Pitney Bowes 2007 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2007 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

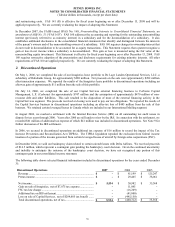

PITNEY BOWES INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Tabular dollars in thousands, except per share data)

48

Interest Rate Swaps

Derivatives designated as fair value hedges include interest rate swaps related to fixed rate debt. Changes in the fair value of

both the derivative and hedged item attributable to the risk being hedged are recognized in income. In December 2003, we

entered into an interest rate swap for an aggregate notional amount of $350 million. The interest rate swap effectively

converted the fixed rate of 4.75% on $350 million of our notes, due 2018, into variable interest rates. The variable rates

payable by us in connection with the swap agreement are based on six month LIBOR less a spread of 22.8 basis points. At

December 31, 2007, the fair value of the derivative represented an asset of $6.8 million. Long-term debt was increased by

$6.8 million at December 31, 2007.

Net Investment Hedges

A portion of our inter-company loans denominated in a foreign currency is designated as a hedge of net investment. The

revaluation of these loans is reflected as a deferred translation gain or loss and thereby offsets a portion of the translation

adjustment of the applicable foreign subsidiaries’ net assets. At December 31, 2007, we had two inter-company loans with

an outstanding value of $126.4 million associated with these net investment hedges. Net deferred translation gains of $37.4

million for 2007 were included in accumulated other comprehensive income in stockholders’ equity on the Consolidated

Balance Sheet.

Reclassification

Certain prior year amounts in the consolidated financial statements have been reclassified to conform to the current year

presentation.

New Accounting Pronouncements

In May 2005, the Financial Accounting Standards Board (FASB) issued SFAS No. 154, Accounting Changes and Error

Corrections (“FAS 154”), which replaces APB Opinion No. 20, Accounting Changes and SFAS No. 3, Reporting Accounting

Changes in Interim Financial Statements-An Amendment of APB Opinion No. 28. FAS 154 requires retrospective application

to prior periods’ financial statements of a voluntary change in accounting principle unless it is not practicable. FAS 154 is

effective for accounting changes and corrections of errors made in fiscal years beginning after December 15, 2005. Our

adoption of FAS 154 did not have a material impact on our financial position, results of operations or cash flows.

In June 2005, the FASB issued FASB Staff Position (FSP) No. FAS 143-1, Accounting for Electronic Equipment Waste

Obligations, that provides guidance on how commercial users and producers of electronic equipment should recognize and

measure asset retirement obligations associated with the European Directive 2002/96/EC on Waste Electrical and Electronic

Equipment (the Directive). The adoption of this FSP did not have a material effect on our financial position, results of

operations or cash flows for those European Union (EU) countries that enacted the Directive into country-specific laws.

In June 2006, the FASB issued FASB Interpretation (FIN) No. 48, Accounting for Uncertainty in Income Taxes (“FIN 48”),

which supplements Statement of Financial Accounting Standard No. 109, Accounting for Income Taxes, by defining the

confidence level that a tax position must meet in order to be recognized in the financial statements. FIN 48 requires the tax

effect of a position to be recognized only if it is “more-likely-than-not” to be sustained based solely on its technical merits as

of the reporting date. If a tax position is not considered more-likely-than-not to be sustained based solely on its technical

merits, no benefits of the position are recognized. This is a different standard for recognition than was previously required.

The more-likely-than-not threshold must continue to be met in each reporting period to support continued recognition of a

benefit. At adoption, companies adjusted their financial statements to reflect only those tax positions that were more-likely-

than-not to be sustained as of the adoption date. Any necessary adjustment was recorded directly to opening retained earnings

in the period of adoption and reported as a change in accounting principle. We adopted the provisions of FIN 48 on January

1, 2007 which resulted in a decrease to opening retained earnings of $84.4 million, with a corresponding increase in our tax

liabilities.

In July 2006, the FASB issued FSP No. FAS 13-2, Accounting for a Change or Projected Change in the Timing of Cash

Flows Relating to Income Taxes Generated by a Leveraged Lease Transaction, that provided guidance on how a change or a

potential change in the timing of cash flows relating to income taxes generated by a leveraged lease transaction affected the

accounting by a lessor for the lease. We adopted the provisions of FSP No. FAS 13-2 on January 1, 2007. Our adoption of

this FSP did not have a material impact on our financial position, results of operations or cash flows.