Cisco 2011 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2011 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

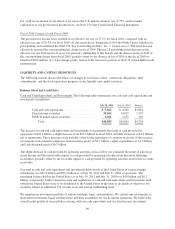

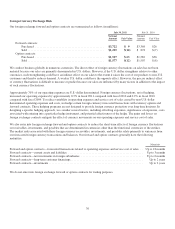

Equity Price Risk

The fair value of our equity investments in publicly traded companies is subject to market price volatility. We

may hold equity securities for strategic purposes or to diversify our overall investment portfolio. Our equity

portfolio consists of securities with characteristics that most closely match the Standard & Poor’s 500 Index or

NASDAQ Composite Index. These equity securities are held for purposes other than trading. To manage our

exposure to changes in the fair value of certain equity securities, we may enter into equity derivatives designated

as hedging instruments.

Publicly Traded Equity Securities

The following tables present the hypothetical fair values of publicly traded equity securities as a result of selected

potential decreases and increases in the price of each equity security in the portfolio, excluding hedged equity

securities, if any. Potential fluctuations in the price of each equity security in the portfolio of plus or minus 10%,

20%, and 30% were selected based on potential near-term changes in those security prices. The hypothetical fair

values as of July 30, 2011 and July 31, 2010 are as follows (in millions):

VALUATION OF

SECURITIES

GIVEN AN X%

DECREASE IN

EACH STOCK’S PRICE

FAIR VALUE

AS OF

JULY 30,

2011

VALUATION OF

SECURITIES

GIVEN AN X%

INCREASE IN

EACH STOCK’S PRICE

(30%) (20%) (10%) 10% 20% 30%

Publicly traded equity securities ......... $953 $1,089 $1,225 $1,361 $1,497 $1,633 $1,769

VALUATION OF

SECURITIES

GIVEN AN X%

DECREASE IN

EACH STOCK’S PRICE

FAIR VALUE

AS OF

JULY 31,

2010

VALUATION OF

SECURITIES

GIVEN AN X%

INCREASE IN

EACH STOCK’S PRICE

(30%) (20%) (10%) 10% 20% 30%

Publicly traded equity securities ......... $876 $1,001 $1,126 $1,251 $1,376 $1,501 $1,626

There were no significant impairment charges on our investments in publicly traded equity securities in fiscal

2011 while there was no such impairment charge in 2010. For fiscal 2009 impairment charges on our investments

in publicly traded equity securities were $39 million.

Investments in Privately Held Companies

We have also invested in privately held companies. These investments are recorded in other assets in our

Consolidated Balance Sheets and are accounted for using primarily either the cost or the equity method. As of

July 30, 2011, the total carrying amount of our investments in privately held companies was $796 million,

compared with $756 million at July 31, 2010. Some of the privately held companies in which we invested are in

the startup or development stages. These investments are inherently risky because the markets for the

technologies or products these companies are developing are typically in the early stages and may never

materialize. We could lose our entire investment in these companies. Our evaluation of investments in privately

held companies is based on the fundamentals of the businesses invested in , including, among other factors, the

nature of their technologies and potential for financial return. Our impairment charges on investments in

privately held companies were $10 million, $25 million, and $85 million for fiscal 2011, 2010, and 2009,

respectively.

75