Pitney Bowes 2007 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2007 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

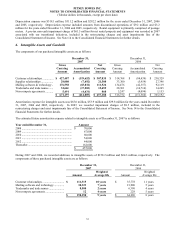

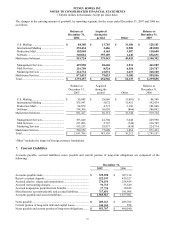

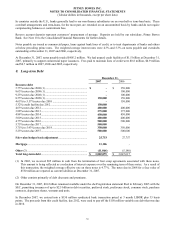

PITNEY BOWES INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Tabular dollars in thousands, except per share data)

46

Multiple Element Arrangements

Certain of our transactions are consummated at the same time. The most common form of these transactions involves the

sale or lease of equipment, a meter rental and/or an equipment maintenance agreement. In these cases, revenue is recognized

for each of the elements based on their relative fair values in accordance with SFAS 13, Emerging Issues Task Force (EITF)

No. 00-21, Accounting for Revenue Arrangements with Multiple Deliverables, and SAB 104. Fair values of any meter rental

or equipment maintenance agreement are determined by reference to the prices charged in standalone and renewal

transactions. Fair value of equipment is determined based upon the present value of the minimum lease payments.

Costs and Expenses

We have a centralized treasury system and do not allocate interest costs to our business segments. Accordingly, all interest

costs are included in interest expense on the Consolidated Statements of Income and are not allocated to cost of financing.

Deferred Marketing Costs

We capitalize certain direct mail, telemarketing, internet, and retail marketing costs, associated with the acquisition of new

customers in accordance with SOP No. 93-7, Reporting on Advertising Costs. These costs are amortized over the expected

revenue stream ranging from 5 to 9 years. We review individual marketing programs for impairment on a periodic basis or as

circumstances warrant.

Other assets on our Consolidated Balance Sheets at December 31, 2007 and 2006 include $121 million and $117 million,

respectively, of deferred marketing costs. The Consolidated Statements of Income include the related amortization expense

of $39 million, $44 million and $46 million for the years ended December 31, 2007, 2006 and 2005, respectively.

Restructuring Charges

We apply the provisions of SFAS No. 146, Accounting for Costs Associated with Exit or Disposal Activities, to account for

one-time benefit arrangements and exit or disposal activities. SFAS No. 146 requires that a liability for costs associated with

an exit or disposal activity be recognized when the liability is incurred. We account for ongoing benefit arrangements under

SFAS No. 112, Employers’ Accounting for Postemployment Benefits, which requires that a liability be recognized when the

costs are probable and reasonably estimable. See Note 14 to the Consolidated Financial Statements.

Income Taxes

We recognize deferred tax assets and liabilities for the future tax consequences attributable to differences between the

financial statements carrying amounts of existing assets and liabilities and their respective tax bases. A valuation allowance

is provided when it is more likely than not that some portion or all of a deferred tax asset will not be realized. The ultimate

realization of deferred tax assets depends on the generation of future taxable income during the period in which related

temporary differences become deductible. We consider the scheduled reversal of deferred tax liabilities, projected future

taxable income and tax planning strategies in this assessment. Deferred tax assets and liabilities are measured using the

enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be

recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the

period that includes the enactment date of such change.

Earnings per Share

Basic earnings per share is based on the weighted average number of common shares outstanding during the year, whereas

diluted earnings per share also gives effect to all dilutive potential common shares that were outstanding during the period.

Dilutive potential common shares include preference stock, preferred stock, stock option and purchase plan shares.

Stock-based Compensation

Effective January 1, 2006, we adopted the provisions of SFAS No. 123(R), Share-Based Payment (“FAS 123R”). We

previously applied Accounting Principles Board (APB) Opinion No. 25, Accounting for Stock Issued to Employees, and

related Interpretations and provided the required pro forma disclosures of SFAS No. 123, Accounting for Stock-Based

Compensation. We elected to adopt the modified retrospective application method provided by FAS 123(R) and accordingly,

financial statement amounts for the periods presented herein reflect results as if the fair value method of expensing had been

applied from the original effective date of FAS 123.

Stock-based compensation represents the cost related to stock-based awards granted to employees. We measure stock-based

compensation cost at grant date, based on the estimated fair value of the award, and recognize the cost as expense on a

straight-line basis (net of estimated forfeitures) over the employee requisite service period. We estimate the fair value of

stock options using a Black-Scholes valuation model. The expense is recorded in costs; selling, general and administrative

expense; and research and development expense in the Consolidated Statements of Income based on the employees’

respective functions.