Rogers 2007 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2007 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

ROGERS COMMUNICATIONS INC. 2007 ANNUAL REPORT 47

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The credit ratings accorded by the

rating agencies are not recom-

mendations to purchase, hold or

sell the rated securities inasmuch

as such ratings do not comment

as to market price or suitability

for a particular investor. There is

no assurance that any rating will

remain in effect for any given

period of time or that any rating

will not be revised or withdrawn

entirely by a rating agency in the

future if in its judgment circum-

stances so warrant.

Deficiency of Pension Plan Assets Over Accrued Obligations

As disclosed in Note 18 to our 2007 Audited Consolidated Financial

Statements, our pension plans had a deficiency of plan assets over

accrued obligations of $83 million and $67 million at December 31,

2007, and December 31, 2006, respectively. In addition to our regular

contributions, we are making certain minimum monthly special

payments to eliminate this deficiency. In 2007, the special payment

totalled approximately $2 million. Our total estimated annual fund-

ing requirements, which include both our regular contributions

and these special payments, are expected to increase from $28 mil-

lion in 2007 to $35 million in 2008, subject to annual adjustments

thereafter, due to various market factors and the assumption that

staffing levels at the Company will remain relatively stable year-

over-year. We are contributing to the plans on this basis. As further

discussed in the section of this MD&A entitled “Critical Accounting

Estimates”, changes in factors such as the discount rate, the rate of

compensation increase and the expected return on plan assets can

impact the accrued benefit obligation, pension expense and the

deficiency of plan assets over accrued obligations in the future.

INTEREST RATE AND FOREIGN EXCHANGE MANAGEMENT

Economic Hedge Analysis

For the purposes of our discussion on the hedged portion of long-

term debt, we have used non-GAAP measures in that we include

all cross-currency interest rate exchange agreements (whether or

not they qualify as hedges for accounting purposes) since all such

agreements are used for risk management purposes only and

are designated hedges of specific debt instruments for economic

purposes. As a result, the Canadian dollar equivalent of U.S. dollar-

denominated long-term debt reflects the contracted foreign

exchange rate for all of our cross-currency interest rate exchange

agreements regardless of qualifications for accounting purposes as

a hedge.

During 2007, we redeemed an aggregate US$705 million of our U.S.

dollar-denominated debt and terminated an aggregate notional

principal amount of US$275 million of our cross-currency interest

rate exchange agreements.

As a result of the foregoing debt redemptions and swap termina-

tions, on December 31, 2007, 100% of our U.S. dollar-denominated

debt was hedged on an economic basis and on an accounting basis,

as noted below.

20072006

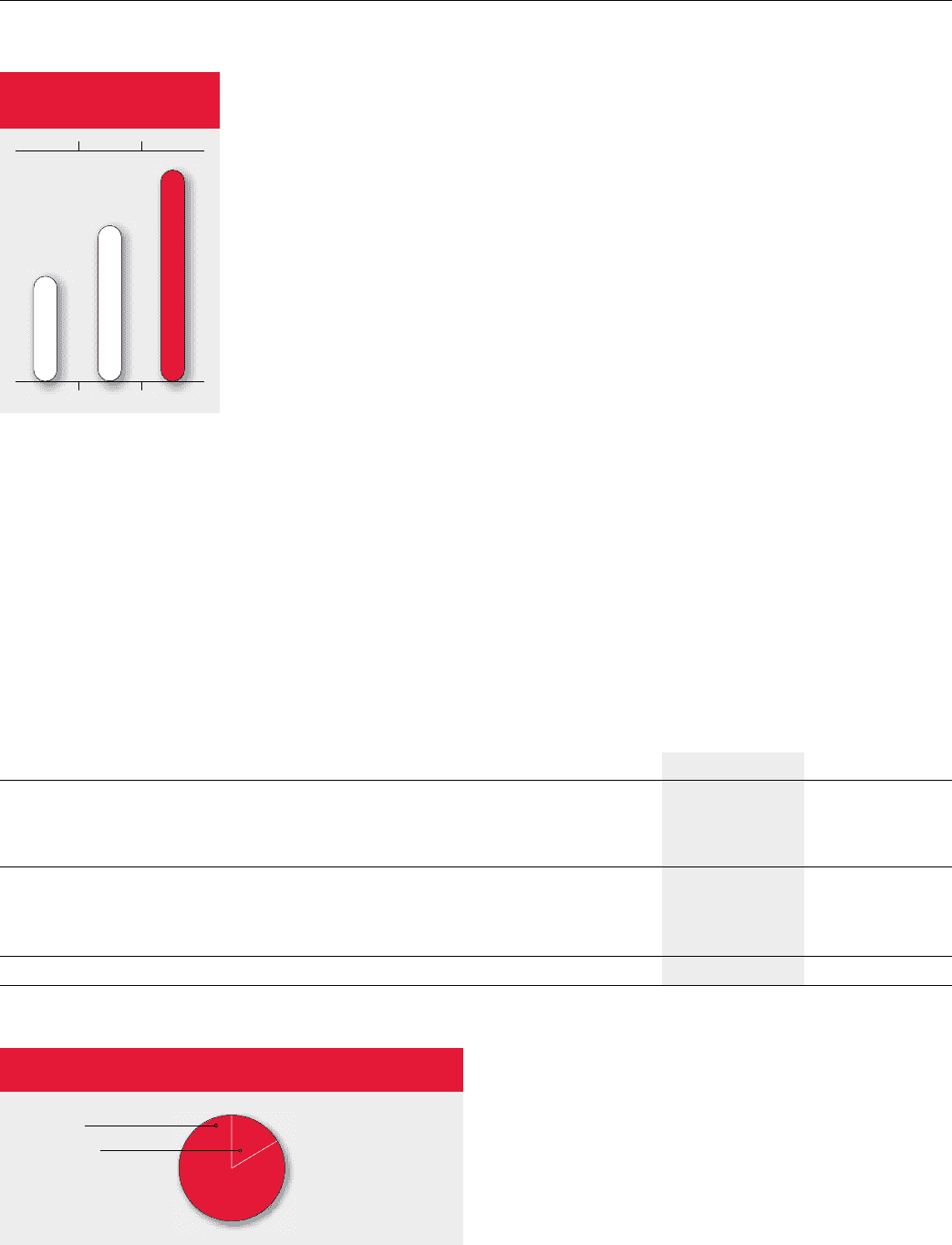

6.4x4.7x3.2x

RATIO OF ADJUSTED

OPERATING PROFIT

TO INTEREST

200

6

2007

2005

Consolidated Hedged Position

(In millions of dollars, except percentages) December 31, 2007 December 31, 2006

U.S. dollar-denominated long-term debt US $ 4,190 US $ 4,895

Hedged with cross-currency interest rate exchange agreements US $ 4,190 US $ 4,475

Hedged exchange rate 1.3313 1.3229

Percent hedged 100.0% (1) 91.4%

Amount of long-term debt (2) at fixed rates:

Total long-term debt Cdn $ 7,454 Cdn $ 7,658

Total long-term debt at fixed rates Cdn $ 6,214 Cdn $ 6,851

Percent of long-term debt fixed 83.4% 89.5%

Weighted average interest rate on long-term debt 7.53% 7.98%

(1) Pursuant to the requirements for hedge accounting under Canadian Institute of Chartered Accountants (“CICA”) Handbook Section 3865, Hedges, on December 31, 2007, RCI accounted for 100%

(2006 – 93.6%) of its cross-currency interest rate exchange agreements as hedges against designated U.S. dollar-denominated debt.

(2) Long-term debt includes the effect of the cross-currency interest rate exchange agreements.

FIXED VERSUS FLOATING DEBT COMPOSITION

(%)

Fixed 83.4%

Floating 16.6%