HSBC 2005 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

HSBC HOLDINGS PLC

Financial Review (continued)

164

Annuities are contracts providing income from

capital investment paid in a stream of regular

payments for either a fixed period or during the

annuitant’s lifetime. Deferred annuities are those

whose payments to the annuitant begin at a

designated future date as opposed to immediate

annuities where payments begin at once. The

principal risks in respect of annuity business relate to

mortality and market risk in relation to the need to

match investments against the anticipated cash flow

profile of the policies. HSBC has a number of

annuity books, some of which have been in run-off

for several years. The majority of the annuity book is

composed of contracts with a duration of no longer

than five years. Investments are managed to match

the anticipated cash flow profile, and the mortality

risk is regularly monitored. HSBC has annuity

business in the US, Mexico, Cayman Islands and

Argentina.

The major component of the ‘Term assurance

and other long-term contracts’ category is term

assurance and critical illness policies written in the

UK. The principal risks are in respect of mortality

and morbidity, and are mitigated through a

combination of underwriting practices, premium

adjustment in light of changes in experience and

reinsurance.

For linked insurance business, market risk is

usually borne by policyholders. The principal risk

retained by HSBC relates to expenses, although

mortality, disability and morbidity risks are also

associated with this product and are managed

through the application of the techniques set out

above for non-linked lines of business.

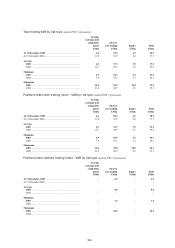

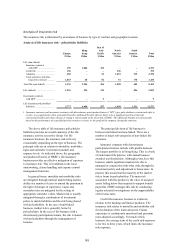

Analysis of non-life insurance risk – net written insurance premiums1

Europe

Hong-

Kong

Rest of

Asia-

Pacific

North

America

South

America Tota l

US$m US$m US$m US$m US$m US$m

Accident and health ................... 33 67 3 8 1 112

Motor ......................................... 192201147259529

Fire and other damage ............... 251 34 3 8 58 354

Liability ..................................... 229 17 2 90 15 353

Credit (non-life) ......................... 225 – –202 –427

Marine, aviation

and transport .......................... –16 4 –2242

Other non-life insurance

contracts ................................ 10 29 – 17 12 68

Total net written insurance

premiums ............................... 940 183 23 372 367 1,885

1Net written insurance premiums represent gross written premiums less gross written premiums ceded to reinsurers.

Non-life insurance contracts include liability

and property insurance. However, only a small

proportion of HSBC’s non-life insurance portfolio is

liability insurance which is in general underwritten

as part of a product business proposal. The key risks

associated with non-life business are underwriting

risk and claims experience risk. Underwriting risk is

the risk that HSBC does not charge premiums

appropriate for the cover provided and claims

experience risk is the risk that portfolio experience is

worse than expected. HSBC manages these risks

through prudent pricing (for example, imposing

restrictions and deductibles in the policy terms and

conditions), product design, risk selection, claims

handling, investment strategy and reinsurance

policy. All non-life insurance contracts are annually

renewable and the underwriters have the right to

refuse renewal or to change the terms and conditions

of the contract at renewal.

HSBC underwrites non-life insurance business

in Ireland, the UK, Hong Kong, Argentina, the US,

Mexico and Singapore.

Accident and health insurance business is

underwritten in all major markets with the largest

portfolio being Hong Kong. Potential accumulations

of personal accident risks are mitigated by the

purchase of catastrophe reinsurance.

Motor insurance business covers vehicle

damage and liability for personal injury. It includes a

large portfolio underwritten in Brazil for

US$105 million, which was disposed of during

2005. Other significant portfolios are written in the