Rogers 2007 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2007 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

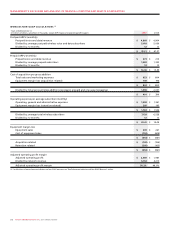

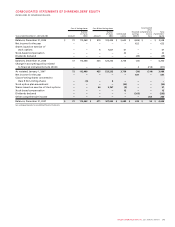

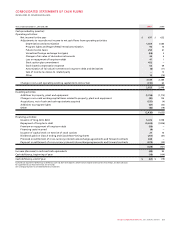

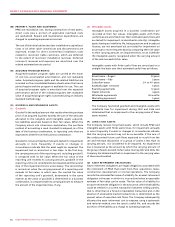

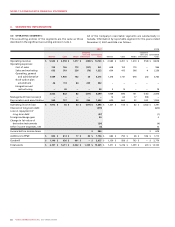

84 ROGERS COMMUNICATIONS INC. 2007 ANNUAL REPORT

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(H) FINANCIAL INSTRUMENTS:

(i) Adoption of new financial instruments standards:

In 2005, The Canadian Institute of Chartered Accountants

(“CICA”) issued Handbook Section 3855, Financial Instruments –

Recognition and Measurement, Handbook Section 1530,

Comprehensive Income, Handbook Section 3251, Equity, and

Handbook Section 3865, Hedges. The new standards were

adopted commencing January 1, 2007, and were generally

required to be adopted retrospectively without restatement.

A new statement entitled “Consolidated Statement of

Comprehensive Income” was added to the Company’s

consolidated financial statements and includes net income

as well as other comprehensive income. Accumulated other

comprehensive income forms part of shareholders’ equity.

The impact of the adoption of these standards on opening

accumulated other comprehensive income and on opening

deficit at January 1, 2007, was as follows:

(A) Under these standards, all of the Company’s financial assets

are classified as available-for-sale or loans and receivables.

Available-for-sale investments are carried at fair value on the

balance sheet, with changes in fair value recorded in other

comprehensive income, until such time as the investments

are disposed of or an other-than-temporary impairment has

occurred, in which case the impairment is recorded in income.

Loans and receivables and all financial liabilities are carried

at amortized cost using the effective interest method. Upon

adoption, the Company determined that none of its financial

assets are classified as held-for-trading or held-to-maturity and

none of its financial liabilities are classified as held-for-trading.

The impact of the classification provisions of the new standards

on January 1, 2007, was an adjustment of $213 million to bring

the carrying value of available-for-sale investments to fair

value, with a corresponding increase in opening accumulated

other comprehensive income of $211 million, net of income

taxes of $2 million.

For the year ended December 31, 2007, the impact of the

classification provisions of the new standards was an increase

in the carrying value of available-for-sale investments

of $140 million, with a corresponding increase in other

comprehensive income. In addition, realized gains of $2 million

were reclassified out of accumulated other comprehensive

income and recognized in the consolidated statements of

income upon disposal of an investment.

(B) All derivatives, including embedded derivatives that must be

separately accounted for, are measured at fair value, with

changes in fair value recorded in the consolidated statements

of income unless they are effective cash flow hedging

instruments. The changes in fair value of cash flow hedging

derivatives are recorded in other comprehensive income,

to the extent effective, until the variability of cash flows

relating to the hedged asset or liability is recognized in the

consolidated statements of income. Any hedge ineffectiveness

is recognized in the consolidated statements of income

immediately. The impact of remeasuring hedging derivatives

on the consolidated financial statements on January 1, 2007,

was an increase in derivative instruments of $561 million. This

also resulted in a decrease in opening accumulated other

comprehensive income of $425 million, net of income taxes of

$136 million, and an increase in opening deficit of $8 million,

net of income taxes of $2 million, representing the ineffective

portion of hedging relationships.

In 2007, $1 million related to hedge ineffectiveness was

recognized as an increase to net income.

The foreign exchange loss reclassified from comprehensive

income for the year ended December 31, 2007, exactly offset

the foreign exchange gains recognized in the consolidated

statements of income related to the carrying value of

U.S. dollar denominated debt.

(C) As a result of the application of these standards, the Company

separated the early repayment option on one of the Company’s

debt instruments and recorded the fair value of $19 million

related to this embedded derivative on the consolidated

balance sheet on January 1, 2007, with a corresponding

decrease in opening deficit of $13 million, net of income taxes

of $6 million. The fair value of this embedded derivative at

December 31, 2007, was $13 million and the decrease in the fair

value of $6 million was recorded in the consolidated statements

of income for the year ended December 31, 2007.

Impact

upon Income tax Net

adoption impact impact

Available-for-sale investments (A) $ 213 $ (2) $ 211

Derivative instruments (B) (561) 136 (425)

Opening accumulated other comprehensive income $ (348) $ 134 $ (214)

Ineffective portion of hedging derivatives (B) $ (10) $ 2 $ (8)

Early repayment option (C) 19 (6) 13

Deferred transitional gain (E) 54 (17) 37

Transaction costs (F) (59) 20 (39)

Opening deficit $ 4 $ (1) $ 3