HSBC 2005 Annual Report Download - page 299

Download and view the complete annual report

Please find page 299 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

299 -

300

300 -

301

301 -

302

302 -

303

303 -

304

304 -

305

305 -

306

306 -

307

307 -

308

308 -

309

309 -

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

297

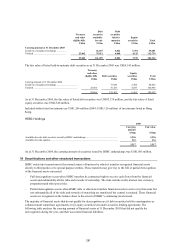

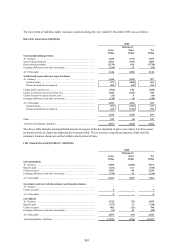

The cost of capital assigned to an individual cash-generating unit and used to discount its future cash flows can have

a significant effect on its valuation. The cost of capital percentage is generally derived from an appropriate Capital

Asset Pricing Model, which itself depends on inputs reflecting a number of financial and economic variables

including the risk-free rate in the country concerned and a premium to reflect the inherent risk of the business being

evaluated. These variables are established on the basis of management judgement.

Management judgement is required in estimating the future cash flows of the cash-generating units. These values are

sensitive to the cash flows projected for the periods for which detailed forecasts are available, and to assumptions

regarding the long-term sustainable pattern of cash flows thereafter. While the acceptable range within which

underlying assumptions can be applied is governed by the requirement for resulting forecasts to be compared with

actual performance and verifiable economic data in future years, the cash flow forecasts necessarily and appropriately

reflect management’s view of future business prospects.

The following CGUs include in their carrying value goodwill that is a significant proportion of total goodwill

reported by HSBC. These CGUs do not carry on their balance sheet any intangible assets with indefinite useful lives,

other than goodwill.

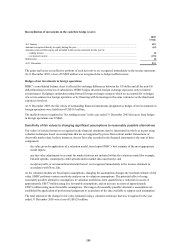

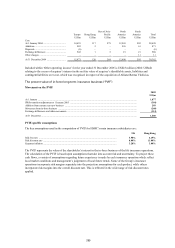

Cash Generating Unit

Goodwill at

1 July 2005

Discount

rate

Nominal

growth rate

beyond initial

cash flow

projections

US$m % %

Personal Financial Services – Europe ........................................................... 3,515 10.2 4.3

Commercial Banking – Europe .................................................................... 2,913 9.9 3.9

Private Banking – Europe ............................................................................. 3,701 10.0 3.2

Corporate, Investment Banking and Markets – Europe ................................ 3,694 10.1 4.0

Personal Financial Services – North America (other than Mexico) .............. 10,451 10.0 6.1

Total goodwill in the CGUs listed above ...................................................... 24,274

There was no evidence of impairment arising from this review. The only circumstances where a reasonably possible

change in key assumptions might have caused an impairment loss to be recognised was in respect of Private Banking

Europe where:

– a fall of 0.9% in the long-term growth rate beyond the initial cash flow projections; or

– an increase of 0.8% in the discount rate

would have caused an impairment loss to be recognised. Recognising this, the calculation of the value in use for

Private Banking – Europe, based on discounted projected cash flows, has been additionally benchmarked against

market transactions in private banking companies in Europe to ensure the carrying value is supportable.