Wells Fargo 2010 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2010 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

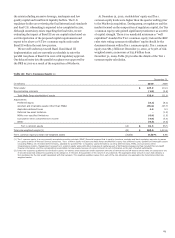

|

|

securities and capital markets by the SEC; (v) establishes the

Bureau of Consumer Financial Protection within the FRB, which

will have sweeping powers to administer and enforce a new

federal regulatory framework of consumer financial regulation;

(vi) may limit the existing pre-emption of state laws with respect

to the application of such laws to national banks, makes federal

pre-emption no longer applicable to operating subsidiaries of

national banks, and gives state authorities, under certain

circumstances, the ability to enforce state laws and federal

consumer regulations against national banks; (vii) provides for

increased regulation of residential mortgage activities; (viii)

revises the FDIC's assessment base for deposit insurance by

changing from an assessment base defined by deposit liabilities

to a risk-based system based on total assets; (ix) authorizes the

FRB to issue regulations regarding the amount of any

interchange transaction fee that an issuer may receive to ensure

that it is reasonable and proportional to the cost incurred; and

(x) includes several corporate governance and executive

compensation provisions and requirements, including

mandating an advisory stockholder vote on executive

compensation.

Although the Dodd-Frank Act became generally effective in

July 2010, many of its provisions have extended implementation

periods and delayed effective dates and will require extensive

rulemaking by regulatory authorities as well as require more

than 60 studies to be conducted over the next one to two years.

Accordingly, in many respects the ultimate impact of the Dodd-

Frank Act and its effects on the U.S. financial system and the

Company will not be known for an extended period of time.

Nevertheless, the Dodd-Frank Act, including future rules

implementing its provisions and the interpretation of those rules,

could result in a loss of revenue, require us to change certain of

our business practices, limit our ability to pursue certain

business opportunities, increase our capital requirements and

impose additional assessments and costs on us, and otherwise

adversely affect our business operations and have other negative

consequences, including to our credit ratings to the extent the

legislation reduces the probability of future Federal financial

assistance or support currently assumed by the rating agencies in

their credit ratings. A reduction in one or more of our credit

ratings could adversely affect our ability to borrow funds and

raise the costs of our borrowings substantially and could cause

creditors and business counterparties to raise collateral

requirements or take other actions, which could adversely affect

our ability to raise capital.

Recently, the Obama Administration delivered a report to

Congress regarding proposals to reform the housing finance

market in the United States. The report, among other things,

outlined various potential proposals to wind down the GSEs and

reduce or eliminate over time the role of the GSEs in

guaranteeing mortgages and providing funding for mortgage

loans, as well as proposals to implement reforms relating to

borrowers, lenders, and investors in the mortgage market,

including reducing the maximum size of a loan that the GSEs can

guarantee, phasing in a minimum down payment requirement

for borrowers, improving underwriting standards, and increasing

accountability and transparency in the securitization process.

The extent and timing of any regulatory reform regarding the

GSEs and the home mortgage market, as well as any effect on the

Company’s business and financial results, are uncertain.

Any other future legislation and/or regulation, if adopted,

also could have a material adverse effect on our business

operations, income, and/or competitive position and may have

other negative consequences.

For more information, refer to the “Regulation and

Supervision” section in our 2010 Form 10-K.

Bank regulators and other regulations, including

proposed Basel capital standards and FRB guidelines,

may require higher capital levels, limiting our ability to

pay common stock dividends or repurchase our

common stock. Federal banking regulators continually

monitor the capital position of banks and bank holding

companies. In July 2009, the Basel Committee on Bank

Supervision published a set of international guidelines for

determining regulatory capital known as Basel III. These

guidelines, which were finalized in December 2010, followed

earlier guidelines by the Basel Committee and are designed to

address many of the weaknesses identified in the banking sector

as contributing to the financial crisis of 2008 - 2010 by, among

other things, increasing minimum capital requirements,

increasing the quality of capital, increasing the risk coverage of

the capital framework, and increasing standards for the

supervisory review process and public disclosure.

In 2010, the FRB issued guidelines for evaluating proposals

by large bank holding companies, including the Company, to

undertake capital actions in 2011, such as increasing dividend

payments or repurchasing or redeeming stock. Pursuant to those

FRB guidelines, the Company submitted a proposed Capital Plan

Review to the FRB. The FRB is expected to undertake these

capital plan reviews on a regular basis in the future. There can be

no assurance that the FRB will respond favorably to the

Company’s current Capital Plan Review, or future capital plan

reviews, and the FRB, the Basel standards or other regulatory

capital requirements may limit or otherwise restrict how we

utilize our capital, including common stock dividends and stock

repurchases. Although not currently anticipated, our regulators

may require us to raise additional capital in the future. Issuing

additional common stock may dilute existing stockholders.

Bankruptcy laws may be changed to allow mortgage

“cram-downs,” or court-ordered modifications to our

mortgage loans including the reduction of principal

balances. Under current bankruptcy laws, courts cannot force

a modification of mortgage and home equity loans secured by

primary residences. In response to the current financial crisis,

legislation has been proposed to allow mortgage loan “cram-

downs,” which would empower courts to modify the terms of

mortgage and home equity loans including a reduction in the

principal amount to reflect lower underlying property values.

This could result in writing down the balance of our mortgage

and home equity loans to reflect their lower loan values. There is

also risk that home equity loans in a second lien position (i.e.,

behind a mortgage) could experience significantly higher losses

to the extent they become unsecured as a result of a cram-down.

The availability of principal reductions or other modifications to

93