Xcel Energy 2012 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2012 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

113

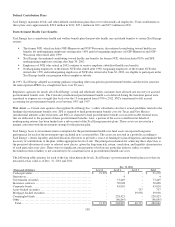

Investments in equity securities and other funds — Equity securities are valued using quoted prices in active markets. The fair

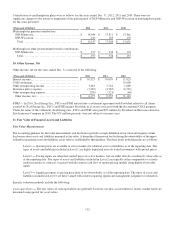

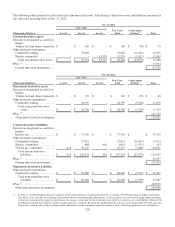

values for commingled funds, international equity funds, private equity investments and real estate investments are measured

using net asset values, which take into consideration the value of underlying fund investments, as well as the other accrued assets

and liabilities of a fund, in order to determine a per share market value. The investments in commingled funds and international

equity funds may be redeemed for net asset value with proper notice. Private equity investments require approval of the fund for

any unscheduled redemption, and such redemptions may be approved or denied by the fund at its sole discretion. Unscheduled

distributions from real estate investments may be redeemed with proper notice; however, withdrawals from real estate

investments may be delayed or discounted as a result of fund illiquidity. Based on Xcel Energy’s evaluation of its ability to

redeem private equity and real estate investments, fair value measurements for private equity and real estate investments have

been assigned a Level 3.

Investments in debt securities — Fair values for debt securities are determined by a third party pricing service using recent trades

and observable spreads from benchmark interest rates for similar securities, except for asset-backed and mortgage-backed

securities, for which the third party service may also consider additional, more subjective inputs. Since the impact of the use of

these less observable inputs can be significant to the valuation of asset-backed and mortgage-backed securities, fair value

measurements for these instruments have been assigned a Level 3. Inputs that may be considered in the valuation of asset-backed

and mortgage-backed securities in conjunction with pricing of similar securities in active markets include the use of risk-based

discounting and estimated prepayments in a discounted cash flow model. When these additional inputs and models are utilized,

decreases in the risk-adjusted discount rates and any acceleration of the assumed future principal prepayment rates each have the

impact of increasing reported fair values for these instruments.

Interest rate derivatives — The fair values of interest rate derivatives are based on broker quotes that utilize current market

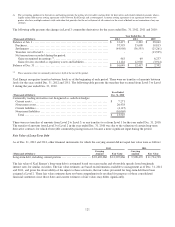

interest rate forecasts.

Commodity derivatives — The methods used to measure the fair value of commodity derivative forwards and options utilize

forward prices and volatilities, as well as pricing adjustments for specific delivery locations, and are generally assigned a Level 2.

When contractual settlements extend to periods beyond those readily observable on active exchanges or quoted by brokers, the

significance of the use of less observable forecasts of long-term forward prices and volatilities on a valuation is evaluated, and

may result in Level 3 classification.

Electric commodity derivatives held by NSP-Minnesota include FTRs purchased from MISO. FTRs purchased from MISO are

financial instruments that entitle or obligate the holder to one year of monthly revenues or charges based on transmission congestion

across a given transmission path. The value of an FTR is derived from, and designed to offset, the cost of energy congestion, which is

caused by overall transmission load and other transmission constraints. In addition to overall transmission load, congestion is also

influenced by the operating schedules of power plants and the consumption of electricity pertinent to a given transmission path.

Unplanned plant outages, scheduled plant maintenance, changes in the relative costs of fuels used in generation, weather and overall

changes in demand for electricity can each impact the operating schedules of the power plants on the transmission grid and the value

of an FTR. NSP-Minnesota’s valuation process for FTRs utilizes complex iterative modeling to predict the impacts of forecasted

changes in these drivers of transmission system congestion on the historical pricing of FTR purchases.

If forecasted costs of electric transmission congestion increase or decrease for a given FTR path, the value of that particular FTR

instrument will likewise increase or decrease. Given the limited observability of management’s forecasts for several of the inputs

to this complex valuation model – including expected plant operating schedules and retail and wholesale demand, fair value

measurements for FTRs have been assigned a Level 3. Monthly FTR settlements are included in the FCA, and therefore changes

in the fair value of the yet to be settled portions of FTRs are deferred as a regulatory asset or liability. Given this regulatory

treatment and the limited magnitude of NSP-Minnesota’s FTRs relative to its electric utility operations, the numerous

unobservable quantitative inputs to the complex model used for valuation of FTRs are insignificant to the consolidated financial

statements of Xcel Energy.

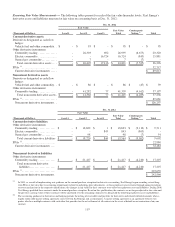

Non-Derivative Instruments Fair Value Measurements

The NRC requires NSP-Minnesota to maintain a portfolio of investments to fund the costs of decommissioning its nuclear

generating plants. Together with all accumulated earnings or losses, the assets of the nuclear decommissioning fund are legally

restricted for the purpose of decommissioning the Monticello and Prairie Island nuclear generating plants. The fund contains cash

equivalents, debt securities, equity securities and other investments – all classified as available-for-sale. NSP-Minnesota plans to

reinvest matured securities until decommissioning begins. The MPUC approved NSP-Minnesota’s proposed change in escrow

fund investment strategy in September 2012. The MPUC approved an asset allocation for the escrow and investment targets by

asset class for both the escrow and qualified trust.