HSBC 2005 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

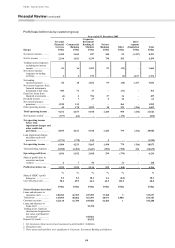

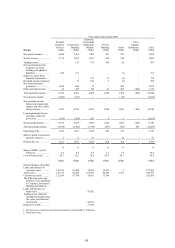

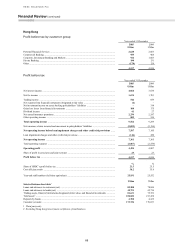

59

sophisticated risk-based pricing enabled customer

rates to be differentiated more acutely.

Net interest income from other unsecured

lending in the UK increased by 4 per cent. The

launch of differentiated pricing initiatives in April,

notably through preferential personal lending rate

offers to lower-risk customers, helped boost average

loan balances by 9 per cent, and increase HSBC’s

market share of gross advances from 10.7 to 11.7 per

cent. Focused sales and marketing, notably the

‘January sale’, also contributed to higher balances.

As indebtedness levels grew, growth was curtailed

through a tightening of underwriting criteria in the

more difficult credit environment. The introduction

of preferential pricing, and a mix change towards

higher value but lower-yielding loans, led to a

48 basis point narrowing of spreads.

Recruitment of new current account customers

was strong, and HSBC’s market share of new current

accounts increased to 14.7 per cent, largely through

brand-led awareness and marketing. The launch of

two new current account propositions, including

HSBC’s first value-driven packaged account in the

UK market, and improved cross-sales aided growth

of 6 per cent in overall customer accounts. This led

to an increase in net interest income from UK

current accounts of 5 per cent to US$1.0 billion,

broadly in line with the 6 per cent increase in

average balances.

Sales of new UK savings accounts increased

markedly, and average balances rose by 15 per cent,

driven by a greater front-line focus, competitive

pricing and the launch of new products, including

‘Regular Saver’ and ‘Online Saver’. Included in this

was growth of over US$1.2 billion in First Direct’s

‘e-savings’ product, launched in September 2004.

Net interest income, however, fell by 5 per cent,

largely due to the non-recurrence of the benefit to

spreads from base rate rises in 2004, and a slight

reduction in margin. The latter arose from

competitive pricing initiatives partly designed to

improve brand awareness and widen product

consideration.

In Turkey, innovative marketing initiatives and

advertising campaigns, with an emphasis on

attracting new customers, contributed to strong

growth in net interest income, which more than

doubled compared with 2004. Average card balances

increased by 66 per cent to US$0.9 billion, and

average mortgage balances more than doubled to

US$0.6 billion. Higher card usage by existing

customers, higher average mortgage advances and a

7 per cent increase in overall customer numbers

contributed to the growth.

In France, net interest income was broadly in

line with 2004. Marketing campaigns in the run-up

to the rebranding exercise contributed to a 54 per

cent increase in mortgage sales in a buoyant market,

and a resulting 18 per cent increase in average

balances. Cross-sales of current and special

regulated savings accounts were strong, and average

deposit balances grew by 4 per cent to

US$14.9 billion. The benefit of this balance sheet

expansion was largely offset by lower spreads, as

competitive pricing reduced yields on lending

products, and the maturing of older, higher-yielding

investments reduced the funding benefit from

deposits.

Excluding net interest income, net operating

income before loan impairment charges grew by

16 per cent to US$3,386 million, of which

12 percentage points was in the UK and largely

attributable to increased fees associated with the

increase in personal lending, mortgage and credit

card volumes described above. Increased card

utilisation also led to higher cash advance fees and

currency conversion income. An improved

investment fund offering, following the

depolarisation of the previously tied sales force, was

reflected in a 5 per cent increase in related

commissions. In Turkey, fee income benefited from

increased lending activity. In France, privatisations

boosted brokerage income, and new product

launches and marketing aided growth in insurance

and investment sales.

Under IFRSs, changes in presentation from

1 January 2005, notably for certain contracts

previously accounted for as insurance, and with the

designation of insurance-related assets at fair value,

caused large movements within certain individual

income lines. These had negligible impact on income

overall. There was also a US$32 million gain from

the fair value measurement of options linked to

French home-savings products.

Loan impairment charges of US$1,711 million

were 73 per cent higher than 2004, the majority of

which occurred in the UK. In large part, this

reflected the strong growth in higher margin credit

card and other unsecured lending in recent years.

Weakening economic conditions and sharply rising

personal bankruptcies, following the change in

legislation in 2004, were also significant

contributors.

Loan impairment charges as a percentage of

period end net customer advances rose from 0.8 to

1.4 per cent.

HSBC responded to the weaker UK credit

environment by further refining its credit eligibility