HSBC 2005 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

HSBC HOLDINGS PLC

Financial Review (continued)

144

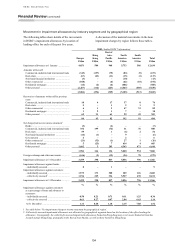

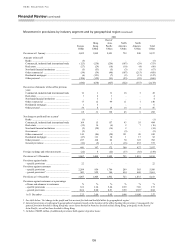

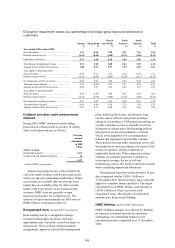

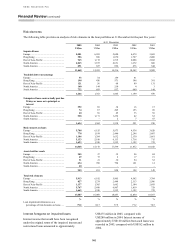

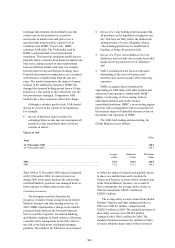

HSBC Holdings’ maximum exposure to credit

risk at 31 December 2005, excluding collateral or

other credit enhancements, was as follows:

2005

Carrying

value

Off-balance

sheet exposure

Maximum

exposure

US$m US$m US$m

Derivatives ......................................................................................................... 968 – 968

Loans and advances to HSBC undertakings ....................................................... 14,092 3,663 17,755

Financial investments – debt securities of HSBC undertakings .......................... 3,256 – 3,256

Guarantees .......................................................................................................... – 36,877 36,877

18,316 40,540 58,856

No collateral or other credit enhancements were

held by HSBC Holdings in respect of its transactions

with subsidiary undertakings, other than cash

deposited in respect of interest rate contract margins.

HSBC Holdings’ financial assets are held with

subsidiaries of HSBC, primarily those domiciled in

Europe and North America.

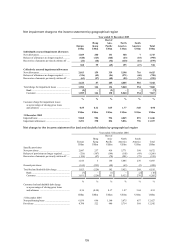

Areas of special interest

Group advances to personal customers

The loan impairment charge in 2005 remained

dominated by the charge relating to the personal

sector, which represented 92 per cent of the Group

total after taking account of losses from HSBC’s

other credit related activities. Within this total, losses

on residential mortgages remained modest.

At 31 December 2005, HSBC’s lending to the

personal sector amounted to US$420 billion, or

56 per cent of total gross loans and advances,

compared with US$388 billion (57 per cent) at

31 December 2004. Acquisitions in 2005 accounted

for 1 per cent of the overall increase on the previous

year. The main characteristics of this portfolio and

the economic influences affecting it are outlined

below.

Secured residential mortgages, including the

Hong Kong GHOS, accounted for US$239 billion,

or 57 per cent of total lending to the personal sector,

compared with US$228 billion, or 59 per cent, at

31 December 2004. The US and the UK were the

main areas of growth in 2005, though increased

lending to European customers was masked by the

effect of the strengthening US dollar on currency

translation. In percentage terms, growth in the Rest

of Asia-Pacific was also strong, and mortgage

lending increased by over 30 per cent in each of the

Middle East, India, Taiwan, South Korea, mainland

China and Singapore.

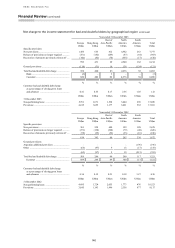

Growth in the unsecured element of the

portfolio, consisting of credit and charge card

advances, personal loans, vehicle finance facilities

and other varieties of instalment finance, was more

subdued than in the prior year. Following a review of

the UK personal unsecured lending book,

US$1 billion of gross lending to personal customers

was written off, and related collectively assessed loss

allowances extinguished. This reflected those

amounts for which it was deemed there was no

realistic possibility of recovery, and was the main

cause of more subdued growth. At 31 December

2005, the combined portfolios totalled

US$182 billion, or 43 per cent, of total lending to the

personal sector, compared with US$160 billion, or

41 per cent, at 31 December 2004. The acquisition of

the credit card portfolios of Metris added

US$5 billion to unsecured lending in 2005.

Growth in these portfolios reflected resilient

consumer spending in most of the main economies in

which HSBC operates. In the UK, demand for

additional consumer credit moderated, and

marketing and competitive pricing initiatives were

the main drivers of growth. Again, growth in Europe

was masked by the strengthening US dollar.

Geographically, total lending to personal

customers was dominated by the diverse and mature

portfolios in North America (US$218 billion), the

UK (US$107 billion) and Hong Kong

(US$38 billion). Collectively, these books accounted

for 87 per cent of total lending to the personal sector

(31 December 2004: 87 per cent).

Account management within HSBC’s personal

lending portfolios is generally supported by

sophisticated statistical techniques, which are

enhanced by the availability of credit reference data

in key local markets. The utilisation of an

increasingly analytical approach to the management

of these portfolios remains an ongoing objective of

the Group.

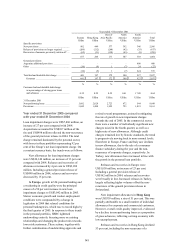

In the US, excluding the acquisition of Metris,

growth was largely in the mortgage services and

branch-based consumer lending businesses.

Promotions in the dealer network, and strong growth

in the consumer direct loan programme, also