HSBC 2005 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

39

sector, however, contributed to a modest charge for

loan impairment as compared with a net release in

2004. In the Rest of Asia-Pacific, continuing releases

and recoveries partly offset the impact of lending

growth in the region. Higher charges in the personal

sector in Brazil followed intense competitive

pressure in the consumer segment, where significant

increases in the availability of credit led to customers

becoming over-indebted.

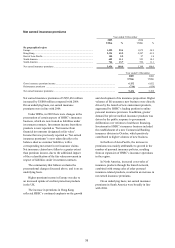

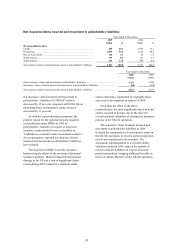

The aggregate customer loan impairment

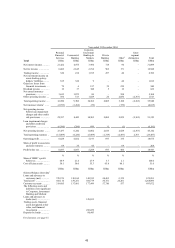

allowances at 31 December 2005 of

US$11,357 million represented 1.5 per cent of gross

customer advances (net of reverse repos, settlement

accounts and netting) compared with 2.0 per cent at

31 December 2004. As in 2004, HSBC’s cross-

border exposures did not necessitate significant

allowances.

Impaired loans to customers were

US$11,446 million at 31 December 2005 compared

with US$12,427 million at 31 December 2004,

largely reflecting the write-off of impaired loans

against the provisions held in respect of these loans.

At constant exchange rates, impaired loans were

3 per cent lower than 2004 compared with

underlying lending growth (excluding lending to the

financial sector and settlement accounts) of 12 per

cent.

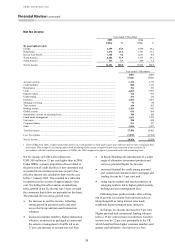

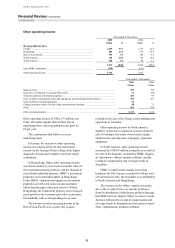

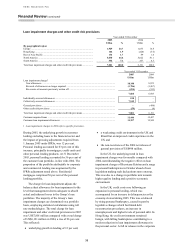

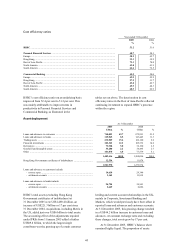

Operating expenses

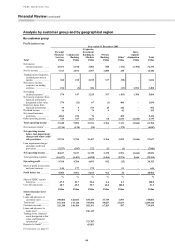

Year ended 31 December

2005 2004

US$m % US$m %

By geographical region

Europe ....................................................................................................... 12,639 41.4 12,028 44.4

Hong Kong ................................................................................................ 2,867 9.4 2,558 9.4

Rest of Asia-Pacific ................................................................................... 2,762 9.1 2,087 7.7

North America ........................................................................................... 10,217 33.6 9,032 33.3

South America ........................................................................................... 1,967 6.5 1,413 5.2

30,452 100.0 27,118 100.0

Intra-HSBC elimination ............................................................................. (938) (631)

Total operating expenses ........................................................................... 29,514 26,487

Year ended 31 December

2005 2004

US$m US$m

By expense category

Employee compensation and benefits .............................................................................................16,145 14,523

Premises and equipment (excluding depreciation) .......................................................................... 2,977 2,615

General and administrative expenses .............................................................................................. 8,206 7,124

Administrative expenses ................................................................................................................. 27,328 24,262

Depreciation of property, plant and equipment ............................................................................... 1,632 1,731

Amortisation of intangible assets1................................................................................................... 554 494

Total operating expenses ................................................................................................................ 29,514 26,487

At 31 December

2005 2004

Staff numbers (full-time equivalent)

Europe ............................................................................................................................................ 77,755 74,861

Hong Kong ..................................................................................................................................... 25,931 25,552

Rest of Asia-Pacific ........................................................................................................................ 55,577 41,031

North America ................................................................................................................................ 75,926 69,781

South America ................................................................................................................................ 33,282 32,108

Total staff numbers ......................................................................................................................... 268,471 243,333

1Intangible asset amortisation comprises the expensing through the income statement of purchased intangibles such as mortgage

servicing rights and customer/merchant relationships and amounts allocated to intangible assets on the fair valuation of assets within

acquired business combinations. This latter category principally includes customer relationships.

Operating expenses of US$29,514 million were

US$3,027 million, or 11 per cent, higher than in

2004. On an underlying basis, cost growth was 9 per

cent, trailing net operating income growth before