HSBC 2005 Annual Report Download - page 165

Download and view the complete annual report

Please find page 165 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

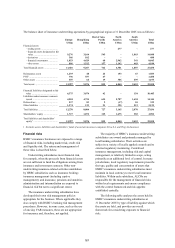

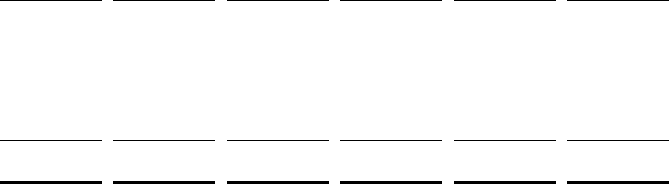

163

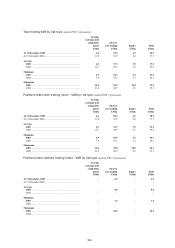

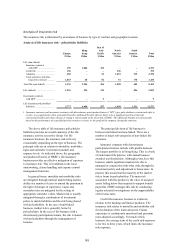

Analysis of insurance risk

The insurance risk is illustrated by an analysis of business by type of contract and geographic location.

Analysis of life insurance risk – policyholder liabilities

Europe

Hong

Kong

Rest of

Asia-

Pacific

North

America

South

America Tota l

US$m US$m US$m US$m US$m US$m

Life (non-linked)

Insurance contracts

with DPF1 .......................... 155 3,886 152 – – 4,193

Credit life .............................. 156 – –196 –352

Annuities ............................... 202 – 22 1,651 515 2,390

Term assurance and other

long-term contracts ........... 1,063 68 82 51 170 1,434

Total life (non-linked) ............... 1,576 3,954 256 1,898 685 8,369

Life (linked) .............................. 1,201 536 332 – 826 2,895

Investment contracts

with DPF1 .............................. ––9––9

Life insurance policyholders’

liabilities ................................ 2,777 4,490 597 1,898 1,511 11,273

1Insurance contracts and investment contracts with discretionary participation features (‘DPF’) give policyholders a contractual right to

receive, as a supplement to their guaranteed benefits, additional benefits that are likely to be a significant portion of the total

contractual benefits and whose amount or timing is contractually at the discretion of HSBC. The additional benefits are contractually

based on the performance of a specified pool of contracts or assets, or the profit of the company issuing the contracts.

The above table of life insurance policyholder

liabilities provides an overall summary of the life

insurance activity across the Group. For life

insurance business, the insurance risk will vary

considerably depending on the type of business. The

principal risks are in relation to mortality, morbidity,

lapse and surrender, investment (market) and

expense levels. As indicated above, the geographic

and product diversity of HSBC’s life insurance

business provides an effective mitigation of exposure

to insurance risk. This is in addition to the local

underwriting, claims handling and expense control

management functions.

In general terms, mortality and morbidity risks

are mitigated through medical underwriting and the

ability in a number of cases to amend the premium in

the light of changes in experience. Lapse and

surrender risks are mitigated by the setting of

appropriate surrender values. Market risk is usually

mitigated through a combination of investment

policy to match liabilities and the risk being shared

with policyholders. In the case of unit-linked

business, market risk is generally borne by

policyholders. In the case of life business with a

discretionary participation feature, the risk is shared

with policyholders through the management of

bonuses.

The principal division of life business is

between unit linked and non-linked. There are a

number of major sub-categories of non-linked life

assurance.

Insurance contracts with discretionary

participation features include with-profits business.

The largest portfolio is in Hong Kong. This is a book

of endowment life policies, with annual bonuses

awarded to policyholders. Although prima facie this

business entails significant market risk, this is

managed in conjunction with other risks through the

investment policy and adjustment to bonus rates. In

practice this means that the majority of the market

risk is borne by policyholders. The main risk

associated with this product is the value of assigned

assets falling below that required to support benefit

payments. HSBC manages this risk by conducting

regular actuarial investigations on the supportability

of the bonus rates.

Credit life insurance business is written in

relation to the banking and finance products. The

insurance risk relates to mortality and morbidity risk

for the duration of the loans advanced. Claims

experience is continuously monitored and premium

rates adjusted accordingly. For much of this

business, the average term of the credit risk exposure

is for two to three years, which limits the insurance

risk exposure.