HSBC 2005 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

61

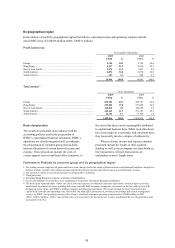

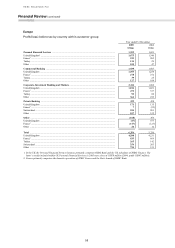

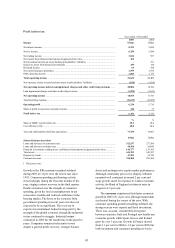

Commercial Banking customers with the most

experienced relationship managers, led to a 10 per

cent increase in medium term loan balances. Sight

deposit balances grew by 7 per cent, though deposit

spreads decreased as maturing funds were placed at

lower prevailing interest rates.

Net fee income increased by 2 per cent to

US$1,621 million, net of IFRSs changes to switch

some fees into the effective interest rate calculation,

which led to a 15 per cent reduction in fee income.

In the UK, higher new business volumes and lending

activity contributed to a US$77 million, or 27 per

cent, increase in loan and overdraft fee income.

Increased customer numbers, coupled with the

introduction of a new small business tariff in January

2005, led to a 13 per cent increase in current account

fee income. Card acquiring income increased by

8 per cent, despite a slowdown in consumer

spending driven by a 6 per cent increase in

transaction volumes, reflecting merchant acquisition.

A 21 per cent increase in card customer numbers

contributed to higher card issuing income.

HSBC benefited from the recruitment of

additional sales staff, development of profitable

relationships with brokers and the success of

dedicated corporate and commercial centres. Invoice

financing fee income increased by 9 per cent,

benefiting from an expanded client base, while a

tariff review contributed to a 16 per cent increase in

treasury income. The recruitment, in both 2004 and

2005, of commercial independent financial advisors,

together with the development of existing sales staff,

led to a 13 per cent increase in insurance and

investment income, with fee income from savings

and investment products increasing by a third.

Income in the vehicle and equipment leasing

businesses decreased by 13 per cent, following an

agreement to outsource the operational functions of

the UK vehicle finance contract hire business to Lex

Vehicle Leasing, which took effect from November

2005. Excluding the transfer, net fee income from

leasing increased by 5 per cent.

Loan impairment charges and other credit risk

provisions increased by 26 per cent to

US$378 million. In the UK, lending growth and

sizeable allowances against a small number of

accounts led to a US$162 million increase in

charges. Overall credit quality remained relatively

strong, although some deterioration was evident in

the market in the last three months of 2005 as

consumer spending declined. In France, new

individually assessed allowances were largely offset

by higher recoveries, while in Malta net releases

decreased as a large release against a single customer

in 2004 was not repeated.

Operating expenses decreased by 5 per cent and,

together with increased income, resulted in a

6 percentage point improvement in the cost

efficiency ratio. In the UK, the non-recurrence of

cost reduction expenditure in 2004, together with the

resulting fall in staff numbers and strong cost

control, contributed to a 10 per cent decrease in

operating expenses. Although overall staff numbers

declined, additional sales staff were hired to take

advantage of business opportunities in support of

revenue growth. These sales staff were supported by

press and other advertising campaigns aimed at

attracting customers switching banks and start-up

businesses to HSBC, together with a campaign

targeting SMEs which contributed to an increase in

marketing costs.

In France, staff recruitment, increased marketing

activity and re-branding led to an 8 per cent increase

in costs. Staff costs rose as HSBC France recruited

additional sales staff to support business expansion,

and success led to higher performance-related

remuneration. Campaigns targeting top tier

commercial customers and supporting product

launches led to an increase in marketing expenditure,

while rebranding and supporting activity to

emphasise the ‘HSBC’ name change also

contributed.

In an economy which grew by 5.5 per cent in

2005, increased business activity, the launch of SME

banking and the recruitment of additional sales and

support staff in Turkey contributed to a rise in

income and a 17 per cent increase in operating

expenses.

Corporate, Investment Banking and Markets

reported a pre-tax profit of US$2,114 million, an

increase of 27 per cent, compared with 2004.

Revenues from all major client-related trading

activities increased, particularly from the credit and

rates, equities and structured derivatives businesses

where HSBC has invested in upgrading its

capabilities. Operating expenses rose, reflecting the

first full-year cost of the expanded sales and

execution capabilities. However, cost growth slowed

in the second half of 2005 and in aggregate in

Europe, revenue growth comfortably surpassed

growth in costs. In Europe, 2005 marked the

transition from the investment phase of Corporate,

Investment Banking and Markets’ development

strategy to a focus on implementation.

Total operating income increased by 15 per cent

to US$5,510 million. Balance sheet management and

money market revenues declined by approximately

46 per cent reflecting a challenging interest rate