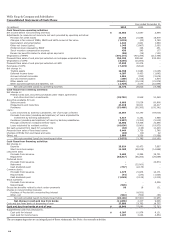

Wells Fargo 2010 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2010 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

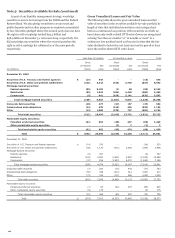

Note 1: Summary of Significant Accounting Policies (continued)

• repayment is deemed to be protracted beyond reasonable

time frames;

• the loan has been classified as a loss by either our internal

loan review process or our banking regulatory agencies;

• the customer has filed bankruptcy and the loss becomes

evident owing to a lack of assets; or

• the loan is 180 days past due unless both well-secured and

in the process of collection.

For consumer loans, our charge-off policies are as follows:

• 1-4 family first and junior lien mortgages – We generally

charge down to net realizable value when the loan is

180 days past due.

• Auto loans – We generally fully charge off when the loan is

120 days past due.

• Credit card loans – We generally fully charge off when the

loan is 180 days past due.

• Unsecured loans (closed end) – We generally charge off

when the loan is 120 days past due.

• Unsecured loans (open end) – We generally charge off when

the loan is 180 days past due.

• Other secured loans – We generally fully or partially charge

down to net realizable value when the loan is 120 days past

due.

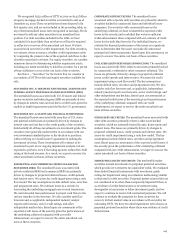

IMPAIRED LOANS We consider a loan to be impaired when,

based on current information and events, we determine that we

will not be able to collect all amounts due according to the loan

contract, including scheduled interest payments. Our impaired

loans include commercial and industrial, commercial real estate

(CRE), and foreign loans on nonaccrual status for which we

determine that we will not be able to collect all amounts due and

consumer, commercial and industrial, CRE, and foreign loans

modified in a TDR, on both accrual and nonaccrual status.

When we identify a loan as impaired, we measure the

impairment based on the present value of expected future cash

flows, discounted at the loan’s effective interest rate. When

collateral is the sole source of repayment for the loan, we may

measure impairment based on the fair value of the collateral. If

foreclosure is probable, we use the current fair value of the

collateral less selling costs, instead of discounted cash flows.

If we determine that the value of an impaired loan is less than

the recorded investment in the loan (net of previous charge-offs,

deferred loan fees or costs and unamortized premium or

discount), we recognize impairment. When the value of an

impaired loan is calculated by discounting expected cash flows,

interest income is recognized using the loan’s effective interest

rate over the remaining life of the loan.

TROUBLED DEBT RESTRUCTURINGS (TDRs) In situations

where, for economic or legal reasons related to a borrower’s

financial difficulties, we grant a concession for other than an

insignificant period of time to the borrower that we would not

otherwise consider, the related loan is classified as a TDR. We

strive to identify borrowers in financial difficulty early and work

with them to modify their loan to more affordable terms before it

reaches nonaccrual status. These modified terms may include

rate reductions, principal forgiveness, term extensions, payment

forbearance and other actions intended to minimize our

economic loss and to avoid foreclosure or repossession of the

collateral. For modifications where we forgive principal, the

entire amount of such principal forgiveness is immediately

charged off. Loans classified as TDRs are considered impaired

loans.

PURCHASED CREDIT-IMPAIRED (PCI) LOANS Loans acquired

in a transfer, including business combinations, where there is

evidence of credit deterioration since origination and it is

probable at the date of acquisition that we will not collect all

contractually required principal and interest payments are

accounted for as PCI loans. PCI loans are initially recorded at

fair value, which includes estimated future credit losses expected

to be incurred over the life of the loan. Accordingly, the historical

allowance for credit losses related to these loans is not carried

over. Some loans that otherwise meet the definition as credit-

impaired are specifically excluded from the PCI loan portfolios,

such as revolving loans where the borrower still has revolving

privileges.

Evidence of credit quality deterioration as of the purchase

date may include statistics such as past due and nonaccrual

status, commercial risk ratings, recent borrower credit scores

and recent loan-to-value percentages. Generally, acquired loans

that meet our definition for nonaccrual status are considered to

be credit-impaired.

Substantially all commercial and industrial, CRE and foreign

PCI loans are accounted for as individual loans. Conversely,

Pick-a-Pay and other consumer PCI loans have been aggregated

into several pools based on common risk characteristics. Each

pool is accounted for as a single asset with a single composite

interest rate and an aggregate expectation of cash flows.

Accounting for PCI loans involves estimating fair value, at

acquisition, using the principal and interest cash flows expected

to be collected discounted at the prevailing market rate of

interest. The excess of cash flows expected to be collected over

the carrying value (estimated fair value at acquisition date) is

referred to as the accretable yield and is recognized in interest

income using an effective yield method over the remaining life of

the loan, or pool of loans, in situations where there is a

reasonable expectation about the timing and amount of cash

flows to be collected. The difference between contractually

required payments and the cash flows expected to be collected at

acquisition, considering the impact of prepayments, is referred

to as the nonaccretable difference.

Subsequent to acquisition, we regularly evaluate our

estimates of cash flows expected to be collected. If we have

probable decreases in cash flows expected to be collected (other

than due to decreases in interest rate indices and changes in

prepayment assumptions), we charge the provision for credit

losses, resulting in an increase to the allowance for loan losses. If

we have probable and significant increases in cash flows

expected to be collected, we first reverse any previously

established allowance for loan losses and then increase interest

income as a prospective yield adjustment over the remaining life

of the loan, or pool of loans. Estimates of cash flows are

impacted by changes in interest rate indices for variable rate

116