HSBC 2005 Annual Report Download - page 316

Download and view the complete annual report

Please find page 316 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

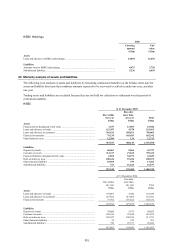

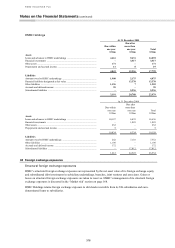

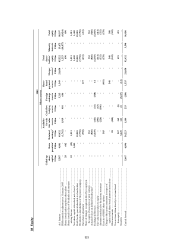

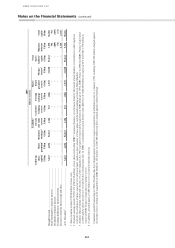

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

314

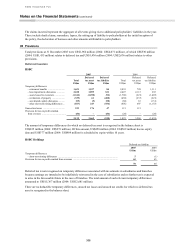

Performing loans are grouped, as far as possible, into homogeneous pools segregated by maturity and the coupon

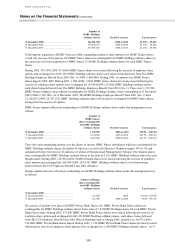

rates of the loans within each pool. In general, cash flows are discounted using current market rates for

instruments with similar maturity, repricing and credit risk characteristics. For fixed rate loans, assumptions are

made on the expected prepayment rates appropriate to the type of loan.

Conforming residential mortgages in the US are treated differently when there is an established market value for

asset-backed securities. In such cases, fair value is estimated by reference to quoted market prices for loans with

similar characteristics and maturities.

For impaired uncollateralised commercial loans, fair value is estimated by discounting the future cash flows over

the time period they are expected to be recovered. For impaired commercial loans where collateral exists, fair

value is the lower of the carrying values of the loans net of impairment allowances, and the fair value of the

collateral, discounted as appropriate.

(ii) Financial investments

In 2004, financial investments include debt securities and equity shares intended to be held on a continuing

basis. Such financial investments were included in the balance sheet at cost less provision for any permanent

diminution in value.

From 1 January 2005, on implementation of IAS39, the only financial investments not measured at fair value in

the balance sheet are held-to-maturity debt securities. Held-to-maturity debt securities are initially recorded at

fair value plus any directly attributable transaction costs, and are subsequently measured at amortised cost using

the effective interest rate method, less any impairment losses.

The fair values of listed financial investments are determined using bid market prices. The fair values of unlisted

financial investments are determined using valuation techniques that take into consideration future earnings

streams and valuations of equivalent quoted securities.

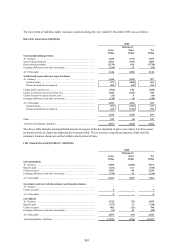

(iii) Deposits by banks and customer accounts

Deposits by banks and customer accounts are grouped by residual maturity. Fair values are estimated using

discounted cash flows, applying either market rates, where applicable, or current rates offered for deposits of

similar remaining maturities.

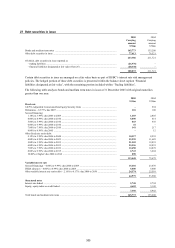

(iv) Debt securities in issue and subordinated liabilities

Fair values are determined using quoted market prices at the balance sheet date where applicable, or by reference

to quoted market prices for similar instruments.

The fair values presented in the table above are stated at a specific date and may be significantly different from the

amounts which will actually be paid or received on the maturity or settlement dates of the instruments. In many

cases, it would not be possible to realise immediately the estimated fair values. Accordingly these fair values do not

represent the value of these financial instruments to HSBC as a going concern.

The fair values of intangible assets, such as values placed on portfolios of core deposits, credit card relationships and

customer goodwill, are not included above, because they are not financial instruments.

As other financial institutions use different valuation methodologies and assumptions in determining fair values,

comparisons of fair values between financial institutions may not be meaningful and users are advised to exercise

caution when using this data.

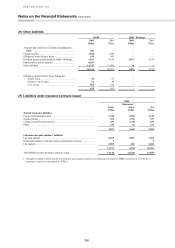

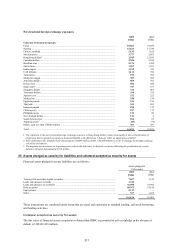

In addition, the following table lists those financial instruments where the carrying amount is a reasonable

approximation of fair value, for example, because they are either short term in nature or reprice to current market

rates frequently:

Assets Liabilities

Cash and balances at central banks Hong Kong Government currency notes in circulation

(representative of Hong Kong banknotes issued)

Items in the course of collection Items in the course of transmission

Hong Kong Government certificates of indebtedness

(representative of Hong Kong banknotes issued)

Endorsements and acceptances

Endorsements and acceptances Short-term payables within ‘Other Liabilities’

Short-term receivables within ‘Other Assets’