HSBC 2005 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

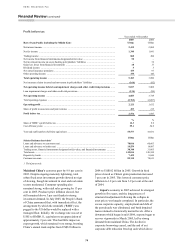

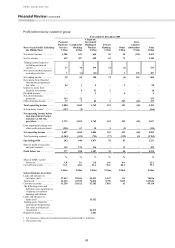

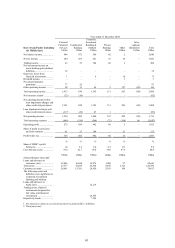

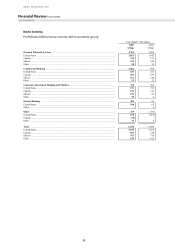

75

stronger growth in private capital investment. The

tightening of the labour market boosted employment

and led to a sustained rise in real wages for the first

time in five years, providing strong support for

consumer spending. The rise in the core consumer

price index in November 2005 set the stage for the

end of the Bank of Japan’s quantitative easing policy.

Elsewhere in the region, most economies

performed impressively in 2005, in particular India’s.

The main drivers of growth were exports, demand for

technology, and domestic consumption. Investment

demand, by contrast, remained weak. Strong

domestic growth and continued firmness in energy

prices resulted in an increase in inflationary

pressures, especially in Indonesia and Thailand,

where fuel subsidies were lowered or removed.

Central banks in both these countries increased rates

substantially. Elsewhere, particularly in South Korea

and Taiwan, energy prices did not significantly affect

headline inflation, and the benign inflationary

environment was maintained with less need for

monetary tightening. Most Asian currencies ended

the year strongly against the US dollar.

2005 was a good year economically for the

Middle East, where growth was boosted by high oil

prices and additional capacity in downstream oil and

gas, real estate, transportation and tourism. Long-

term growth was reinforced through economic

liberalisation. The result was to encourage private

sector investment in both established and new sectors

of the region’s economy. Regional interest rates

mirrored US dollar rate increases during the year

without any noticeable effect on credit growth,

though inflationary pressures arose from the US

dollar’s weakness and general economic expansion.

GDP growth is estimated by the International

Monetary Fund to have been over 6 per cent in Saudi

Arabia in 2005. Economies in the region which are

not as dependent on oil also performed well, with the

United Arab Emirates, for example, registering

strong growth in non-oil sectors such as financial

services and tourism.

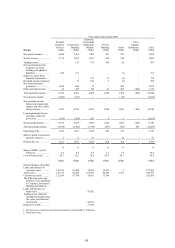

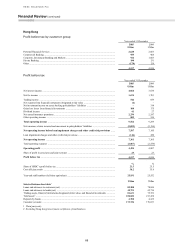

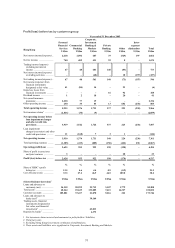

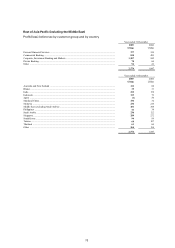

HSBC’s operations in the Rest of Asia-Pacific

reported a pre-tax profit of US$2,574 million,

compared with US$1,847 million in 2004,

representing an increase of 39 per cent. On an

underlying basis, pre-tax profits grew by 29 per cent

and represented around 12 per cent of HSBC’s

equivalent total profit. Strong growth across the

majority of countries in the region resulted in higher

revenues across all customer groups.

The commentary that follows is on an underlying

basis.

Personal Financial Services reported a pre-tax

profit of US$377 million, an increase of 6 per cent

compared with 2004, reflecting higher net interest

income led by strong asset and deposit growth,

increased fee income and higher income from

investments in the Middle East and mainland China.

Costs in support of business expansion rose and were

broadly in line with revenue growth. Higher loan

impairment charges reflected growth in credit card

lending and the non-recurrence in 2005 of loan

impairment provision releases in 2004.

Net interest income grew by 25 per cent to

US$1,208 million, reflecting strong growth across

the majority of countries in the region. Deposit

balances generally grew strongly during 2005. This

was due in part to the range of new products

launched during the year, including dual currency,

floating rate and higher-yielding time deposits. The

number of Premier account holders rose

significantly, with a 40 per cent growth across the

region generating US$3.5 billion of additional

balances. In mainland China, organic expansion

continued, with the opening of ten new branches and

sub-branches. The deposit base grew by 80 per cent,

as considerable emphasis was placed on the provision

of wealth management services through the HSBC

Premier account service. Deposit spreads also

widened as interest rates rose, contributing to higher

net interest income in mainland China, Singapore and

India.

In the Middle East, a rise of 37 per cent in net

interest income was driven by a combination of

widening deposit spreads and strong loan growth,

partly offset by lower asset spreads as funding costs

increased following interest rate rises.

Average mortgage balances increased by 27 per

cent to US$16.7 billion. This growth reflected

marketing campaigns in India, Malaysia and

Singapore alongside new products introduced in

Australia and Korea. Higher sales volumes were also

generated by direct sales forces across the region,

notably in India, where mortgage balances grew by

43 per cent. The benefits of higher mortgage balances

were partly offset by lower spreads as pricing stayed

highly competitive.

The credit card business continued to expand in

a number of countries. Credit card spending

increased by 33 per cent, contributing to a 42 per cent

growth in average card balances. Other notable

developments included promotional campaigns, new

product launches and a series of customer acquisition

strategies including the exclusive rewards

programme, ‘Home and Away’. At the end of the

year, the number of cards in circulation stood at