Rogers 2007 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2007 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124

|

|

116 ROGERS COMMUNICATIONS INC. 2007 ANNUAL REPORT

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(K) CONSOLIDATED STATEMENTS OF CASH FLOWS:

(i) Canadian GAAP permits the disclosure of a subtotal of the

amount of funds provided by operations before changes in

non-cash operating working capital items in the consolidated

statements of cash flows. United States GAAP does not permit

this subtotal to be included.

(ii) Canadian GAAP permits bank advances to be included in the

determination of cash and cash equivalents in the consolidated

statements of cash flows. United States GAAP requires that

bank advances be reported as financing cash flows. As a result,

under United States GAAP, the total decrease in cash and

cash equivalents in 2007 of $42 million would be nil and cash

used in financing activities would be increased by $42 million.

The total increase in cash and cash equivalents in 2006 in the

amount of $85 million would be nil and cash used in financing

activities would be decreased by $85 million.

In addition to the amounts disclosed above, under United States

GAAP, the net amount recognized in the consolidated balance

sheets related to the Company’s supplemental unfunded pension

benefits for certain executives was $24 million (2006 – $19 million).

The total accumulated other comprehensive loss associated with

the supplemental plan amounts to $8 million (2006 – $5 million), on

a pre-tax basis.

(N) RECENT UNITED STATES ACCOUNTING PRONOUNCEMENTS:

In September 2006, the FASB issued FASB Statement No. 157,

Fair Value Measurements. This new standard defines fair value,

establishes a framework for measuring fair value under generally

accepted accounting principles and expands disclosures about

fair value measurements. This new standard is effective for the

Company beginning January 1, 2008. The Company is currently

assessing the impact of this new standard.

(L) OTHER DISCLOSURES:

United States GAAP requires the Company to disclose accrued

liabilities, which is not required under Canadian GAAP. Accrued

liabilities included in accounts payable and accrued liabilities as

at December 31, 2007, were $1,659 million (2006 – $1,287 million). At

December 31, 2007, accrued liabilities in respect of PP&E totalled

$133 million (2006 – $153 million), accrued interest payable totalled

$87 million (2006 – $109 million), accrued liabilities related to payroll

totalled $179 million (2006 – $234 million), and CRTC commitments

totalled $2 million (2006 – $9 million).

(M) PENSIONS:

The following summarizes the additional disclosures required and

different pension-related amounts recognized or disclosed in the

Company’s accounts under United States GAAP:

In February 2007, the FASB issued FASB Statement No. 159, The

Fair Value Option for Financial Assets and Financial Liabilities.

This statement permits entities the option to measure financial

instruments at fair value, thereby achieving an offsetting effect

for accounting purposes for certain changes in fair value of

certain related assets and liabilities without having to apply hedge

accounting. This statement is effective for the Company beginning

January 1, 2008. The Company is currently assessing the impact of

this new standard on its consolidated financial statements.

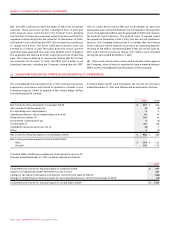

2007 2006

Current service cost (employer portion) $ 29 $ 24

Interest cost 34 32

Expected return on plan assets (37) (33)

Amortization:

Transitional asset (10) (10)

Realized gains included in income 1 1

Net actuarial loss 7 10

Net periodic pension cost under Canadian and United States GAAP $ 24 $ 24

Accrued benefit asset under Canadian GAAP $ 39 $ 34

Accumulated other comprehensive loss under United States GAAP, on a pre-tax basis (115) (97)

Net amount recognized in the consolidated balance sheets under United States GAAP $ (76) $ (63)