HSBC 2005 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

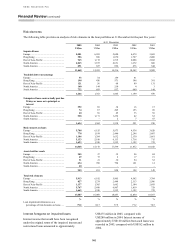

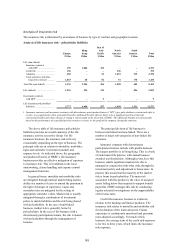

157

US$4.0 million), compared with US$3.7 million at

31 December 2004 (2004 average: US$3.9 million;

2004 minimum: US$2.8 million; 2004 maximum:

US$4.6 million).

Non-trading exposure also arises on non-

cumulative perpetual preferred securities issued.

These fixed-rate securities are eligible as tier 1

capital and are managed as capital instruments. Prior

to the adoption of IFRSs these securities were

classified as a non-equity element of minority

interests but they are now classified as debt

securities issued and therefore included in non-

trading market risk analysis. The combination of a

fixed interest rate and perpetual term generated a

VAR of US$65.0 million at 31 December 2005

(2005 average: US$70.3 million; 2005 minimum:

US$62.3 million; 2005 maximum: US$78.2 million),

compared with US$72.5 million at 31 December

2004 (2004 average: US$75.6 million; 2004

minimum: US$66.6 million; 2004 maximum:

US$86.3 million).

Market risk arises in HSBC’s insurance

businesses within their portfolios of investments and

policyholders’ liabilities. The principal market risks

are interest-rate risk and equity risk, which primarily

arise when guaranteed investment return policies

have been issued. The insurance businesses have a

dedicated head office market risk function which

oversees management of this risk.

A similar market risk also arises within HSBC’s

defined benefit pension schemes to the extent that

the obligations of the schemes are not fully matched

by assets with determinable cash flows. This risk

principally derives from the pension schemes

holding equities against their future pension

obligations. The risk is that market movements in

equity prices could result in assets which are

insufficient over time to cover the level of projected

liabilities. Management, together with the trustees

who act on behalf of the pension scheme

beneficiaries, assess the level of this risk using

reports prepared by independent external actuaries.

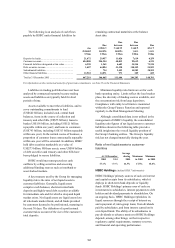

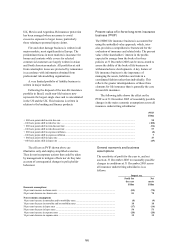

The present value of HSBC’s defined benefit

pension plans’ liabilities was US$27.7 billion at

31 December 2005, compared with US$26.5 billion

at 31 December 2004. Assets of the defined benefit

schemes at 31 December 2005 comprised: equity

investments 46 per cent (54 per cent at 31 December

2004); debt securities 33 per cent (29 per cent at

31 December 2004) and other (including property)

21 per cent (17 per cent at 31 December 2004). (See

Note 7 on the Financial Statements).

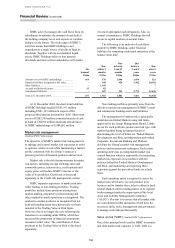

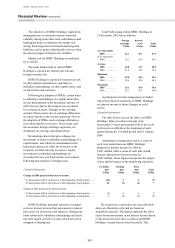

Net interest income

A principal part of HSBC’s management of market

risk in non-trading portfolios is to monitor the

sensitivity of projected net interest income under

varying interest rate scenarios (simulation

modelling). HSBC aims, through its management of

market risk in non-trading portfolios, to mitigate the

impact of prospective interest rate movements which

could reduce future net interest income, whilst

balancing the cost of such hedging activities on the

current net revenue stream.

For simulation modelling, businesses use a

combination of scenarios relevant to local businesses

and local markets as well as standard scenarios

required to be used across HSBC. The standard

scenarios are consolidated to illustrate the combined

pro forma impact on HSBC consolidated portfolio

valuations and net interest income.

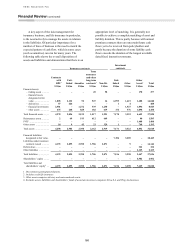

The table below sets out the impact on future net

interest income of a 25 basis points parallel fall or

rise in all yield curves worldwide at the beginning of

each quarter during the 12 month period from 1

January 2006. These scenarios differ from those

disclosed in the Annual Report and Accounts 2004

which assumed an immediate 100 basis points

parallel rise or fall in all yield curves on the first day

of the 12 month period. The revised scenarios,

although still simplified, are considered more

relevant.

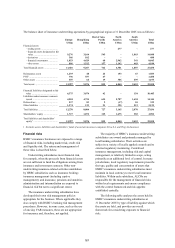

Assuming no management actions, such a series

of incremental parallel rises in all yield curves would

decrease planned net interest income for the year to

31 December 2006 by US$525 million, while such a

series of incremental parallel falls in all yield curves

would increase planned net interest income by

US$474 million. These figures incorporate the

impact of any option features in the underlying

exposures.

Instead of assuming that all interest rates move

together, HSBC groups its interest rate exposures

into currency blocs whose interest rates are

considered likely to move together. The sensitivity of

projected net interest income, on this basis, is

described as follows: