HSBC 2005 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

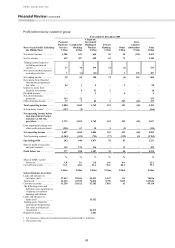

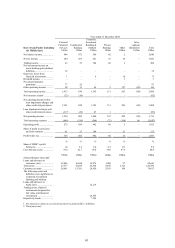

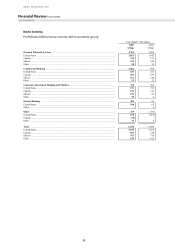

87

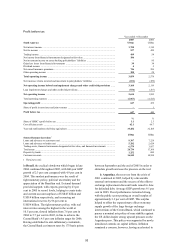

20 per cent market share and a near seven-fold

increase since December 2002. Strong sales of

insurance products resulted from increased cross-

selling through the branch network and combining

sales with other Personal Financial Services products

containing insurance components. Mutual fund

balances grew by 58 per cent, partly attributable to

the successful launch of new funds targeting

different market segments, along with strong cross-

sales among HSBC’s extensive customer base.

Trading income in 2005 was in line with 2004.

In the US mortgage banking business revenues

increased, largely as a result of more originations

and sales related income, which reflected improved

gains on each individual sale and a 41 per cent

increase in the volume of originated loans sold. In

addition, a higher percentage of ARM loans that

previously would have been held on balance sheet

were sold in 2005. This was partly offset by lower

gains on Decision One sales in the mortgage services

business.

The increase in other income was largely due to

the US. Losses from sales of properties repossessed

after customers default on their mortgage payments,

which are recorded as a reduction in other income,

were US$96 million lower than in 2004. This was

attributable to improvements in the process by which

fair market value is determined at the time of

repossession, and to a reduction in the number of

properties falling into repossession as credit quality

improved.

Loan impairment charges and other credit risk

provisions of US$5,086 million were marginally

lower than in 2004. In the US, charges were lower

notwithstanding the adverse effect of Hurricane

Katrina and higher bankruptcy filings following

changes in bankruptcy legislation. Partly offsetting

these impacts was the non-recurrence of

US$47 million charges from adopting Federal

Financial Institutions Examination Council charge-

off policies relating to retail and credit card balances

in 2004. Excluding these factors, the lower charge

reflected favourable credit conditions in the US.

Higher levels of secured lending, continued targeting

of higher credit quality customers and improvements

in underwriting contributed to the reduction. In

Mexico loan impairment charges rose in line with

higher lending volumes and the non-recurrence in

2005 of loan impairment provision releases in 2004,

while underlying credit quality remained stable. In

Canada, charges were in line with prior year, as

higher charges in the consumer lending business due

to loan growth were offset by provision releases in

the core bank business.

Operating expenses grew by 6 per cent to

US$7,382 million, largely in the US and Mexico. In

the US, costs increased by 3 per cent, as staff and

marketing costs rose in the consumer finance

business to support revenue growth. Acquisition

costs were incurred following the Metris purchase.

In the credit cards business, higher marketing spend

was incurred on the non-prime portfolios and

investment in new initiatives. Higher marketing

expenses were also incurred following changes in

contractual obligations associated with the General

Motors’ co-branded credit card portfolio in July

2004, but these were partly offset by improved

income through lower account origination fees.

In the US Bank, costs grew to support business

expansion and new branch openings. Brand

awareness programmes in the second and fourth

quarters increased marketing costs, and expenditure

was incurred on promoting the online savings

product. The benefit of these initiatives was reflected

in a significant increase in customer awareness of the

HSBC brand. Within the retail brokerage business,

cost increases reflected more stringent regulatory

requirements.

In Mexico, operating expenses grew by

21 per cent, driven by a combination of higher staff,

marketing and IT costs. Staff costs grew by

12 per cent, reflecting increases incurred to improve

customer service levels within the branch network

and bonus costs in line with increased sales.

Marketing costs grew to support the credit cards

business, evidenced by the 80 per cent increase in

the number of cards in circulation. IT costs rose as

new systems to meet Group standards, such as the

WHIRL credit card platform, were rolled out. In

Canada, operating expenses grew due to the opening

of new branches within the consumer finance

business, and expansion of the mortgage and credit

cards businesses.

Commercial Banking’s pre-tax profits

increased by 23 per cent to US$1,064 million,

primarily due to lending growth and improved

liability interest spreads.

Net interest income increased by 23 per cent to

US$1,449 million. In the US, deposit growth,

particularly among small businesses, contributed to a

20 per cent increase in net interest income. The

recruitment of additional sales and support staff and

expansion on both the East and West coasts led to a

15 per cent increase in deposits and a 16 per cent

increase in lending balances, with income from

commercial real estate lending increasing by 27 per

cent. HSBC achieved particularly strong growth in

the SME market and maintained its market leading