HSBC 2005 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

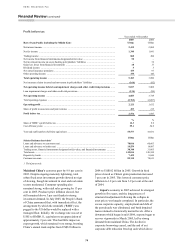

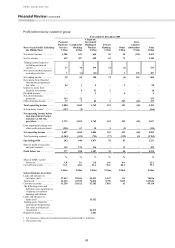

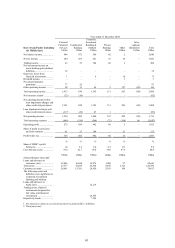

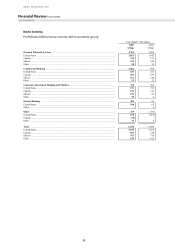

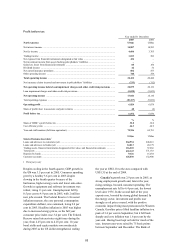

HSBC HOLDINGS PLC

Financial Review (continued)

84

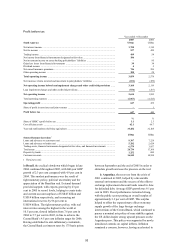

Canada has indicated that further increases may be

required.

Mexico’s GDP growth was 3.0 per cent

compared with 4.2 per cent in 2004, in line with

lower external demand from the US. The fiscal

accounts for the year showed a reduced deficit of

0.9 per cent, mostly from windfall earnings from

high oil prices. As in 2004, high oil receipts and

increasing levels of workers’ remittances helped

minimise the current account deficit at an estimated

less than 1 per cent of GDP. The biggest

achievement was the reduction in headline inflation

from 5.2 per cent at the end of 2004 to 3.3 per cent

in December 2005, with core inflation finishing the

year at 3.1 per cent. HSBC views macroeconomic

stability as encouragingly robust ahead of what looks

likely to be a keenly contested presidential election

in mid-2006.

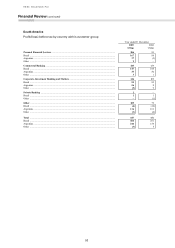

HSBC’s operations in North America reported a

pre-tax profit of US$6,872 million, compared with

US$6,070 million in 2004, representing an increase

of 13 per cent. On an underlying basis, pre-tax

profits grew by 12 per cent and represented around

33 per cent of HSBC’s equivalent total profit. In the

US, the benefits from strong deposit growth in

Personal Financial Services were partly negated by

narrowing spreads on lending in a rising interest rate

environment. In Commercial Banking, growth in

pre-tax profits was largely driven by lending and

deposit balance growth and improved liability

interest margins. In Corporate, Investment Banking

and Markets, growth in revenues was offset by

investment expenditure to build the required

platform and infrastructure for future growth.

The commentary that follows is on an

underlying basis.

Personal Financial Services, including the

consumer finance business, generated a pre-tax

profit of US$4,761 million, 8 per cent higher than in

2004. Under IFRSs, from 1 January 2005, HSBC

changed the accounting treatment for certain debt

issued and related interest rate swaps. This did not

change the underlying economics of the transactions.

The resulting revenues of US$618 million in 2004

are excluded from the following commentary. In

addition, interest income earned on mortgage

balances held on HSBC’s balance sheet pending sale

into the US secondary mortgage market has been

reported under trading income. In 2004 this was

reported in net interest income. This difference in

treatment has also been excluded from the following

commentary.

In the US, profit before tax rose 28 per cent to

US$3,853 million. The rise in profit was largely

driven by widening deposit spreads, strong deposit

and customer loan growth and higher fee income,

partly offset by lower asset spreads due to higher

funding costs. Loan impairment charges fell,

notwithstanding the higher charges due to the

combined impacts of Hurricane Katrina and changes

in bankruptcy legislation. In Mexico, excluding the

transfer of some customers to the Commercial

Banking segment due to alignment with Group

standards, pre-tax profits rose. This was driven by

strong revenue growth from higher deposit balances

and widening spreads, strong loan growth and higher

fee income, partly offset by the non-recurrence in

2005 of loan impairment provision releases in 2004.

Net interest income grew by 5 per cent to

US$12,753 million, largely from increases in the US

and Mexico. In the US, net interest income rose by

3 per cent largely driven by higher deposit balances

and widening deposit spreads. Average loan

balances grew strongly, in particular from prime and

non-prime residential mortgages. With ongoing

strong demand for unsecured lending, the credit

card, private label card and personal non-credit card,

portfolios continued to grow. The benefits of strong

asset growth were largely offset by lower spreads as

interest rates rose.

Additional resources were focused on the core

retail banking business in the US as high priority

was given to growing the deposit base. Investment in

the retail branch network continued, to ensure a

presence in locations with high growth potential.

During the year, 27 new branches were opened, each

tailored to meet the needs of the local market. The

launch of two new deposit products, HSBC’s first

national savings product, ‘Online Savings’, and

‘HSBC Premier Savings’, augmented by a 45 per

cent rise in new personal account openings, led to a

4 per cent growth in average deposit balances to

US$26.7 billion.

Overall, average mortgage balances including

US$3.3 billion held for resale were

US$112.1 billion, representing a 27 per cent

increase. This was due to the significant expansion

of adjustable rate mortgages (‘ARMs’) originated

during 2004 in the US bank and strong growth

within the mortgage services and branch-based

consumer lending businesses. These volume benefits

were largely offset by narrowing spreads as yields

fell due to changes in product mix and higher

funding costs.

Prime mortgages originated in 2005 were

largely sold into the large government sponsored

mortgage associations, reflecting a strategic decision

to focus on loans originated through the retail