HSBC 2005 Annual Report Download - page 338

Download and view the complete annual report

Please find page 338 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

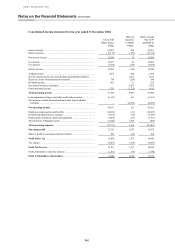

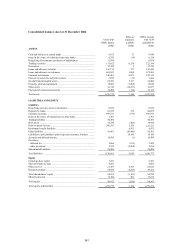

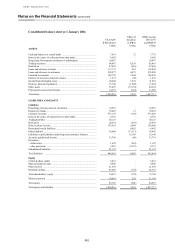

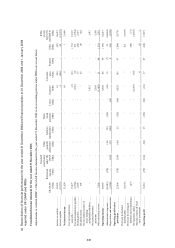

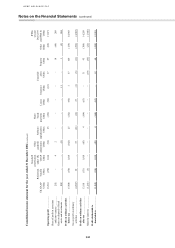

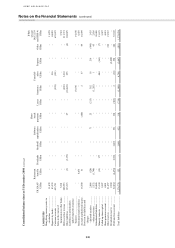

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

336

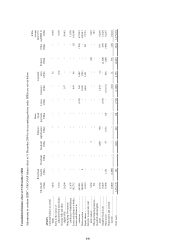

IAS 19 ‘Employee Benefits’ (‘IAS 19’)

IAS 19 requires pension fund assets to be assessed at fair value and liabilities on the basis of current actuarial

assumptions using the projected unit credit method. As permitted by an amendment to IAS 19, HSBC elected to

recognise all actuarial gains and losses directly in retained earnings.

The change in accounting resulted in the recognition of a pension obligation of US$6,475 million at

31 December 2004 (1 January 2004: US$4,982 million) which, after adjustment for prospective tax relief and the

portion of the deficit attributable to minority interests, reduced total shareholders’ equity by US$4,470 million

(1 January 2004: US$3,529 million). The effect of the transition to IAS 19 on 2004’s operating profit was to

increase the charge for pension costs by US$170 million. US$242 million of this related to an increase in

pension liability from termination benefits attributable to members of the HSBC Bank (UK) Pension Scheme

arising from major staff reduction programme in the second half of the year. Under UK GAAP, the impact of the

staff reduction programme on the pension scheme was spread over the remaining average life of the scheme.

IAS 10 ‘Events after the Balance Sheet Date’ (‘IAS 10’)

Under IAS 10, equity dividends declared after the balance sheet date are not included as a liability at the balance

sheet date. Accordingly, HSBC reversed the liability for proposed dividends at each balance sheet date. This had

the effect of increasing shareholders’ equity at 31 December 2004 and 1 January 2004 by US$2,996 million and

US$2,627 million respectively.

IAS 17 ‘Leases’ (‘IAS 17’)

IAS 17 requires that unearned income on finance leases be taken to income at a rate calculated to give a constant

rate of return on the net investment in the lease, with no account taken in calculating the net investment of the

tax effects of the lease. In general, this leads to a deferral of finance income compared with the pattern of

recognition under UK GAAP, where income is recognised at a constant rate of return on the net cash investment

in the lease including the effect of tax.

Under UK GAAP, assets leased out under operating leases are depreciated over their useful lives so that, for

each asset, rentals less depreciation are recognised at a constant periodic rate of return on the net cash invested in

that asset. Under IFRSs, operating leased assets are depreciated to ensure that in each period the depreciation

charge is at least equal to that which would have arisen on a straight-line basis.

The effect of both finance and operating leases on shareholders’ equity at 31 December 2004 was a decrease of

US$503 million (1 January 2004: decrease of US$402 million). The effect of the transition to IAS 17 was to

decrease operating profit by US$90 million for the year ended 31 December 2004.

Under UK GAAP, leasehold land was separately identified within the valuation of land and buildings. For

HSBC, this principally arose in Hong Kong, where all land is held by way of leases. IFRSs require leasehold

land to be treated as held under an operating lease unless title is expected to pass to the lessee at the end of the

lease. No revaluation is permitted in respect of such owner-occupied operating lease assets. Leasehold land

valued at US$1,345 million at 1 January 2004 was reclassified as operating lease assets on the date of transition

to IFRSs. This resulted in the reversal of previously recognised revaluation surpluses amounting to

US$622 million, and the inclusion of prepaid rentals of US$723 million in ‘Other assets’ at 1 January 2004.

IFRS 2 ‘Share-based Payment’ (‘IFRS 2’)

IFRS 2 requires companies to adopt a fair-value-based method of accounting for share-based compensation plans

which takes into account vesting conditions related to market performance, for example total shareholder return.

Under this method, compensation cost is measured at the date of grant based on the assessed value of the award

and is recognised over the service period, which is usually the vesting period.

In respect of other vesting conditions, an estimate of the number of options that will lapse before they vest is

made at grant date and adjustments to this estimate are made over the service period. Accordingly, the expense

recognised reflects, over time, the actual number of lapsed options for non-market performance-related

conditions.

There is no exemption under IFRS 2 for Save-As-You-Earn schemes, as existed under UK GAAP.