HSBC 2005 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

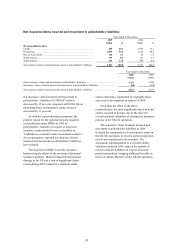

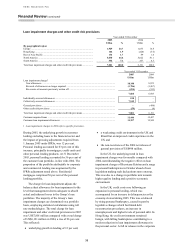

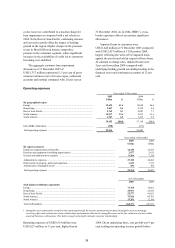

31

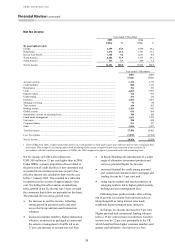

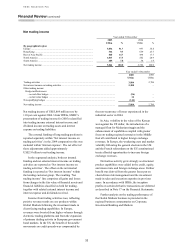

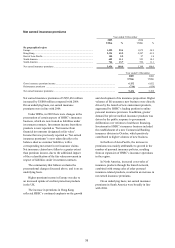

increased by 9 per cent, reflecting increased

customer numbers, the launch of a new packaged

product in the UK and the introduction of a Small

Business Tariff in Commercial Banking. Buoyant

equity markets benefited custody fees, which grew

as a result of both increased asset values and strong

new business volumes. Private Banking fee income

was 12 per cent higher than in 2004 following

increases in client assets under management and

transaction volumes.

In Hong Kong, net fee income was in line with

2004. Unit trust fees decreased by 42 per cent as

Personal Financial Services customers switched to

traditional deposit savings and shorter-term

investment products. The launch of 173 new open-

ended funds established HSBC as the leading

investment service provider in Hong Kong. This,

together with the successful attraction of client assets

in Private Banking, contributed to a rise in income

from funds under management. Credit card fee

income increased by 18 per cent, reflecting growth

in cardholder spending as HSBC strengthened its

position as the largest credit card issuer in Hong

Kong. In Commercial Banking, net fees increased as

trade services, insurance and lending income rose.

However, lower Structured Finance revenues led to

reduced Corporate, Investment Banking and Markets

fees.

Net fee income in the Rest of Asia-Pacific rose

by 28 per cent from higher card transaction volumes

and increased account service fees in response to the

expansion of the Personal Financial Services

business in the region. Rising equity markets,

buoyant regional economies and an increase in

personal wealth combined with the launch of new

products to increase sales of investment products to

personal customers. Client assets in Private Banking

also grew. Global Transaction Banking revenues

increased in line with transaction volumes following

investment in 2004 to expand capabilities. Custody

fees grew by 29 per cent as a result of improved

investor sentiment and rising local equity markets.

Trade services income rose by 13 per cent, reflecting

strong trade flows.

In North America, net fee income grew by

21 per cent. Card fee income grew as a result of

higher transactions, increased receivables and

improvements in the interchange rate, while US

mortgage lending fees benefited from lower

refinancing prepayments and the consequent release

of impairment provisions on mortgage servicing

rights. In Mexico, strong growth in the cards base

drove higher net fee income and increased

transaction volumes delivered higher ATM fees and

increased remittance income. Investment banking

fees increased in response to HSBC’s success in

attracting customers with an expanded range of

products.

Net fee income in South America increased by

23 per cent, principally due to higher card, lending

and current account servicing fees. Current account

fees benefited from increased customer numbers and

tariff increases, while lending fee growth was

principally related to higher lending volumes. Card

fees increased as a result of higher spending in both

Brazil and Argentina.