HSBC 2005 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2005 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

|

|

165

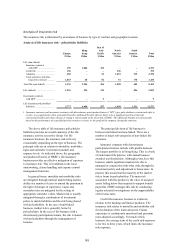

UK, Mexico and Argentina. Reinsurance protection

has been arranged where necessary to avoid

excessive exposure to larger losses, particularly

those relating to personal injury claims.

Fire and other damage business is written in all

major markets, most significantly in Europe. The

predominant focus in most markets is insurance for

homes and contents while covers for selected

commercial customers are largely written in Asian

and South American markets. All portfolios at risk

from catastrophic losses are protected by reinsurance

in accordance with information obtained from

professional risk-modelling organisations.

A very limited portfolio of liability business is

written in major markets.

Following the disposal of the non-life insurance

portfolio in Brazil, credit non-life business now

represents the largest single class and is concentrated

in the US and the UK. This business is written in

relation to the banking and finance products.

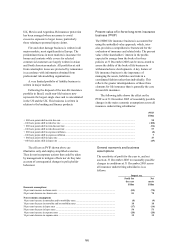

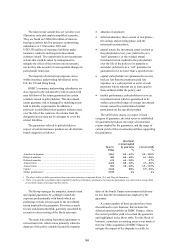

Present value of in-force long-term insurance

business (‘PVIF’)

The HSBC life insurance business is accounted for

using the embedded value approach, which, inter

alia, provides a comprehensive framework for the

evaluation of insurance and related risks. The present

value of the shareholders’ interest in the profits

expected to emerge from the book of in-force

policies at 31 December 2005 can be stress-tested to

assess the ability of the book of life business to

withstand adverse developments. A key feature of

life insurance business is the importance of

managing the assets, liabilities and risks in a

coordinated fashion rather than individually. This

reflects the greater interdependence of these three

elements for life insurance than is generally the case

for non-life insurance.

The following table shows the effect on the

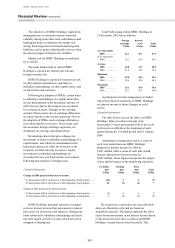

PVIF as at 31 December 2005 of reasonably possible

changes in the main economic assumptions across all

insurance underwriting subsidiaries:

PVIF

US$m

+ 100 basis points shift in risk-free rate ........................................................................................................................... 90

– 100 basis points shift in risk-free rate ........................................................................................................................... (100)

+ 100 basis points shift in risk discount rate .................................................................................................................... (54)

– 100 basis points shift in risk discount rate .................................................................................................................... 57

+ 100 basis points shift in expenses inflation ................................................................................................................... (8)

– 100 basis points shift in expenses inflation ................................................................................................................... 7

+ 100 basis points shift in lapse rate ................................................................................................................................ 47

– 100 basis points shift in lapse rate ................................................................................................................................ (49)

The effects on PVIF shown above are

illustrative only and employ simplified scenarios.

They do not incorporate actions that could be taken

by management to mitigate effects nor do they take

account of consequential changes in policyholder

behaviour.

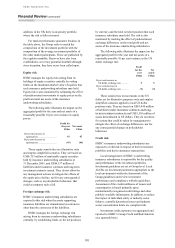

General economic and business

assumptions

The sensitivity of profit for the year to, and net

assets at, 31 December 2005 to reasonably possible

changes in conditions at 31 December 2005 across

all insurance underwriting subsidiaries is as

follows:

Impact on:

Profit for

the year

Net

assets

US$m US$m

Economic assumptions

20 per cent increase in claims costs ................................................................................................ (82) (78)

20 per cent decrease in claims costs ................................................................................................ 81 78

Non-economic assumptions

10 per cent increase in mortality and/or morbidity rates.................................................................. (8) (9)

10 per cent decrease in mortality and/or morbidity rates ................................................................. 18 18

50 per cent increase in lapse rates ................................................................................................... (17) (14)

50 per cent decrease in lapse rates................................................................................................... 56 51

10 per cent increase in expense rates .............................................................................................. (20) (20)

10 per cent decrease in expense rates .............................................................................................. 19 19