HSBC 2005 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

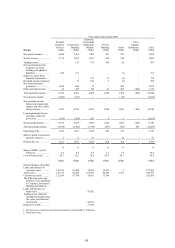

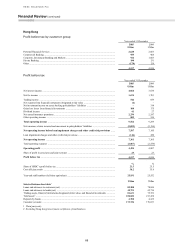

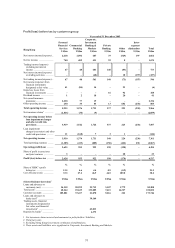

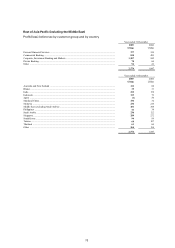

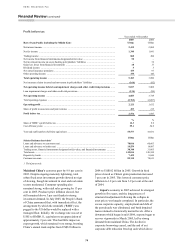

67

Hong Kong’s economy grew by 7.3 per cent in

2005, down from the growth of 8.6 per cent achieved

in 2004. Robust domestic demand provided strong

support, particularly in the second half of the year,

and external trade maintained its rapid rate of

growth. Despite a substantial rise of more than 3 per

cent in local interest rates in 2005, domestic demand

continued to expand, reflecting a sustained

improvement in business and consumer confidence.

Increased consumer spending, spurred by greater job

security as unemployment fell, and improving

household incomes, became a key driver of growth

in the latter part of the year. The rise in domestic

spending more than offset the slower growth in

tourists’ spending which occurred in 2005,

particularly among mainland visitors, and consumer

optimism remained unaffected by a cooling in the

property market induced by the higher interest rate

environment. Hong Kong’s strong export

performance also propelled growth, benefiting from

sustained external demand and foreign importers

building up inventories as trade talks continued on

textile quotas between mainland China and its major

trading partners. Domestic exports also picked up,

reflecting increased local production. In 2005,

inflation rose to 1.1 per cent, mainly driven by

increased demand for property rentals.

HSBC’s operations in Hong Kong reported a

pre-tax profit of US$4,517 million, compared with

US$4,830 million in 2004. IFRSs changes to the

treatment of preference share dividends led to a

US$387 million decrease in pre-tax profits.

Excluding this, profits increased by 2 per cent.

Subdued profit growth was largely attributable to a

turnaround in loan impairment charges, as 2004

benefited from non-recurring releases from general

provisions, and a fall in balance sheet management

revenues. Pre-tax profits in Hong Kong represented

around 22 per cent of HSBC’s total profit at this

level. In Corporate, Investment Banking and

Markets, balance sheet management revenues were

negatively affected by the influence of short-term

interest rate rises and a flattening yield curve.

Expense growth in Corporate, Investment Banking

and Markets reflected the first full-year effect of the

investment made to support business expansion. Pre-

tax profits of Personal Financial Services and

Commercial Banking grew by 27 per cent and

6 per cent respectively, benefiting from a sharp rise

in deposit spreads as short-term interest rates

increased in a benign credit environment.

The commentary that follows is on an

underlying basis.

Personal Financial Services reported a pre-tax

profit of US$2,628 million, 27 per cent higher than

in 2004. This was largely due to widening deposit

spreads, deposit growth and improved credit quality.

During the year, HSBC placed considerable

emphasis on maintaining its leadership position and

meeting customer needs in both the credit cards and

insurance businesses. Market share of both spend

and balances grew in respect of credit cards along

with strong insurance revenue growth.

Net interest income grew by 30 per cent to

US$2,618 million. During 2005, interest rates in

Hong Kong rose significantly, reflecting rising US

dollar interest rates. In addition, adjustments to the

Hong Kong: US dollar linked exchange rate system

reduced the likelihood of an upward realignment of

the Hong Kong dollar, prompting a reversal of much

of the inward flows from investors that had

depressed local market rates in 2004. Consequently,

deposit spreads widened to more normal levels after

the exceptionally low spreads experienced in 2004.

Interest rate rises also helped stimulate growth in

average deposit balances as investor sentiment

moved away from long-term equity-related

investments into shorter-term liquid deposits.

Despite the competitive deposit market, average

balances grew by US$2.9 billion, or 3 per cent.

The mortgage market remained highly

competitive during 2005. During the first half of the

year, HSBC did not aggressively compete on price

but maintained a selective approach to mortgage

approvals, mainly by offering competitive rates to

the existing customer base. Yields gradually

improved during the year, as HSBC repriced

upwards following a series of interest rates increases.

Spreads declined compared with 2004, as

improvements in yields were more than offset by

higher funding costs following rising interest rates.

Average mortgage balances, excluding the reduction

in balances under the suspended Hong Kong

Government Home Ownership Scheme (‘GHOS’)

grew by 1 per cent, despite the highly competitive

environment.

Average credit card balances grew by 10 per

cent, and HSBC’s market share of card balances also

increased by 550 basis points led by targeted

promotional campaigns and rewards programmes.

These volume benefits were more than offset by

lower spreads, mainly due to higher funding costs as

interest rates rose.

Net fees fell by 6 per cent to US$740 million,

driven mainly by lower sales of unit trusts and

capital guaranteed funds, partly offset by higher

sales of structured deposit products and open-ended

funds. A 34 per cent fall in unit trust fee income was

driven by a change in market sentiment during 2005.