Xerox 2014 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2014 Xerox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

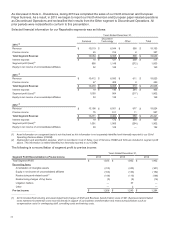

Impairment of Long-Lived Assets

We review the recoverability of our long-lived assets, including buildings, equipment, internal use software and other

intangible assets, when events or changes in circumstances occur that indicate that the carrying value of the asset

may not be recoverable. The assessment of possible impairment is based on our ability to recover the carrying value

of the asset from the expected future pre-tax cash flows (undiscounted and without interest charges) of the related

operations. If these cash flows are less than the carrying value of such asset, an impairment loss is recognized for

the difference between estimated fair value and carrying value. Our primary measure of fair value is based on

discounted cash flows.

Pension and Post-Retirement Benefit Obligations

We sponsor defined benefit pension plans in various forms in several countries covering employees who meet

eligibility requirements. Retiree health benefit plans cover U.S. and Canadian employees for retiree medical costs.

We employ a delayed recognition feature in measuring the costs of pension and post-retirement benefit plans. This

requires changes in the benefit obligations and changes in the value of assets set aside to meet those obligations to

be recognized not as they occur, but systematically and gradually over subsequent periods. All changes are

ultimately recognized as components of net periodic benefit cost, except to the extent they may be offset by

subsequent changes. At any point, changes that have been identified and quantified but not recognized as

components of net periodic benefit cost, are recognized in Accumulated Other Comprehensive Loss, net of tax.

Several statistical and other factors that attempt to anticipate future events are used in calculating the expense,

liability and asset values related to our pension and retiree health benefit plans. These factors include assumptions

we make about the discount rate, expected return on plan assets, rate of increase in healthcare costs, the rate of

future compensation increases and mortality. Actual returns on plan assets are not immediately recognized in our

income statement due to the delayed recognition requirement. In calculating the expected return on the plan asset

component of our net periodic pension cost, we apply our estimate of the long-term rate of return on the plan assets

that support our pension obligations, after deducting assets that are specifically allocated to Transitional Retirement

Accounts (which are accounted for based on specific plan terms).

For purposes of determining the expected return on plan assets, we utilize a market-related value approach in

determining the value of the pension plan assets, rather than a fair market value approach. The primary difference

between the two methods relates to systematic recognition of changes in fair value over time (generally two years)

versus immediate recognition of changes in fair value. Our expected rate of return on plan assets is applied to the

market-related asset value to determine the amount of the expected return on plan assets to be used in the

determination of the net periodic pension cost. The market-related value approach reduces the volatility in net

periodic pension cost that would result from using the fair market value approach.

The discount rate is used to present value our future anticipated benefit obligations. The discount rate reflects the

current rate at which benefit liabilities could be effectively settled considering the timing of expected payments for

plan participants. In estimating our discount rate, we consider rates of return on high-quality fixed-income

investments adjusted to eliminate the effects of call provisions, as well as the expected timing of pension and other

benefit payments.

Each year, the difference between the actual return on plan assets and the expected return on plan assets, as well

as increases or decreases in the benefit obligation as a result of changes in the discount rate and other actuarial

assumptions, are added to or subtracted from any cumulative actuarial gain or loss from prior years. This amount is

the net actuarial gain or loss recognized in Accumulated other comprehensive loss. We amortize net actuarial gains

and losses as a component of net pension cost for a year if, as of the beginning of the year, that net gain or loss

(excluding asset gains or losses that have not been recognized in market-related value) exceeds 10% of the greater

of the projected benefit obligation or the market-related value of plan assets (the "corridor" method). This

determination is made on a plan-by-plan basis. If amortization is required for a particular plan, we amortize the

applicable net gain or loss in excess of the 10% threshold on a straight-line basis in net periodic pension cost over

the remaining service period of the employees participating in that pension plan. In plans where substantially all

participants are inactive, the amortization period for the excess is the average remaining life expectancy of the plan

participants.

Our primary domestic plans allow participants the option of settling their vested benefits through the receipt of a

lump-sum payment. The participant's vested benefit is considered fully settled upon payment of the lump-sum. We

have elected to apply settlement accounting and therefore we recognize the losses associated with settlements in

this plan immediately upon the settlement of the vested benefits. Settlement accounting requires us to recognize a

pro rata portion of the aggregate unamortized net actuarial losses upon settlement. The pro rata factor is computed

75