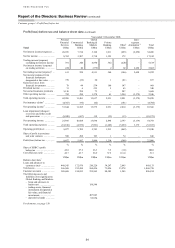

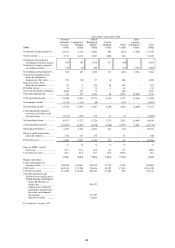

Competitive environment

38

Advances in technology

Customer transaction volumes continue to grow at a

rate considerably ahead of the growth in underlying

balances or accounts, leading many banks to seek to

reduce unit costs per service transaction in order to

maintain margins. The deployment of automated

secure transaction channels requires significant

investment, providing a competitive advantage to

banks with larger scale. Despite widespread adoption

by both banks and customers of new distribution

channels, the expected reduction in volumes of

transactions through traditional channels has been

slow to materialise and many banking customers

continue to prefer to use them. The younger

generation of customers, however, tends to be more

comfortable with system-aided self-service,

particularly for savings accounts, credit cards and

simple investments. HSBC expects the sophistication

of products sold in direct channels and adoption rates

to increase, as the use of 24-hour self-service

channels, such as ATMs, internet, mobile, and voice

response units becomes increasingly commonplace.

Regulation

Initiatives such as Basel II, together with the

increasingly international scope of financial services,

have raised the level of cooperation between

regulatory authorities in different countries.

Enhanced understanding of how risks are originated

and dispersed in modern financial markets has

reinforced the need to address how best to regulate

the increasingly integrated and international nature

of banking and financial services; this has been

evidenced most recently in coordinated discussions

on the global liquidity disruption. In addition, the

enlargement of the EU, the introduction of the

Markets in Financial Instruments Directive

(‘MIFID’) and the continued effort to endorse

consistent standards and enforcement has

encouraged regulatory bodies to work together more

closely. Interaction and cooperation have led to

competitive and regulatory issues emerging in one

country rapidly being taken up in other jurisdictions.

Uniform global standards, however, continue to be

complicated by differing local interpretations, or

additional local regulation.

Regional factors

Europe

Across Europe, in all sectors, HSBC competes with a

growing range of institutions. These markets are

characterised by rapid innovation, margin

compression through competition and a constant

flow of new entrants. Regulators monitor the

financial services sector closely and conduct reviews

into the long-term evolution of the industry.

Legislators are enforcing legislation with the aim of

improving competition and protecting consumers.

In November 2007, the European Commission

announced that in order to improve the

competitiveness and efficiency of European retail

financial services markets, reviews would be

undertaken to improve customer choice and mobility

within the single market; better facilitate retail

insurance markets; achieve progress towards

adequate and consistent rules for the distribution of

retail investment products; and promote financial

education, financial inclusion and adequate redress

for consumers.

Following a long running investigation, the

Competition Directorate-General determined that

MasterCard’s multilateral interchange fees for cross-

border payment card transactions violate EU

competition rules. MasterCard has six months to

comply or respond. HSBC is fully engaged in the

case through its membership of MasterCard.

A number of key EU measures intended to

facilitate development of the single market and

increase competition came into effect during the

year; principally, transposition of the Markets in

Financial Instruments Directive in November 2007.

Implementation of phase 1 of the Single Euro

Payments Area programme occurred in January

2008.

UK

Financial services, including retail banking, is a

highly competitive sector in the UK, led by several

national and international institutions which compete

on both price and service quality. Domestic

acquisitions or mergers are limited. The sector is

closely regulated, and a series of investigations with

particular relevance to Personal Financial Services

remain in progress.

In July 2007, a group of seven banks (including

HSBC) and one building society announced that they

had agreed with the Office of Fair Trading (‘OFT’)

that the legal status and enforceability of certain of

the charges applied to their personal customers in

relation to unauthorised overdrafts should be tested

in the High Court. Certain preliminary issues in the

case came before the High Court in a trial starting

in January 2008 and this part of the case concluded

in February 2008. At the date of this report,

judgement in the case is awaited. The OFT is also

conducting a market study into competition for

personal current accounts.