Volvo 2008 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2008 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

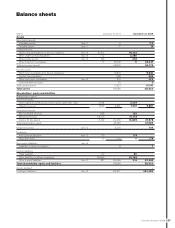

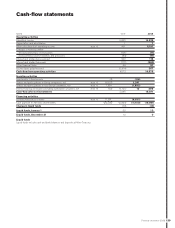

119

Financial information 2008

Currency risks

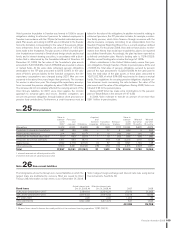

The content of the reported balance sheet may be affected by changes

in different exchange rates. Currency risks in Volvo’s operations are

related to changes in the value of contracted and expected future

payment fl ows (commercial currency exposure), changes in the value

of loans and investments (fi nancial currency exposure) and changes

in the value of assets and liabilities in foreign subsidiaries (currency

exposure of shareholders’ equity). The aim of Volvo’s currency-risk

management is to minimize, over the short term, negative effects on

Volvo’s earnings and fi nancial position stemming from exchange-rate

changes.

Commercial currency exposure

In order to hedge the value of future payment fl ows in foreign curren-

cies, Volvo uses forward contracts and currency options. For each cur-

rency, 75% of the forecast net fl ows for the coming six months are

hedged and 50% for months seven to 12, while contracted fl ows after

12 months shall normally be hedged. As a consequence of the fi nan-

cial turmoil, Volvo will gradually and temporarily shift focus from

hedging forecast fl ows to only hedge contracted fl ows.

The nominal amount of all outstanding forward and option con-

tracts amounted to SEK 73.8 billion (63.1) at December 31, 2008. On

the same date, the fair value of these contracts was negative in an

amount of SEK 2,936 million (positive 266).

The table below presents the effect a change of the value of the

Swedish krona in relation to other currencies would have on the fair

value of outstanding contracts. In reality, currencies usually do not

change in the same direction at any given time, so the actual effect of

exchange-rate changes may differ from the below sensitivity analysis.

Change in value of SEK in relation to

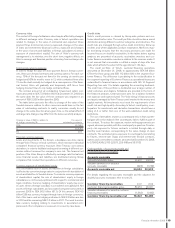

all foreign currencies, %

Fair value of

outstanding contracts

(10) (6,245)

0 (2,936)

10 373

Financial currency exposure

Loans and investments in the Group’s subsidiaries are done mainly

through Volvo Treasury in local currencies, which minimizes individual

companies’ fi nancial currency exposure. Volvo Treasury uses various

derivatives, in order to facilitate lending and borrowing in different cur-

rencies without increase the company’s own risk. The fi nancial net

position of the Volvo Group is affected by exchange rate fl uctuations,

since fi nancial assets and liabilities are distributed among Group

companies that conduct their operations in different currencies.

Currency exposure of shareholders’ equity

The consolidated value of assets and liabilities in foreign subsidiaries

is affected by current exchange rates in conjunction with translation of

assets and liabilities to Swedish kronor. To minimize currency ex posure

of shareholders’ capital, the size of shareholders’ equity in foreign

subsidiaries is continuously optimized with respect to commercial and

legal conditions. Currency hedging of shareholders’ equity may occur

in cases where a foreign subsidiary is considered overcapitalized. Net

assets in foreign subsidiaries and associated companies amounted at

year-end 2008 to SEK 66.0 billion (61.1). Of this amount, SEK 4.3

billion (3.8) was currency-hedged through loans in foreign currencies.

Out of the loans used as hedging instruments SEK 3.3 billion are due

in 2010 and the remaining SEK 1.0 billion in 2011. The need to under-

take currency hedging relating to investments in associated com-

panies and other companies is assessed on a case-by-case basis.

Credit risks

Volvo’s credit provision is steered by Group-wide policies and cus-

tomer-classifi cation rules. The credit portfolio should contain a sound

distribution among different customer categories and industries. The

credit risks are managed through active credit monitoring, follow-up

routines and, where applicable, product reclamation. Moreover, regu-

lar monitoring ensures that the necessary provisions are made for

incurred losses on doubtful receivables. In the tables below, ageing

analyses are presented of accounts receivables overdues and cus-

tomer fi nance receivables overdue in relation to the reserves made. It

is not unusual that a receivable is settled a couple of days after due

date, which affects the extent of the age interval 1–30 days.

The credit portfolio of Volvo’s customer-fi nancing operations

amounted at December 31, 2008, to approximately SEK 98 billion

(79) in the Volvo group and SEK 112 billion (91) in the segment Cus-

tomer Finance. The difference is pertaining to the reclassifi cation in

the segment reporting of Customer Finance as operational leases are

reclassifi ed to fi nancial leases in accordance with IAS 14 Segment

Reporting. See note 1 for details regarding the accounting treatment.

The credit risk of this portfolio is distributed over a large number of

retail customers and dealers. Collaterals are provided in the form of

the fi nanced products. Credit provision aims for a balance between

risk exposure and expected yield. The Volvo Group’s fi nancial assets

are largely managed by Volvo Treasury and invested in the money and

capital markets. All investments must meet the requirements of low

credit risk and high liquidity. According to Volvo’s credit policy, coun-

terparties for investments and derivative transactions should have a

rating of A or better from one of the well-established credit rating

institutions.

The use of derivatives involves a counterparty risk, in that a poten-

tial gain will not be realized if the counterparty fails to fulfi ll its part of

the contract. To reduce the exposure, master netting agreements are

signed, wherever possible, with the counterparty in question. Counter-

party risk exposure for futures contracts is limited through daily or

monthly cash transfers corresponding to the value change of open

contracts. The estimated gross exposure to counterparty risk relating

to futures, interest-rate swaps and interest-rate forward contracts,

options and commodities contracts amounted at December 31, 2008,

to 3,798 (3,424), 2,763 (2,527), 229 (48) and 38 (113).

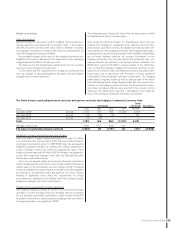

Credit portfolio – Accounts receivable and

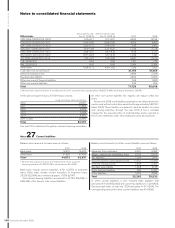

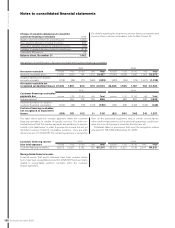

Customer fi nancing receivables

Accounts receivable 2007 2008

Accounts receivable gross 31,427 32,272

Valuation allowance for doubtful

accounts receivable (923) (1,749)

Accounts receivable net 30,504 30,523

For details regarding the accounts receivable and the valuation for

doubtful accounts receivable, refer to note 20.

Customer fi nancing receivables 2007 2008

Customer fi nancing receivables gross 80,210 99,931

Valuation allowance for doubtful customer

fi nancing receivables (1,363) (1,442)

Customer fi nancing receivables net 78,847 98,489