Cisco 2011 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2011 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

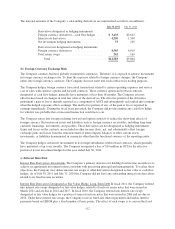

The notional amounts of the Company’s outstanding derivatives are summarized as follows (in millions):

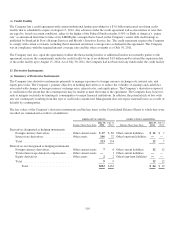

July 30, 2011 July 31, 2010

Derivatives designated as hedging instruments:

Foreign currency derivatives—cash flow hedges .... $ 3,433 $2,611

Interest rate derivatives ........................ 4,250 1,500

Net investment hedging instruments .............. 73 105

Derivatives not designated as hedging instruments:

Foreign currency derivatives .................... 4,565 4,619

Total return swaps ............................ 262 169

Total ................................... $12,583 $9,004

(b) Foreign Currency Exchange Risk

The Company conducts business globally in numerous currencies. Therefore, it is exposed to adverse movements

in foreign currency exchange rates. To limit the exposure related to foreign currency changes, the Company

enters into foreign currency contracts. The Company does not enter into such contracts for trading purposes.

The Company hedges foreign currency forecasted transactions related to certain operating expenses and service

cost of sales with currency options and forward contracts. These currency option and forward contracts,

designated as cash flow hedges, generally have maturities of less than 18 months. The Company assesses

effectiveness based on changes in total fair value of the derivatives. The effective portion of the derivative

instrument’s gain or loss is initially reported as a component of AOCI and subsequently reclassified into earnings

when the hedged exposure affects earnings. The ineffective portion, if any, of the gain or loss is reported in

earnings immediately. During the fiscal years presented, the Company did not discontinue any cash flow hedge

for which it was probable that a forecasted transaction would not occur.

The Company enters into foreign exchange forward and option contracts to reduce the short-term effects of

foreign currency fluctuations on assets and liabilities such as foreign currency receivables, including long-term

customer financings, investments, and payables. These derivatives are not designated as hedging instruments.

Gains and losses on the contracts are included in other income (loss), net, and substantially offset foreign

exchange gains and losses from the remeasurement of intercompany balances or other current assets,

investments, or liabilities denominated in currencies other than the functional currency of the reporting entity.

The Company hedges certain net investments in its foreign subsidiaries with forward contracts, which generally

have maturities of up to six months. The Company recognized a loss of $10 million in OCI for the effective

portion of its net investment hedges for the year ended July 30, 2011.

(c) Interest Rate Risk

Interest Rate Derivatives, Investments The Company’s primary objective for holding fixed income securities is to

achieve an appropriate investment return consistent with preserving principal and managing risk. To realize these

objectives, the Company may utilize interest rate swaps or other derivatives designated as fair value or cash flow

hedges. As of July 30, 2011 and July 31, 2010 the Company did not have any outstanding interest rate derivatives

related to its fixed income securities.

Interest Rate Derivatives Designated as Fair Value Hedge, Long-Term Debt In fiscal 2011, the Company entered

into interest rate swaps designated as fair value hedges related to fixed-rate senior notes that were issued in

March 2011 and are due in 2014 and 2017. In fiscal 2010, the Company entered into interest rate swaps

designated as fair value hedges for a portion of senior fixed-rate notes that were issued in 2006 and are due in

2016. Under these interest rate swaps, the Company receives fixed-rate interest payments and makes interest

payments based on LIBOR plus a fixed number of basis points. The effect of such swaps is to convert the fixed

112