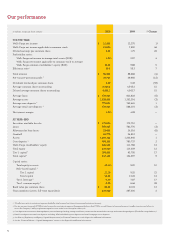

Wells Fargo 2010 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2010 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

|

|

Financial planning and investing: One visit doesn’t do it all

As we stand together with our customers, helping them

manage their investments and plan their financial future,

we’re reminded every day that this isn’t a one-time event any

more than one visit to a doctor’s oce ensures good health.

Our relationships with Wealth, Brokerage and Retirement

customers are built on providing thoughtful, objective, and

frequent advice—understanding each customer’s individual

goals, risk tolerance, and needs, monitoring progress, and

helping them make changes when it’s right for them to doso.

When our customers achieve financial success—however

they define it—then we’ll achieve our goal: becoming the nation’s

most respected provider of wealth, brokerage, and retirement

services. The opportunity to earn more business from our own

customers is enormous. Only nine of every 100 of our banking

households have brokerage relationships with us. Only six of

every 100 have their IRA with us. We want all our investment

customers to bank with us. We want all our banking customers

to think of us first for all their investment needs. Our average

banking household that has a Wealth, Brokerage or Retirement

relationship with us has an average of 9.80products with us

(upfrom 9.67 in first quarter2010).

Wealth Our team-based approach gives our customers access

to experts with deep knowledge and extensive experience in

many disciplines. We manage, administer, or have custody of

$198billion in assets, including $48billion in deposits, for our

high-net-worth clients. Client deposits rose a strong 13percent,

a key measure of our ability to earn more of their business.

Investment management and trust revenue was up 11percent

from 2009 on strong investment results and continued growth

in the trust services provided toclients.

Brokerage We believe every customer should have a financial

plan. WellsFargo Advisors, the nation’s third-largest retail

brokerage network with 15,200 full-service financial advisors

and 4,400 licensed bankers, is helping make that goal a reality.

Today, more than two-thirds of our auent customers have a

financial plan. This year, we grew customer assets 6percent

to $1.2trillion. Managed-account assets, now at $235billion,

rose $38billion, or 20percent. The number of loans originated

through WellsFargo Advisors financial advisors rose 71percent,

totaling $7.2billion.

Retirement Our 2010 Retirement Survey showed that working

in retirement is becoming the norm for middle-class Americans,

the latest evidence that retirement is changing drastically

and that people need help more than ever. We work with

customers as they plan and prepare for their retirement, and

we also administer 401(k), pension, and other retirement plans

for companies. Customer assets in retirement plans that we

administer rose 6percent, or $14billion, to $231billion for the

year. Our national market share rose to 3.7percent (3.1percent

a yearago). We strengthened our rank as one of the nation’s

top-five IRA providers, growing IRA assets 10percent,

or $24billion, to $266billion.

Now the hard part: Making rules that work for America

The Dodd-Frank Wall Street Reform and Consumer Protection

Act may change the landscape of financial services more than

any other law in my three-decade career in the industry. It’s

2,319 pages. (TheSarbanes-Oxley Act of 2002 was 66 pages.

Those were the good olddays!) Its 240 rules will aect checking

accounts, debit cards, credit cards, home loans, and brokerage

accounts. We support any protection for customers nationally

to ensure all financial services providers, not just banks, are

held to the same high standard of responsibility that we’ve tried

to hold ourselves to for almost 160years. Our customers expect

nothing less. We’re working with legislators and regulators

to help make sure thishappens.

Dodd-Frank and other new regulations, however, would

reduce the prices banks can charge for some products. One

example: a reduction of 80percent or more, scheduled to take

eect in July 2011, in the fee banks charge retailers when

customers use their debit cards at the cash register. Government

price controls such as this make no sense. They distort our

market-based, free-enterprise economy. What’s next? Will the

government require car dealers to sell a new vehicle for $5,000

or grocers a gallon of milk for 50cents? Banks should be fairly

compensated for the value that debit cards create for merchants

and their customers by reducing fraud risk and the cost of

carrying cash or handling checks. An 80percent cut in this

fee wouldn’t even enable us to cover the cost of providing

the service.

The key to growing our economy

There are three priorities for our economy. The first is creating

good jobs. The second is creating good jobs. The third is

creating good jobs. Negative home equity, depressed housing

prices, and mortgage foreclosures are not the cause of our

sluggish economy. They’re the result of homeowners losing their

jobs. I started as a loan collector in banking 34years ago. Back

then, when a borrower wasn’t making payments, it usually was

because of divorce, a death in the family, medical emergency

or, most often, unemployment. It’s the same today. Americans

want to pay their bills and will if they have the resources to do

so. The U.S. economy did add a million jobs last year, but that’s

cold comfort to the almost one in every 11 Americans looking

for work. We’re telling all our creditworthy business customers

as often as we can: More credit is available. Many of our

small business and commercial customers have the cash and

resources to rehire and expand, but there’s hesitation because

of the legislative and regulatory landscape, customer spending

habits, and government debt. This can paralyze and confuse

business owners, entrepreneurs, investors, and consumers.

Government and private enterprise need to stand together to

alleviate this uncertainty by promoting fiscal discipline and

economic opportunity.

WellsFargo is hiring. At year-end 2010, we had 6,500

unfilled jobs in our company. We want to create a welcoming

home for talent, a place where team members can build a

varied, challenging, satisfying career that can last a lifetime.

Weconsider team members an asset to invest in, not an

expense to be managed. We invested 3percent of our total

payroll dollars for the year in team member training, an