HSBC 2005 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

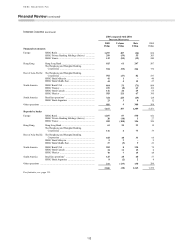

HSBC HOLDINGS PLC

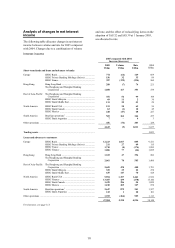

Financial Review (continued)

120

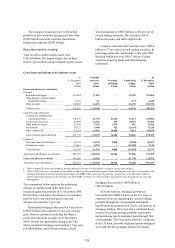

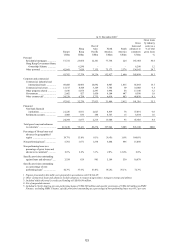

branch expansions in the consumer finance business

delivered a 17 per cent increase in mortgage lending.

Residential mortgage balances in Hong Kong

were broadly flat, in what remained a highly

competitive market. There was a net repayment in

mortgages under the Hong Kong GHOS, under

which new advances remained suspended. In the rest

of Asia-Pacific, an increase of 22 per cent in

mortgage lending was driven by operations in the

Middle East, India, Taiwan, South Korea, mainland

China and Singapore, in each of which growth was

over 30 per cent.

Other personal lending increased by 17 per cent

to US$182 billion, and represented 24 per cent of

total gross loans to customers at 31 December 2005.

The acquisition of Metris in December 2005

increased personal loans by US$5 billion, or

3 percentage points of the growth in 2005. Including

and in part due to this, some 75 per cent of growth

was in North America. Organic growth within the

US in HSBC branded prime, Union Privilege and

non-prime portfolios, partly offset by the continued

decline in certain older acquired portfolios, also

contributed to the increase. The US vehicle finance

business reported strong organic growth, principally

in the near-prime portfolios. This came from newly

originated loans acquired through the dealer

network, growth in the consumer direct loan

programme and expanded distribution through

alliance channels. Growth in personal non-credit

card lending reflected HSBC’s increasing the

availability of this product in the second half of

2004, as a result of an improving US economy, as

well as the success of several large direct mail

campaigns launched in 2005.

In Europe, the charge-off of substantially

provided personal loans against provisions masked

the underlying growth in lending: Other personal

lending net of impairment reserves grew by 13 per

cent. In the UK, growth in credit card and other

unsecured lending was driven by pricing and

marketing initiatives, against the backdrop of

subdued consumer spending. In Turkey, credit card

lending rose markedly, also helped by marketing

campaigns.

In the Rest of Asia-Pacific, continuing

expansion of the credit card base and higher

utilisation of cards by existing customers, together

with successful marketing, contributed to a 25 per

cent increase in lending. In South America,

marketing and new product launches, combined with

improved consumer sentiment, contributed to

underlying growth of 26 per cent in Brazil.

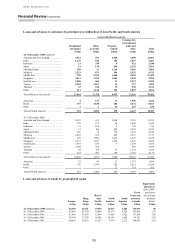

Loans and advances to the corporate and

commercial sectors grew by 12 per cent during 2005,

predominantly in the Commercial Banking customer

group.

In Europe, corporate and commercial advances

increased by 10 per cent, reflecting customer

demand for credit, as well as new customer

acquisition, particularly in the property, distribution

and services sectors. In Hong Kong, an 11 per cent

increase was mainly in the property and

manufacturing sectors, in part reflecting the benefit

of economic expansion in mainland China. This was

also reflected in the Rest of Asia-Pacific, where

strong regional economies, and significant

government-backed infrastructure and property

projects, also contributed to the 16 per cent increase

overall. In North America, a 15 per cent increase

was driven by lending to finance real estate projects

and construction, as well as increases in most other

sectors and industries.

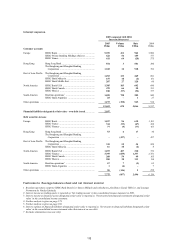

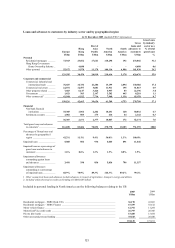

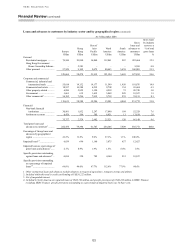

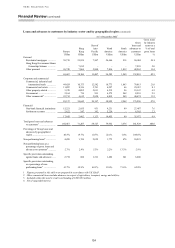

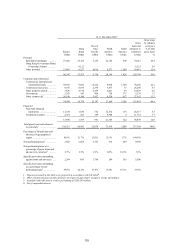

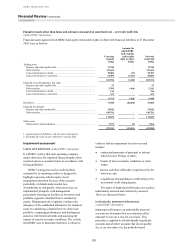

The following tables analyse loans by industry

sector and by the location of the principal operations

of the lending subsidiary or, in the case of the

operations of The Hongkong and Shanghai Banking

Corporation, HSBC Bank, HSBC Bank Middle East

and HSBC Bank USA, by the location of the lending

branch.