HSBC 2005 Annual Report Download - page 380

Download and view the complete annual report

Please find page 380 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

370 -

371

371 -

372

372 -

373

373 -

374

374 -

375

375 -

376

376 -

377

377 -

378

378 -

379

379 -

380

380 -

381

381 -

382

382 -

383

383 -

384

384 -

385

385 -

386

386 -

387

387 -

388

388 -

389

389 -

390

390 -

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

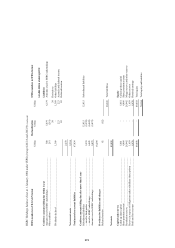

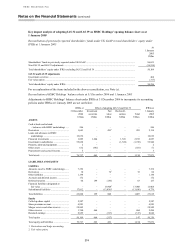

HSBC HOLDINGS PLC

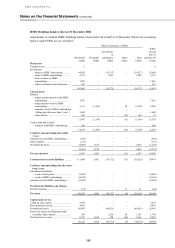

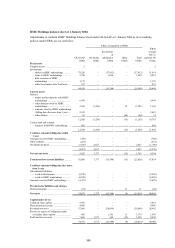

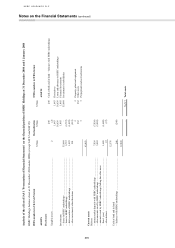

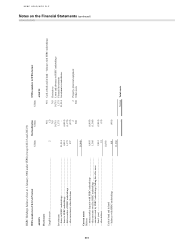

Notes on the Financial Statements (continued)

378

US GAAP

• US GAAP does not permit revaluations of property, including investment property, although it requires

recognition of asset impairment. Any realised surplus or deficit is, therefore, reflected in net income upon

disposal of the property. Depreciation is charged on all properties based on cost.

Impact

• Under IFRSs, the value of property held for own use reflects revaluation surpluses recorded prior to 1 January

2004. Consequently, the values of tangible fixed assets and shareholders' equity are lower under US GAAP than

under IFRSs.

• There is a correspondingly lower depreciation charge and higher net income under US GAAP, partially offset by

higher gains (or smaller losses) on the disposal of fixed assets.

• For investment properties, net income under US GAAP does not reflect the gain or loss recorded under IFRSs

for the period.

Derivatives and hedge accounting

IFRSs

• Derivatives are recognised initially, and are subsequently remeasured, at fair value. Fair values of exchange-

traded derivatives are obtained from quoted market prices. Fair values of OTC derivatives are obtained using

valuation techniques, including discounted cash flow models and option pricing models.

• In the normal course of business, the fair value of a derivative on initial recognition is considered to be the

transaction price (that is the fair value of the consideration given or received). However, in certain circumstances

the fair value of an instrument will be evidenced by comparison with other observable current market

transactions in the same instrument (without modification or repackaging) or will be based on a valuation

technique whose variables include only data from observable markets, including interest rate yield curves, option

volatilities and currency rates. When such evidence exists, HSBC recognises a trading gain or loss on inception

of the derivative. When unobservable market data have a significant impact on the valuation of derivatives, the

entire initial change in fair value indicated by the valuation model is not recognised immediately in the income

statement but is recognised over the life of the transaction on an appropriate basis or recognised in the income

statement when the inputs become observable, or when the transaction matures or is closed out.

• Derivatives may be embedded in other financial instruments; for example, a convertible bond has an embedded

conversion option. An embedded derivative is treated as a separate derivative when its economic characteristics

and risks are not clearly and closely related to those of the host contract, its terms are the same as those of a

stand-alone derivative, and the combined contract is not held for trading or designated at fair value. These

embedded derivatives are measured at fair value with changes in fair value recognised in the income statement.

• Derivatives are classified as assets when their fair value is positive, or as liabilities when their fair value is

negative. Derivative assets and liabilities arising from different transactions are only netted if the transactions are

with the same counterparty, a legal right of offset exists, and the cash flows are intended to be settled on a net

basis.

• The method of recognising the resulting fair value gains or losses depends on whether the derivative is held for

trading, or is designated as a hedging instrument and, if so, the nature of the risk being hedged. All gains and

losses from changes in the fair value of derivatives held for trading are recognised in the income statement.

When derivatives are designated as hedges, HSBC classifies them as either: (i) hedges of the change in fair value

of recognised assets or liabilities or firm commitments (‘fair value hedge’); (ii) hedges of the variability in highly

probable future cash flows attributable to a recognised asset or liability, or a forecast transaction (‘cash flow

hedge’); or (iii) hedges of net investments in a foreign operation (‘net investment hedge’). Hedge accounting is

applied to derivatives designated as hedging instruments in a fair value, cash flow or net investment hedge

provided certain criteria are met.

Hedge accounting

− It is HSBC’s policy to document, at the inception of a hedge, the relationship between the hedging

instruments and hedged items, as well as the risk management objective and strategy for undertaking the