HSBC 2005 Annual Report Download - page 155

Download and view the complete annual report

Please find page 155 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

153

technique that estimates the potential losses that

could occur on risk positions as a result of

movements in market rates and prices over a

specified time horizon and to a given level of

confidence (for HSBC, 99 per cent). HSBC

calculates VAR daily. The VAR model used by

HSBC is predominantly based on historical

simulation. The historical simulation model derives

plausible future scenarios from historical market rate

time series, taking account of inter-relationships

between different markets and rates, for example,

between interest rates and foreign exchange rates.

Potential movements in market prices are calculated

with reference to market data from the last two

years. The model incorporates the impact of option

features in the underlying exposures. HSBC has

changed the assumed holding period from a 10-day

period to a 1-day period as this reflects the way the

risk positions are managed. Comparative VAR

numbers have been restated to reflect this change.

Although a valuable guide to risk, VAR should

always be viewed in the context of its limitations.

For example:

• the use of historical data as a proxy for

estimating future events may not encompass all

potential events, particularly those which are

extreme in nature;

• the use of a 1-day holding period assumes that

all positions can be liquidated or hedged in one

day. This may not fully reflect the market risk

arising at times of severe illiquidity, when a

1-day holding period may be insufficient to

liquidate or hedge all positions fully;

• the use of a 99 per cent confidence level, by

definition, does not take into account losses that

might occur beyond this level of confidence;

and

• VAR is calculated on the basis of exposures

outstanding at the close of business and

therefore does not necessarily reflect intra-day

exposures.

HSBC recognises these limitations by

augmenting its VAR limits with other position and

sensitivity limit structures. Additionally, HSBC

applies a wide range of stress testing, both on

individual portfolios and on the Group’s

consolidated positions. HSBC’s stress-testing regime

provides senior management with an assessment of

the financial impact of identified extreme events on

the market risk exposures of HSBC.

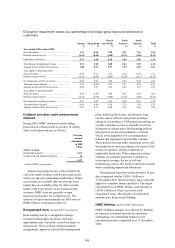

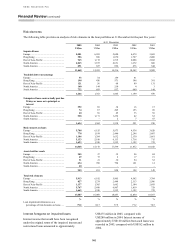

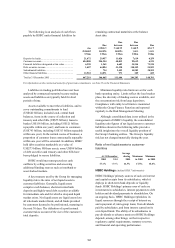

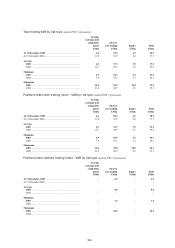

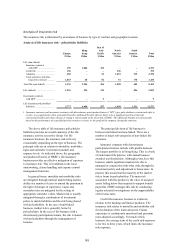

The VAR, both trading and non-trading, for

Global Markets was as follows:

Value at risk

US$m

Total

At 31 December 2005 ..................................................................................................................................................... 128.5

At 31 December 2004 ...................................................................................................................................................... 254.7

Average Minimum Maximum

US$m US$m US$m

2005 .................................................................................................................... 174.1 108.2 248.8

2004 .................................................................................................................... 172.5 101.2 304.2

Total VAR at 31 December 2005 reduced compared

with 31 December 2004. As interest rates rose

during 2005 in the major markets, the risk arising

in Global Markets’ positions was managed down to

limit exposure to further interest rate rises.

(Unaudited information)

The histogram overleaf illustrates the

frequency of daily revenue arising from all Global

Markets’ business and other trading activities. In

2005, HSBC implemented a change in the transfer

pricing of funds between the Personal Financial

Services and the Corporate, Investment Banking

and Markets segments in North America, following

a transfer of the management of all of the interest

rate risk of the held prime residential mortgage

portfolio. The numbers for 2004 have been restated

to reflect the impact of transfer pricing had it been

in place on a similar basis and to include the

Futures and Equities revenues which comprise part

of the Global Markets’ business. As a result of

these restatements, the average daily revenue in

2004 increased from US$18.3 million to

US$20.5 million.

The average daily revenue earned from Global

Markets’ business and other trading activities in

2005 was US$18.7 million, compared with

US$20.5 million in 2004. The standard deviation of

these daily revenues was US$10.4 million

compared with US$8.1 million for 2004. The

standard deviation measures the variation of daily

revenues about the mean value of those revenues.