HSBC 2005 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

HSBC HOLDINGS PLC

Financial Review (continued)

146

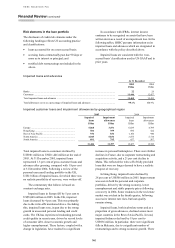

Risk elements in the loan portfolio

The disclosure of credit risk elements under the

following headings reflects US accounting practice

and classifications:

• loans accounted for on a non-accrual basis;

• accruing loans contractually past due 90 days or

more as to interest or principal; and

• troubled debt restructurings not included in the

above.

In accordance with IFRSs, interest income

continues to be recognised on assets that have been

written down as a result of an impairment loss. In the

following tables, HSBC presents information on its

impaired loans and advances which are designated in

accordance with the policy described above.

Impaired loans are consistent with the ‘non-

accrual basis’ classification used in US GAAP and in

prior years.

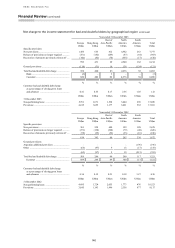

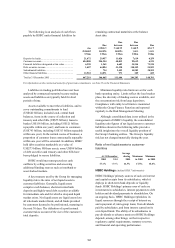

Impaired loans and advances

At 31 December

2005

US$m

2004

US$m

Banks .............................................................................................................................................. 22 26

Customers ....................................................................................................................................... 11,446 12,427

Total impaired loans and advances ................................................................................................. 11,468 12,453

Total allowances cover as a percentage of impaired loans and advances ........................................ 99.1% 100.9%

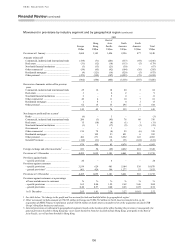

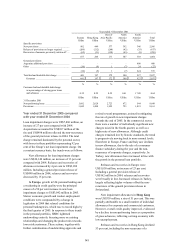

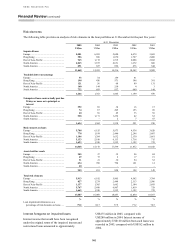

Impaired customer loans and impairment allowances by geographical region

2005 2004

Impaired

loans

Impairment

allowances

Impaired

loans

Impairment

allowances

US$m US$m US$m US$m

Europe ......................................................................... 5,068 3,491 6,039 4,799

Hong Kong .................................................................. 506 399 696 522

Rest of Asia-Pacific ..................................................... 936 836 1,160 940

North America ............................................................. 4,045 5,836 3,875 5,714

South America ............................................................. 891 795 657 567

11,446 11,357 12,427 12,542

Total impaired loans to customers declined by

US$981 million to US$11,446 million at the end of

2005. At 31 December 2005, impaired loans

represented 1.5 per cent of gross customer loans and

advances after grossing, compared with 1.8 per cent

at 31 December 2004. Following a review of the

personal unsecured lending portfolio in the UK,

US$1 billion of impaired loans, for which there was

no realistic possibility of recovery, were written-off.

The commentary that follows is based on

constant exchange rates.

Impaired loans in Europe fell by 5 per cent to

US$5,068 million in 2005. In the UK, impaired

loans decreased by 4 per cent. This was primarily

due to the write-offs mentioned above. Excluding

this, impaired loans rose, in part due to the strong

growth in unsecured personal lending and credit

cards. The UK has experienced weakening personal

credit quality in recent years, driven by record levels

of consumer debt, slower economic growth and

higher unemployment. These factors, coupled with a

change in legislation, have resulted in a significant

increase in personal bankruptcies. There were further

declines in France, due to corporate restructuring and

acquisition activity, and a 21 per cent decline in

Malta. This reflected the write-off of fully provided

loans that were no longer deemed to have a realistic

prospect of recovery.

In Hong Kong, impaired loans declined by

28 per cent to US$506 million in 2005. Improvement

was seen in both the personal and corporate

portfolios, driven by the strong economy, lower

unemployment and stable property prices following

a recovery in 2004. Some weakness in the real estate

market was evident in the fourth quarter, following

successive interest rate rises, but loan quality

remains strong.

Impaired loans, both in absolute terms and as a

proportion of gross advances, declined across most

major countries in the Rest of Asia-Pacific. In total,

impaired balances declined by 19 per cent to

US$936 million. In particular, there were significant

falls in Malaysia, due to a significant number of

restructurings and to strong economic growth. There