HSBC 2005 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

95

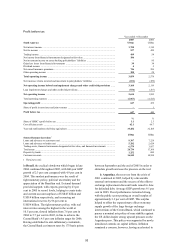

fee income increased by US$27 million, reflecting a

29 per cent increase in credit card fees and a 29 per

cent increase in current account fee income, driven

by increased transaction volumes in a recovering

economy.

The sale of HSBC’s Brazilian property and

casualty insurance business, HSBC Seguros de

Automoveis e Bens Limitada, to HDI Seguros S.A.,

led to the recognition of an US$89 million gain,

reported in other operating income.

Loan impairment charges and other credit risk

provisions increased to US$515 million, reflecting

strong growth in unsecured lending. Credit quality in

Brazil remained stable in the majority of product

lines, but there was a 5 per cent increase in impaired

loans as a proportion of assets in the consumer

finance business. The consumer finance sector

experienced increased credit availability, which led to

indebtedness exceeding customers’ repayment

capacity, increasing delinquencies. However,

tightening of credit approval policies and

improvements in the credit scoring model led to an

improvement in the charge as a proportion of assets

in the fourth quarter. Credit quality in Argentina

improved, reflecting generally better economic

conditions.

Operating expenses increased by 27 per cent. In

Brazil, the acquisition of Valeu Promotora de Vendas

and CrediMatone S.A. led to a significant increase in

average staff numbers, though by the end of 2005

staff numbers were 2 per cent lower than at

December 2004, following a restructuring of the

consumer finance business. The increased average

number of full-time employees, the impact of a

mandatory national salary increase and the transfer of

the Brazilian insurance business from the ‘Other’

business segment contributed to a 25 per cent

increase in Brazilian staff costs. Other expenses grew

to support business expansion and the development

of direct sales channels, while transactional taxes

increased by 21 per cent, driven by higher operating

income. In Argentina, costs were 3 per cent up on

2004 as increased performance-related remuneration

and union agreed salary increases led to higher staff

costs.

Commercial Banking reported pre-tax profits of

US$185 million, 2 per cent higher than 2004. In

Brazil, pre-tax profits increased by 12 per cent as

asset growth drove higher revenues, which were

mitigated by increased loan impairment charges and

higher costs. In Argentina, pre-tax profits declined by

31 per cent, as significant loan recoveries were not

repeated.

Net interest income increased by 49 per cent,

driven by asset growth. In Brazil, a growing economy

and a 30 per cent rise in customer numbers led to

increases in both assets and liabilities. Overdraft

balances grew by 41 per cent as both the number and

the average size of facilities grew, contributing

US$40 million of additional income. Overdraft

spreads increased by 3 percentage points as a result

of increases in the rate charged to new borrowers.

The continuing success of Giro fácil, a revolving loan

and overdraft facility, resulted in a 13 per cent

increase in customer numbers which, together with an

increase in facility utilisation, resulted in a 77 per

cent increase in balances. Invoice financing balances

rose by 30 per cent, benefiting from both increased

marketing and higher sales to Losango clients,

approximately a third of whom now have a

commercial banking relationship with HSBC.

Deposit balances in Brazil increased by 21 per

cent, reflecting initiatives to incentivise staff to

prioritise sales of liability products. However,

competitive pressures contributed to a 5 percentage

points decrease in spreads on loans and advances to

customers, while deposit spreads were 13 basis points

lower. In Argentina, deposits from commercial

customers increased by 42 per cent, reflecting the

continuing economic recovery, while loans and

overdrafts more than doubled and current account

balances increased by 38 per cent. HSBC increased

its market share in both loans and deposits.

Net fee income was 14 per cent lower than 2004,

driven by IFRSs changes to accounting for effective

interest rates, which reduced fee income by 40 per

cent. Excluding this effect, net fee income increased,

due to higher fees from payments and cash

management, current accounts, and lending in Brazil.

Current account fees increased by 26 per cent,

reflecting tariff increases, improved collection

procedures and higher transaction volumes, while

lending fees benefited from higher business volumes.

In Argentina, the launch of a commercial banking

call centre in the first half of 2005 enhanced the

customer service proposition. This, together with the

recruitment of additional relationship managers,

supported a 14 per cent increase in customer numbers

and, as a result, current account fee income increased

by 21 per cent. Improvements in the Argentinian

economic climate contributed to increased trade

flows which, together with the establishment of a

dedicated trade service sales team, led to a 22 per

cent increase in trade services income.

Loan impairment charges and other credit risk

provisions were US$55 million, following a small net

release in 2004. In Brazil, asset growth contributed to

a US$47 million increase in charges. Impaired loans