HSBC 2005 Annual Report Download - page 395

Download and view the complete annual report

Please find page 395 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

390 -

391

391 -

392

392 -

393

393 -

394

394 -

395

395 -

396

396 -

397

397 -

398

398 -

399

399 -

400

400 -

401

401 -

402

402 -

403

403 -

404

404 -

405

405 -

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

393

(commonly referred to as the 'shortcut' method) for certain of these hedging relationships. As a result, no

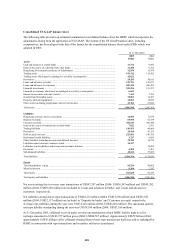

retrospective or prospective assessment of effectiveness is required and no hedge ineffectiveness is recognised.

If any one of the criteria for utilising the shortcut method was not met, the hedging relationship was either

accounted for under the 'long-haul' method whereby effectiveness is assessed and ineffectiveness on effective

hedges is recorded in the income statement, or the hedge relationship was determined to be ineffective for

accounting purposes and the derivative was marked to market with gains and losses recorded directly in net

income.

During 2005, new designations of hedges have generally been designated using the long-haul method of

accounting under SFAS 133 and certain relationships have been re-designated using this method. As a result,

there were no longer any cash flow hedges using the shortcut method of accounting at 31 December 2005, and

HSBC’s US operating subsidiaries have significantly reduced the number of fair value hedges using the shortcut

method of accounting at this date.

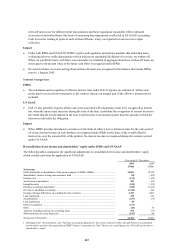

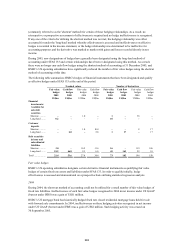

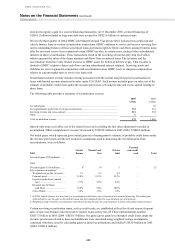

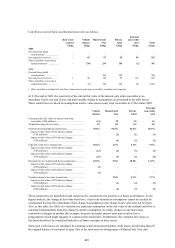

The following table summarises HSBC's hedges of financial instruments that have been designated and qualify

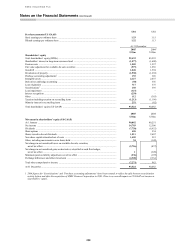

as effective hedges under SFAS 133 at the end of the period.

Nominal values Number of derivatives

Fair value

hedges

Cash flow

hedges

Fair value

hedges

Cash flow

hedges

Fair value

hedges

Cash flow

hedges

Fair value

hedges

Cash flow

hedges

2005 2005 2004 2004 2005 2005 2004 2004

US$bn US$bn US$bn US$bn US$bn US$bn US$bn US$bn

Financial

investments:

Available for

sale debt

securities

Shortcut .......... ––1.0 –1–38 –

Long-haul ....... 0.2 – ––10–––

Customer

deposits

Shortcut .......... ––1.0 10.4 ––817

Long-haul ....... –6.8 –5.8 117 –17

Debt securities

in issue and

subordinated

liabilities

Shortcut .......... 3.0 – 16.5 11.6 16 – 119 106

Long-haul ....... 18.2 46.8 9.3 6.6 45 165 29 10

Total ................... 21.4 53.6 27.8 34.4 73 182 194 150

Fair value hedges

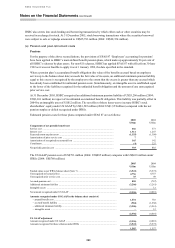

HSBC’s US operating subsidiaries designate certain derivative financial instruments as qualifying fair value

hedges of certain fixed rate assets and liabilities under SFAS 133. In order to qualify initially, hedge

effectiveness is assessed and demonstrated on a prospective basis utilising statistical regression analysis.

2004

During 2004, the short-cut method of accounting could not be utilised for a small number of fair value hedges of

fixed rate liabilities. Ineffectiveness of such fair value hedges recognised in 2004 in net income under US GAAP

(but not under IFRS) was a gain of US$1 million.

HSBC’s US mortgage bank has historically hedged fixed rate closed residential mortgage loans held for sale

with forward sale commitments. In 2004, ineffectiveness on these hedging activities recognised in net income

under US GAAP (but not under IFRS) was a gain of US$2 million. Such hedging activity was ceased on

30 September 2005.